If you have been reading out research regularly we are not shy about calling out if we the stock is a compelling short. We have some shorts on our radar but CMG is not one!

Jeff Gundlach recommended CMG as a short at the Sohn Conference. He has a simple take on the company and its competitive environment, contending, in essence that “a burrito is a burrito”. Here is a quote from Forbes, reporting on his presentation, that goes some way toward summarizing his view:

“a gourmet burrito is an oxymoron... Barriers to entry aren’t all that high, when all that is needed to enter the market is a taco truck... I’m not impressed with [Chipotle’s] earnings growth or its high P/E ratio.”

We have a few points that are worth considering before shorting CMG alongside Mr. Gundlach:

- P/E ratios may be artificially high because of overly-cautious earnings estimates. We think this is the case, currently, for CMG.

- The company’s service model has redefined the industry and leads to above average margins and returns. Comparing CMG to others in QSR, in this regard, is not helpful.

- “Food with Integrity” resonates with millennials and is clearly an early move within a much broader industry trend.

- The barrier to entry point applies to all varieties of food, hamburgers, etc. We do not understand this point.

What Would Make CMG a Short?

We would short CMG upon gaining conviction that its growth story is faltering. New Unit Volumes are, increasingly, a key metric to follow with respect to future sales trends. This trend seems to be improving. We were overly gun-shy in January, when this metric was showing signs of turning around, in staying on the sidelines. While earnings revisions continued lower, the stock moved higher in anticipation of better sales growth. As long as the macro environment continues to improve, we believe that this metric will continue on its current trajectory.

To sum up, here are some of the more CMG important metrics that suggest that CMG is not a short:

- Sell-side sentiment has deteriorated over the past year

- Buy-side sentiment is negative as shown by high short interest

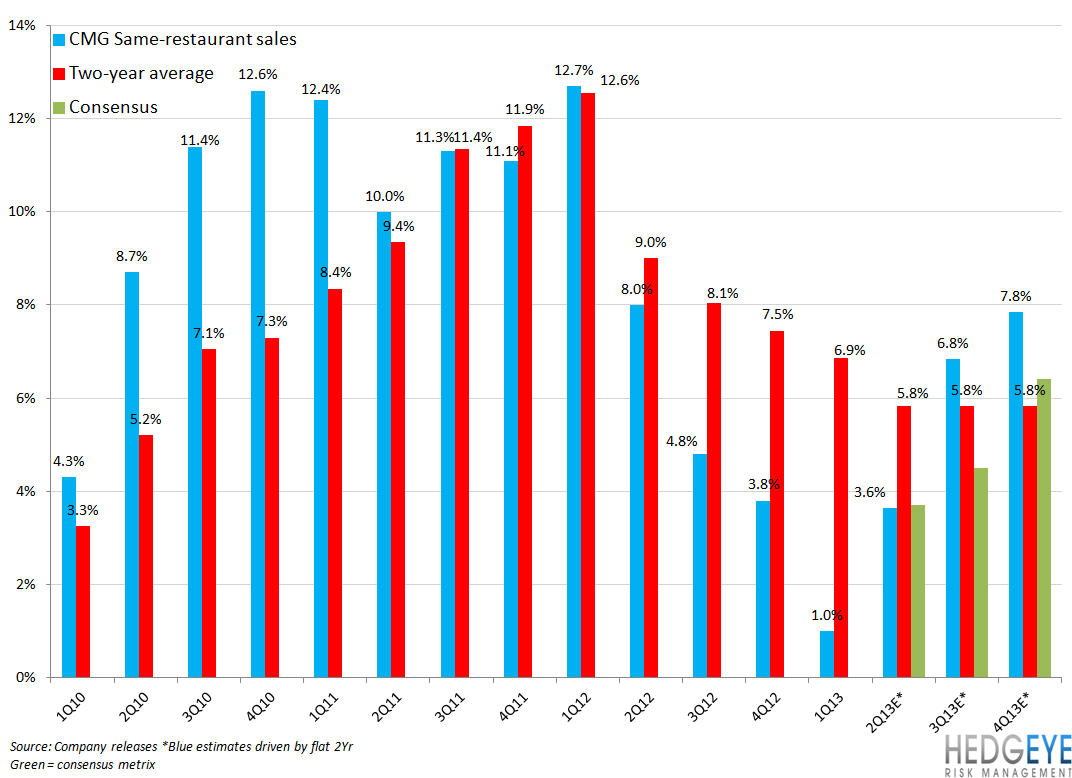

- New store average unit volumes are rising

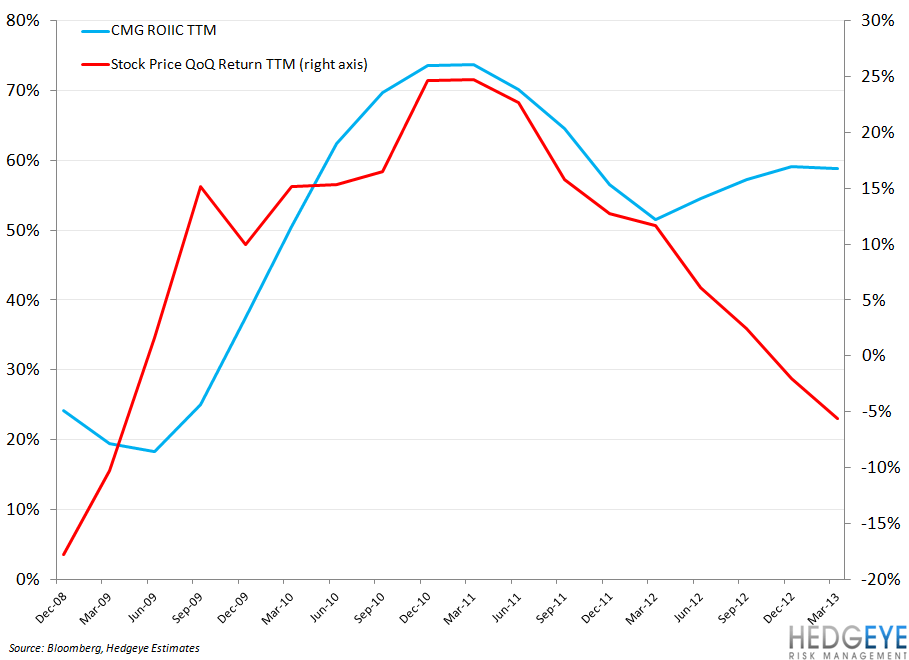

- ROIIC on a TTM basis has stabilized and rising

- EBITDA to Cap Ex is 3.0x

- 2013E EPS estimates are rising

- SSS comparison get easier for the balance of 2013 (and look to be trending positive in the current quarter)

- Food inflation is easing

- $500 million in cash and no funded debt on the balance sheet

- Valuation is rich, but reasonable given the growth model

We believe investors shorting CMG here will suffer. CMG is a growth story, with easing inflation pressures, high margins and returns, that has seen sentiment sequentially deteriorate over the last year. We expect earnings expectations to increase over the next six months.

Howard Penney

Managing Director

Rory Green

Senior Analyst