Key Takeaways:

* XLF Macro Quantitative Setup – Risk reward appears to be short term negatively asymmetric. Our Macro team’s quantitative setup in the XLF shows 0.7% upside to TRADE resistance and 2.5% downside to TRADE support.

* Markit MCDX Index – The decline in muni risk is relentless. Last week spreads tightened a further 16 bps in the 16-v1 series MCDX, ending the week at 42.5 bps versus 59.2 bps the prior week. The Markit MCDX is a measure of municipal credit default swaps.

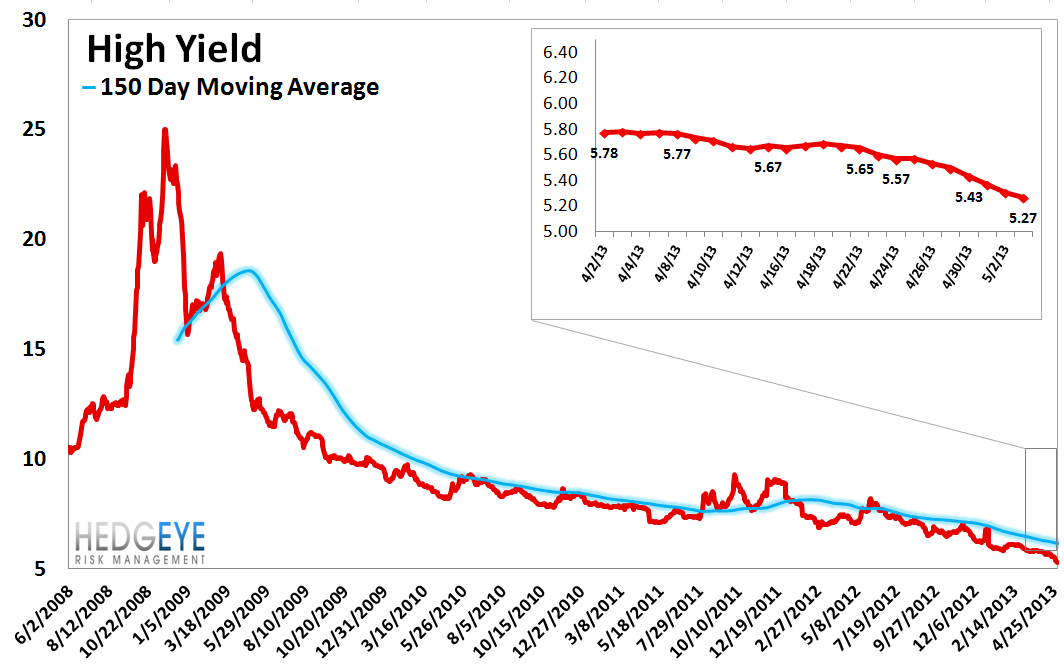

* High Yield (YTM) – The market continues to jump into the HY pool head first, as rates fell 27 bps last week, ending the week at 5.27% versus 5.53% the prior week.

* European Financial CDS - Europe's financial system continues to heal, in spite of the occasional headline to the contrary. With the exception of one Greek bank, all European Financials saw swaps tighten. Big moves came in Spain, Italy, France and the U.K.

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 7 of 12 improved / 0 out of 12 worsened / 6 of 12 unchanged

• Intermediate-term(WoW): Positive / 7 of 12 improved / 2 out of 12 worsened / 4 of 12 unchanged

• Long-term(WoW): Positive / 7 of 12 improved / 0 out of 12 worsened / 6 of 12 unchanged

1. U.S. Financial CDS - Aside from MBIA, all domestic financials tightened. MS, GS and BofA tightened by 12, 10 and 10 bps, respectively. Mortgage Insurers continued their relentless advance, dropping by 42 and 35 bps, respectively (MTG & RDN). Overall, swaps tightened for 26 out of 27 domestic financial institutions.

Tightened the most WoW: ALL, AXP, SLM

Widened the most/ tightened the least WoW: MBI, CB, TRV

Tightened the most WoW: RDN, MTG, AXP

Widened the most/ tightened the least MoM: MBI, PRU, MMC

2. European Financial CDS - With the exception of one Greek bank, all European Financials saw swaps tighten. Big moves came in Spain, Italy, France and the U.K.

3. Asian Financial CDS - Indian banks saw sharp drops in credit default swap premiums. Chinese banks were narrowly tighter, while Japanese banks were mostly unchanged. Daiwa and Nomura, however, both saw swaps drop by 10 and 9 bps, respectively.

4. Sovereign CDS – Sovereign swaps were tighter around the globe last week with the largest improvements coming in Portugal (-40 bps), Spain (-25 bps), and Italy (-20 bps). The U.S. tightened by 2 bps to 32 bps, while Germany and Japan were unchanged.

5. High Yield (YTM) Monitor – High Yield rates fell 26.8 bps last week, ending the week at 5.27% versus 5.53% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 3.6 points last week, ending at 1799.64.

7. TED Spread Monitor – The TED spread rose 0.4 basis points last week, ending the week at 22.71 bps this week versus last week’s print of 22.26 bps.

8. Journal of Commerce Commodity Price Index – The JOC index fell -0.7 points, ending the week at 4.63 versus 5.3 the prior week.

9. Euribor-OIS Spread – The Euribor-OIS spread tightened by 1 bps to 13 bps. The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

10. ECB Liquidity Recourse to the Deposit Facility – Deposits were relatively unchanged week-over-week. The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis.

11. Markit MCDX Index Monitor – Last week spreads tightened 16 bps, ending the week at 42.5 bps versus 59.2 bps the prior week. The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on six 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. We track the 16-V1.

12. Chinese Steel – Steel prices in China fell 0.1% last week, or 3 yuan/ton, to 3571 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened to 146 bps, -1 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 0.7% upside to TRADE resistance and 2.5% downside to TRADE support.

Joshua Steiner, CFA