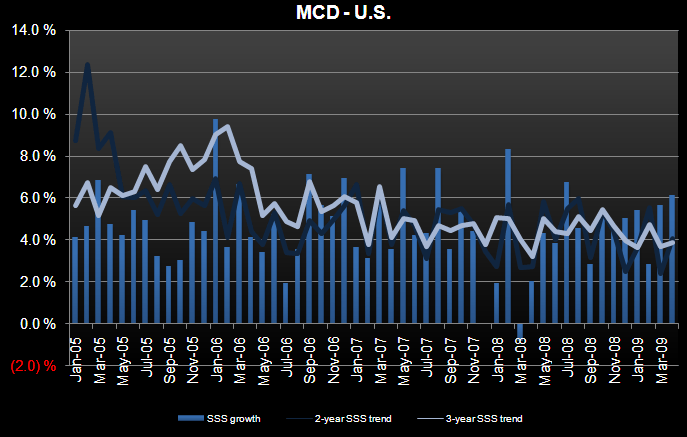

There is no denying that these are some very strong monthly sales numbers from MCD, especially in light of the trends we're seeing at Burger King, Wendy's, and the rest of the consumer names.

So where do we go from here?

The summer will be critical for MCD as the discounted drink promotion was an enormous success for the company last year. If you are a believer that MCD's Latte promotion will be a successful follow up to the drink promotion, there is nothing to worry about. Personally, it's hard to see how an expensive hot beverage is going to do as well as a cheap cold beverage in the summer.

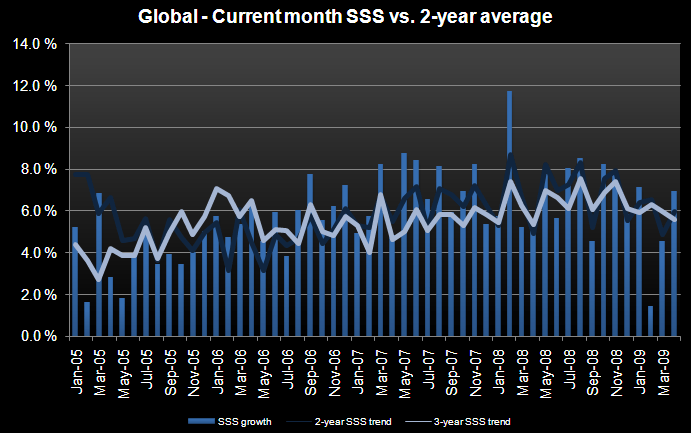

For the balance of 2009 McDonald's global comps get much more difficult; the US comparisons get more difficult peaking at 6.7%; Europe peaks at 11.6% in August and AMPEA in November at 13.3% (10% August comparison).

The current sales trends we are seeing from McDonald's can challenge my cautious stance on the stock. I still stand with my thesis that MCD's coffee strategy moves the store execution away from the core competency of the company and the price tag will limit the success. The average check at breakfast for McDonald's is $3 (+/- $0.50 depending on how you order). Adding a $3+ latte will double the average check at breakfast! Once we get past the trial phase, sticker shock will limit repeat business.