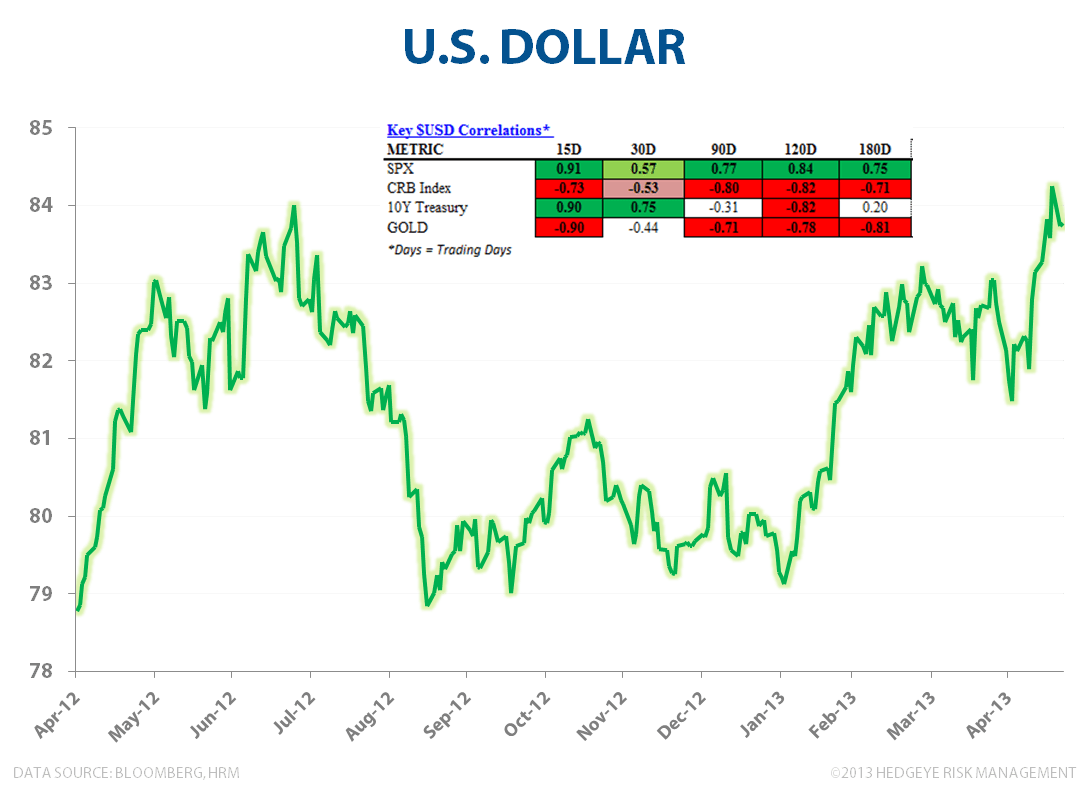

It’s critical to pay close attention to what the US dollar is doing in the immediate term, as it serves as a good indicator of what lies ahead in the intermediate and longer term.

Get this:

- On a three week basis, the S&P 500 versus the USD has a remarkable, positive correlation of +0.91. That is just fantastic. (Correlation of course is a statistical measure of how two securities move in relation to each other. Correlation varies from +1 to -1. Values close to +1 indicate a high-degree of positive correlation while values close to -1 indicate a high degree of negative correlation.

- Meanwhile, the 10-year bond yield positive correlation versus the USD is +0.92 on a 3-week basis. That’s better than fantastic.

- To top it off, gold has a negative 3-week inverse correlation of -0.87 against the dollar.

Is that telling you something?

Bottom line: If you get the dollar right, you get a lot of things right. The dollar is getting stronger folks, not weaker. And that’s why we’re not ready to get off the bullish rocking horse.

Check out the chart below. It shows the performance of the USD index which has risen sharply since January. Note the table which shows the key correlations between the dollar and the S&P 500, commodities, 10-year Treasury and gold.