The upside in McDonald’s stock is not being driven by the company’s fundamentals. The underperformance in the stock since we added it to our Best Ideas list on 4/25, is , is likely to continue and, if we are right on the numbers, could become worse for shareholders.

The company has a lot of work to do to turn its operational performance around and we are not seeing any indication that this reversal will transpire any time soon. Management's recital of the (stale) tenets of the current Plan to Win, “optimize our menu, modernize the customer experience and broaden accessibility to brand McDonald's around the world”, as an answer to all ills, does not instill confidence that the current leadership is coming up with new ideas to counteract the company’s current operating headwinds.

April SRS vs Consensus (Consensus Metrix)

- US Beat: +0.7% versus consensus -0.1%

- Europe Missed: -2.4% versus consensus -1.0%

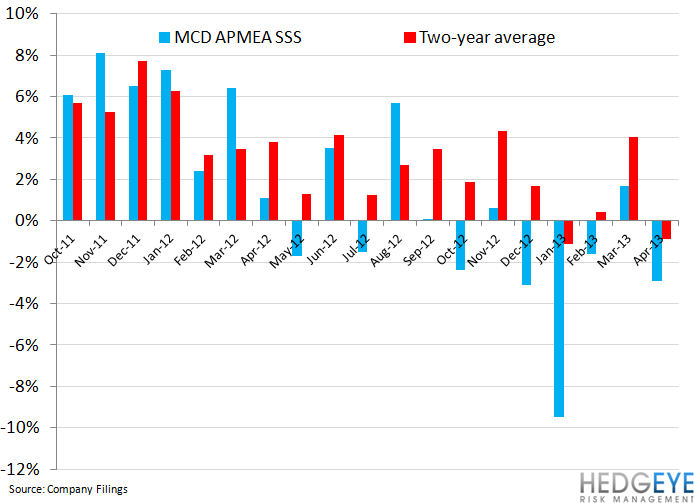

- APMEA Missed: -2.9% versus consensus -1.4%

- Global Missed: -0.6% versus consensus -0.5%

United States: “Premium McWraps, compelling value options and the ongoing popularity of McDonald's breakfast contributed to the month's results.

Europe: “positive performance in the U.K. and Russia more than offset by Germany, France and other markets.”

APMEA: Results reflected “the impact of Avian influenza, primarily in China, and softer results in Japan and Australia.”

Without Sales Growth, Earnings Growth Will Be Difficult

In 1Q13, McDonald’s posted revenue growth of +0.9% on systemwide sales growth of 0%. One month into the second quarter, MCD systemwide sales have decreased -0.4%. The Street is expecting 3% revenue growth in the second quarter.

May and June will be crucial months for McDonald’s. A sequential acceleration in two-year average trends of 105 bps is needed to meet May consensus comparable sales growth in the U.S. So far this year, the two-year trend in U.S. comps has decelerated every month by an average of 83 basis points.

Long-Term Trend Remains Discouraging

Howard Penney

Managing Director

Rory Green

Senior Analyst