Below we hit on a number of topics and developments across Europe.

Call: Largely our bullish outlook on the capital markets across much of the region has not changed, anchored behind the ECB’s willingness to leverage its balance sheet at all costs to save the Union; the European Commission’s willingness to extend fiscal consolidation targets and abandon or lessen austerity programs; and Germany’s willingness to continue to write bailout checks versus the very adverse option of a strong D-Mark.

Further, we’re seeing a decrease in the broader risk profile as Italy has named a new PM and works through a new budget; Slovenia is willing and able to take care of its own bailout needs; and Portugal has set forth a fiscal consolidation program and issued its own sovereign debt this week. Finally, peripheral sovereign auctions continue to price debt lower and data has looked mostly better in APR compared to MAR.

That said, the disconnect with muted to weak fundamentals remains anchored. The credit system across the region, in particular to small-and-medium-sized enterprises (SMEs), remains clogged; unemployment remains staggeringly high; and the Union of uneven countries under one monetary policy and currency remains flawed in its present set-up. This is in line with our call for a very protracted period of low to negative growth throughout Europe.

GBP/USD: On Thursday we added a real-time long position in the GBP/USD via the etf FXB given the BOE opted to leave rates and the QE program unchanged on Thursday. We also see the replacement of Mervyn King in July by the slightly more hawkish Canadian Mark Carney as a bullish catalyst.

ECB Playing Large

Following the 25bps rate cut last week from the ECB below are two statements that stood out this week. While the statements are bullish in terms of the Bank signaling it is ready to act, we expect Draghi to wait and watch the data over the upcoming months to assess the impact of the actions he’s already taken. One thing the bank has little control over is the rate at which it can help unclog the credit channel, especially to small-and-medium-sized enterprises (SMEs).

- Draghi signaled that the central bank stands ready to do more if economic conditions in the Eurozone continue to deteriorate.

- ECB Executive Board Member Yves Mersch said that the ECB still has tools at its disposal, though he noted that it could only spur lending to SMEs in conjunction with other European institutions.

Austerity is Mostly Dead

One on-going theme remains the backlash against austerity. Below are some statements from this week:

- French Finance Minister Pierre Moscovici said that the era of austerity is over in the Eurozone.

- European Commission President Jose Manuel Barroso defended the current prescription, though he also reiterated that policies seen as pure austerity have reached their limits of social and political acceptance.

- German Finance Minister Wolfgang Schaeuble said that there is a "certain flexibility" in allowing France and Spain additional time to meet their deficit targets (France and Spain to get 2 extra year to reach its deficit target, and the Netherlands one extra year).

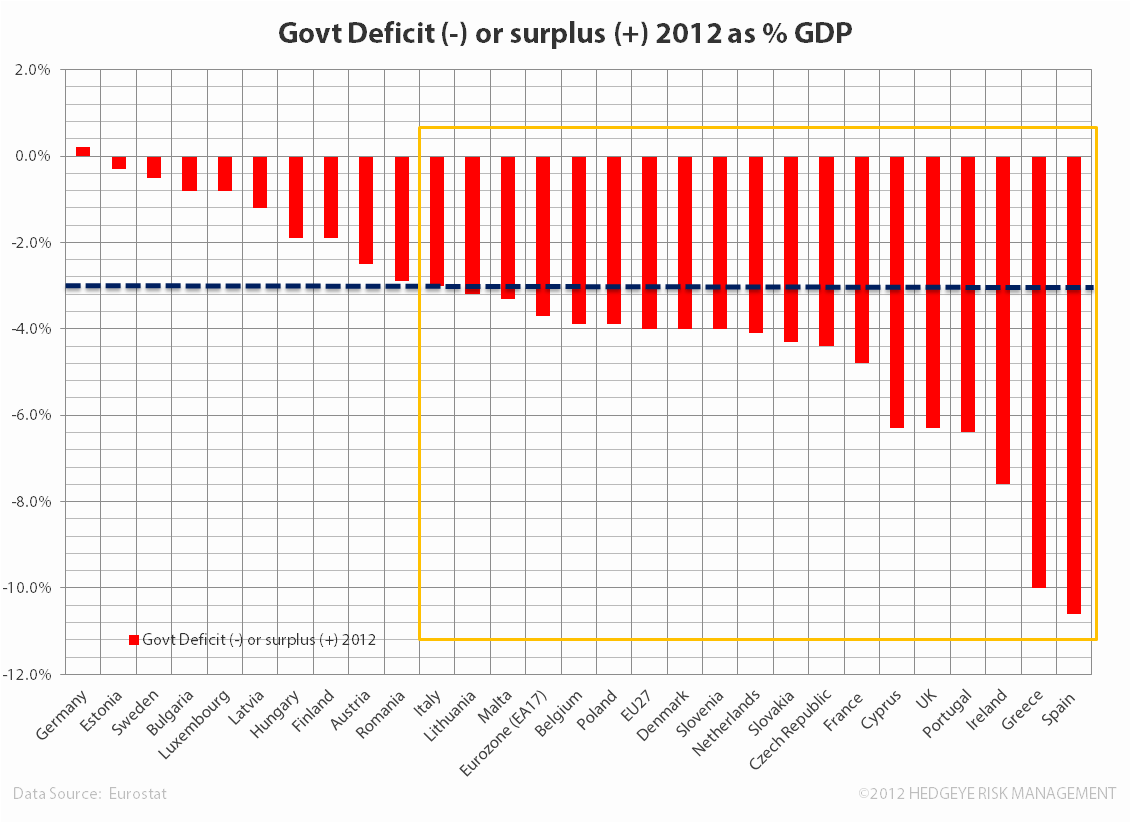

In the charts below we show a snapshot of 2012 debt and deficit levels (as a % of GDP) across the region. What governments need to do is have a balanced approach to austerity and structural reforms. The problem is that structural reform is a broad term that means different things for different countries and given the current fiscal set-ups (and recent consolidation measures), it may be easier or harder to implement based on the country. Most governments are on very uneven terms with their constituencies (given the bite of austerity, or in the case of the Germany the open checkbook), so policy makers are advancing without great leverage. In June EU leaders will sign binding “contracts” on structural reform, yet we have our doubts and foresee little being accomplished.

On the argument for the need of unit labor costs to come down in the periphery, part of the problem is that inflation is typically higher, so it’s simply another competitive tax vis-à-vis Germany. While the idea of higher unit labor costs in Germany has been floated, what really needs to happen is to allow unit labor costs to inflate or at least remain flat (so the people don’t revolt) and to stoke inflation to minimize the debt repayment that much of the periphery owes. This naturally goes against the inflation mandate of the ECB, so here too we expect continued gridlock, with Germany benefitting over much of the region’s loss.

We think German Chancellor Merkel will continue to play her cards, toting the line of not giving up on other country’s need to implement austerity but at the same time not supporting austerity that fully chokes off growth. She’ll be cautious in her tone as she crafts her re-election face domestically and internationally ahead of elections this September.

Portugal Mending?

This was a big week for Portugal. Into the end of last week Portuguese PM Pedro Passos Coelho outlined further austerity measures that involve €4.8B in spending cuts over the next three years. The plan includes:

- shrinking the number of public sector employees by 30K, or 5%

- requiring public employees to work 40 hours a week (five hours longer than they do now)

- increasing the retirement age by one year to 66

- raising the tax on some pension income

While its passage may face opposition, we believe it’s the right directional step. Further, Portugal returned to the bond market on Tuesday, selling €3B of 10YR notes at 5.67%. Demand for the new paper was strong at more than €10B of orders. Portuguese Treasury Secretary Maria Luís Albuquerque said that foreign investors took down 86% of the issue. She added that traditional investors were the biggest buyers, while hedge funds purchased just 7%. Separately Portuguese Finance Minister Vítor Gaspar said that the country had already met its financing needs for this year and was “pre-financing” 2014.

Of note on the successful bond auction is that the 10YR maturity is symbolic because it is viewed as a key criterion for "market access" that the ECB has determined as condition for OMT eligibility.

PMIs

While Final APR PMI figures looked better than initial readings, you’ll note the PMIs across Services and Manufacturing remain well below the 50 line dividing expansion (above) and contraction (below). The fundamental data continues to contrast with the strong performance from most European capital markets.

Slovenia Helps Itself

Slovenia on Thursday outlined a plan to help avoid an international bailout. The key elements of the plan included an increase in the VAT to 22% from 20% and the sale of about 15 state-owned companies. The funds will be used to recapitalize the banking sector, where the three state-owned banks together have about €7B in bad loans, equivalent to about 20% of the country's annual economic output.

The decision by the government confirms our thinking that Slovenia would not possess the spotlight Cyprus did given the limited leverage to the banking system in comparison. The EU has said that it will study the plans and issue its own recommendations later this month.

Enjoy your weekend!

Matthew Hedrick

Senior Analyst