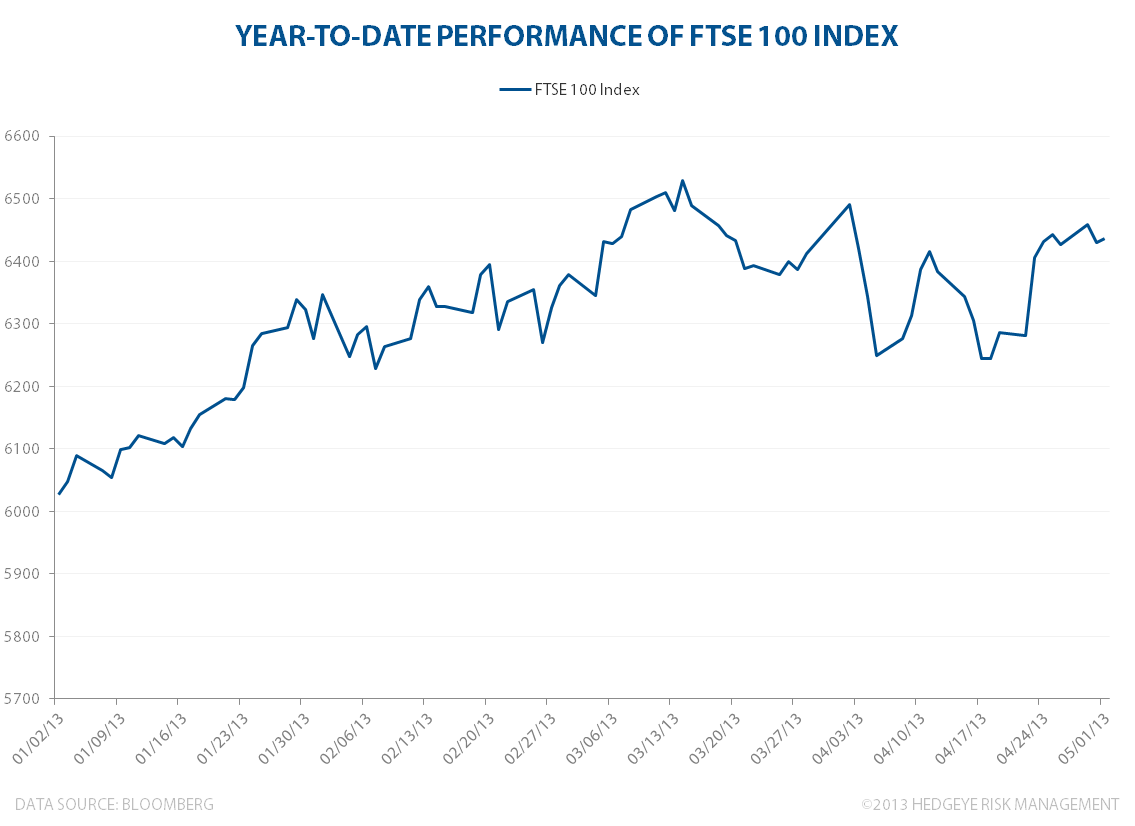

The FTSE 100 Index, which is essentially London's version of the Dow Jones Industrial Average, is doing quite well for the year-to-date. The index is up +11% compared with the Dow, which is up +12.7% year-to-date. This morning's economic data in the UK was the manufacturing Purchasing Managers Index (PMI), which came in at 49.8 for April versus 48.3 in March. That positive news has kept the FTSE in bullish formation and we expect the index to rise higher over the next month.