TODAY’S S&P 500 SET-UP – May 8, 2013

As we look at today's setup for the S&P 500, the range is 71 points or 4.12% downside to 1559 and 0.25% upside to 1630.

SECTOR PERFORMANCE

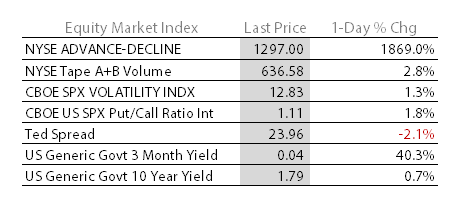

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.57 from 1.56

- VIX closed at 12.83 1 day percent change of 1.34%

MACRO DATA POINTS (Bloomberg Estimates)

- 7am: MBA Mortgage Applications, May 3 (prior 1.8%)

- 8:30am: Fed’s Stein speaks at Chicago Fed conference

- 10:30am: DOE Energy Inventories

- 11am: Fed to purchase $3b-$3.75b debt in 2019-2020 sector

- 1pm: U.S. to sell $24b 10Y notes

GOVERNMENT:

- 9am: Congressional Progressive Caucus event w/ low wage workers employed under federal contracts, w/ Reps. Raul Grijalva, D-Ariz.; Keith Ellison, D-Minn.; Barbara Lee, D-Calif.; Rep. Jan Schakowsky, D-Ill.

- 9am: Mandiant CEO Kevin Mandia, Symentec cyber VP Cheri McGuire testify on Senate Judiciary Cmte panel on law enforcement, private sector responses to cyber threats

- 10am: Senate Health, Education and Labor Cmte votes on nomination of Thomas Perez to Labor sec

- 10am: House Natural Resources Cmte hearing on hydraulic fracturing

- 11:30am: House Oversight holds Benghazi hearing

- 11:30am: Sen. Chris Murphy, D-Conn., Rep. Mo Brooks, R-Ala., Rep. Tim Ryan, D-Ohio, participate in Alliance for American Manufacturing news conf. on supply chain vulnerabilities, natl security risks in defense industrial base

- Sanford defeats Colbert’s sister in South Carolina

WHAT TO WATCH

- Yahoo CEO Mayer said to seek ways to end Microsoft search deal

- Microsoft CFO search said to pit Windows’ Reller against Hood

- Sprint said to press Dish for details before its due diligence

- Fannie Mae settles investor accounting lawsuit for $153m

- Whole Foods raises annual forecast as same-store sales improve

- “Bullish” about acquiring regional food stores

- J.C. Penney reports 1Q prelim. sales drop below ests.

- Walt Disney 2Q adj. EPS, revenue beat estimates

- Electronic Arts projects annual profit exceeding analyst ests.

- WebMD’s CEO Redmond steps down as co. raises sales forecast

- Toyota forecasts profit will rise to 6-yr high on weaker yen

- China export gains spur doubts as U.S., Europe shipments fall

- Berkshire agrees to limit DaVita stake after weighing increase

- China’s CNPC said in talks to buy Brazil’s Barra for $2b

- Apple seeks documents on Android source code in Samsung lawsuit

- Bristol-Myers sues Genentech claiming “Cabilly” patents invalid

- Tom Mockridge is named CEO of Virgin Media on Liberty deal

- Ackman, Einhorn, Eisman to speak at Ira Sohn conference

EARNINGS:

- Calfrac Well Services (CFW CN) 6am, C$0.50

- Susser Holdings (SUSS) 6am, $(0.05)

- Lamar Advertising (LAMR) 6am, $(0.03)

- Cognizant Technology Solutions (CTSH) 6am, $0.93

- Calumet Specialty Products (CLMT) 6:30am, $1.03

- Franco-Nevada (FNV CN) 6:30am, $0.27

- Starwood Property Trust (STWD) 6:45am, $0.46

- Intact Financial (IFC CN) 6:55am, $1.32

- CommonWealth REIT (CWH) 7am, $0.73

- Wendy’s (WEN) 7am, $0.03

- Enbridge (ENB CN) 7am, C$0.52

- AOL (AOL) 7am, $0.45

- Genivar (GNV CN) 7am, C$0.35

- Huntington Ingalls Industries (HII) 7:15am, $0.85

- Sodastream (SODA) 7:30am, $0.65

- Geo Group (GEO) 7:30am, $0.38

- Tim Hortons (THI CN) 7:30am, C$0.61

- Cedar Fair (FUN) 7:35am, $(1.20

- Brookfield Renewable Energy (BEP-U CN) 8am, $0.17

- Vivus (VVUS) 8:15am, $(0.52)

- Allete (ALE) 8:25am, $0.75

- Liberty Interactive (LINTA) 11:45am, $0.19

- News Corp (NWSA) 4pm, $0.35 - Preview

- Linamar (LNR CN) 4pm, C$0.60

- Cousins Properties (CUZ) 4pm, $0.12

- Green Mountain Coffee Roasters (GMCR) 4pm, $0.73

- Tower Group International (TWGP) 4pm, $0.53

- Groupon (GRPN) 4pm, $0.03

- Quebecor (QBR/B CN) 4pm, C$0.61

- Rackspace Hosting (RAX) 4pm, $0.20

- Quantum (QTM) 4:01pm, ($0.01)

- St Joe (JOE) 4:01pm, $(0.01)

- Sunoco Logistics Partners (SXL) 4:01pm, $0.82

- MarkWest Energy (MWE) 4:01pm, $0.26

- Polypore International (PPO) 4:01pm, $0.41

- Tumi (TUMI) 4:01pm, $0.15

- MBIA (MBI) 4:01pm, $0.15

- Andersons (ANDE) 4:01pm, $0.87

- J2 Global (JCOM) 4:03pm, $0.65

- Tesla Motors (TSLA) 4:03pm, $0.04 - Preview

- CenturyLink (CTL) 4:04pm, $0.68

- Activision Blizzard (ATVI) 4:05pm, $0.11 - Preview

- Monster Beverage (MNST) 4:05pm, $0.46

- Dealertrack Technologies (TRAK) 4:05pm, $0.26

- Clean Energy Fuels (CLNE) 4:05pm, $(0.06)

- SemGroup (SEMG) 4:05pm, $0.36

- Shutterstock (SSTK) 4:05pm, $0.16

- McDermott International (MDR) 4:10pm, $0.14

- Corrections of America (CXW) 4:10pm, $0.48

- Finning International (FTT CN) 4:14pm, C$0.47

- Veresen (VSN CN) 4:14pm, C$0.05

- Schweitzer-Mauduit International (SWM) 4:15pm, $0.92

- CF Industries Holdings (CF) 4:15pm, $6.00

- Oiltanking Partners (OILT) 4:15pm, $0.41

- Hawaiian Electric Industries (HE) 4:15pm, $0.38

- RLJ Lodging Trust (RLJ) 4:25pm, $0.37

- Fifth Street Finance (FSC) 4:41pm, $0.28

- Regency Energy Partners (RGP) 4:45pm, $0.03

- Liberty Media (LMCA) 4:45pm, $0.41

- Energy Transfer Partners (ETP) 4:53pm, $0.46

- Transocean (RIG) 4:56pm, $0.99 - Preview

- Ctrip.com (CTRP) 5pm, $0.24

- American Financial (AFG) 5pm, $0.83

- Home Capital Group (HCG CN) 5pm, C$1.67

- Atlas Energy (ATLS) 5pm, $(0.01)

- Atlas Resource Partners (ARP) 5pm, $0.23

- Sun Life Financial (SLF CN) 5:10pm, C$0.66

- Energy Transfer Equity (ETE) 5:10pm, $0.53

- EPAM Systems (EPAM) 5:40pm, $0.34

- Alon USA Energy (ALJ) 5:45pm, $0.55

- Continental Resources (CLR) 5:48pm, $1.14

- Granite REIT (GRT-U CN) 5:51pm, $0.69

- Tronox (TROX) 5:56pm, $(0.21)

- Quad/Graphics (QUAD) 6:30pm, $0.15

- Crosstex Energy (XTEX) 7pm, $(0.25)

- Delek US Holdings (DK) 11pm, $1.18

- Middleby (MIDD) Aft-mkt, $1.31

- Trican Well Service (TCW CN) Aft-mkt, C$0.18

- Northland Power (NPI CN) Aft-mkt, $0.06

- Alon USA Partners (ALDW) Aft-mkt, $1.44

- Calloway REIT (CWT-U CN) Aft-mkt, C$0.45

- Northern Property REIT (NPR-U CN) Aft-mkt, C$0.50

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Iron Ore Seen Dropping by BHP as Supply Growth Tops Demand

- KKR to Goldman Breach Decade-Long Water Deal Dam: Commodities

- Gold Rises in New York Amid Signs of Physical Demand in China

- Copper Rises in New York After Gains in China Signal More Demand

- Gold Assets in Fund Paulson Holds Decline to Four-Year Low

- China’s Gold Purchases From Hong Kong Expand to Record in March

- Sugar Declines on Brazilian Harvest Progress; Coffee Retreats

- Rebar Advances After China’s Trade Performance Beats Estimates

- Gold Eroding Farmer Collateral May Boost Defaults: India Credit

- Carbon Rout Roiling Australia as Polluters Win: Energy Markets

- China Copper Imports Drop 21.1% Yoy as Demand Slows: BI Chart

- Copper Consumers Seen by Boliden Holding Very Low Stockpiles

- Fed Panel Warned of Farmland Bubble Amid Increasing Credit Risk

- Gold Imports by India Seen Topping 100 Tons for a Second Month

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

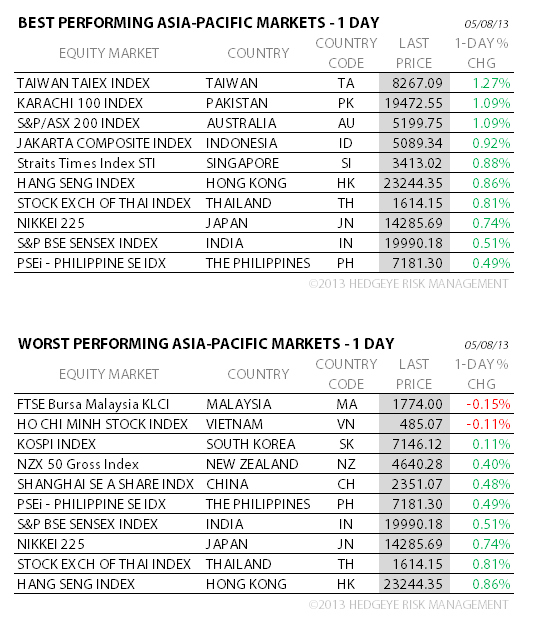

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team