LINN Energy (LINE, LINCO) holds 95,000 net acres prospective for the Granite Wash play on the border of the TX Panhandle and SW Oklahoma (according to the Company's website). The majority of the acreage is in Hemphill County, TX, Wheeler County, TX, and Roger Mills County, OK.

Source: LINN Energy Presentation

In LINN's 4/1/13 presentation, "LINN Energy Response to Another Round of Short Seller Comments," the Company shows its "NAV Schedule (Internal Case)" on slide 9:

Source: LINN Energy Presentation

LINN states that it has 6.2 Tcfe of unproven volume in the Granite Wash, or 44% of its total unproven volume. The value that LINN has put on this total unproven value is $6.5B - $11.2B. If we take 44% of that (that's the best we can do), LINN values its Granite Wash unproven volume at $2.9B - $4.9B. LINN also has 0.4 Tcfe of PUD reserves in the Granite Wash, or 20% of its total PUD reserves. The value that LINN has put on its total PUD reserves is $1.9B. If we take 20% of that, LINN values its Granite Wash PUD reserves at $380MM. In total, LINN assigns $3.3B - $5.3B of value to its non-producing Granite Wash play.

We showed in our 4/5/13 presentation Response to LINN Energy's 4/1/13 Presentation & Additional Research that recent Granite Wash transactions like the Apache/Cordillera, Noble/Unit, and LINN/Plains deals suggested a value only a fraction of what LINN was representing to investors, and those deals were struck around $6,000 - $7,000/acre (after backing out the production).

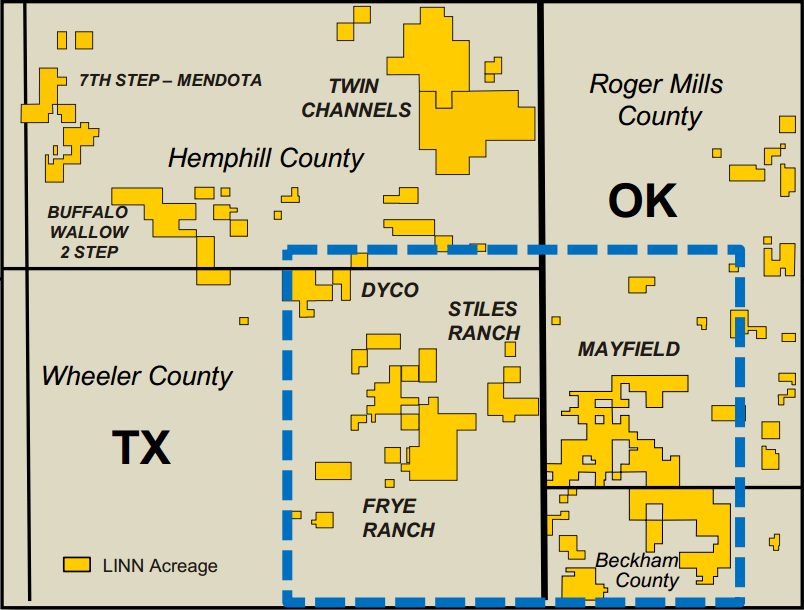

Yesterday we got our latest mark on Granite Wash acreage as Laredo Petroleum (LPI) sold its Anadarko Basin properties to EnerVest (private) for $438MM. The properties produced 58 MMcfe/d (94% liquids-rich gas) in 1Q13. Included in the deal were ~37,000 acres in the Granite Wash and ~67,000 acres in the Eastern Anadarko and Central TX Panhandle. LPI's Granite Wash play borders Hemphill County, TX and Roger Mills County, OK, as pictured below:

Source: Laredo Petroleum Presentation

If we assign a value on the production at $5,000 per flowing Mcfe (standard for gassy volumes), and 0 value to the non-Granite Wash acreage, that leaves us with a market value on Granite Wash acreage of $3,999/acre.

Putting that metric on LINN's 95,000 net acres gives us a non-producing value of $380MM.

So LINN's internal NAV of its Granite Wash play is ~$3.3B - $5.3B, and the market says its worth $380MM. That's quite the bid/ask...

Kevin Kaiser

Senior Analyst