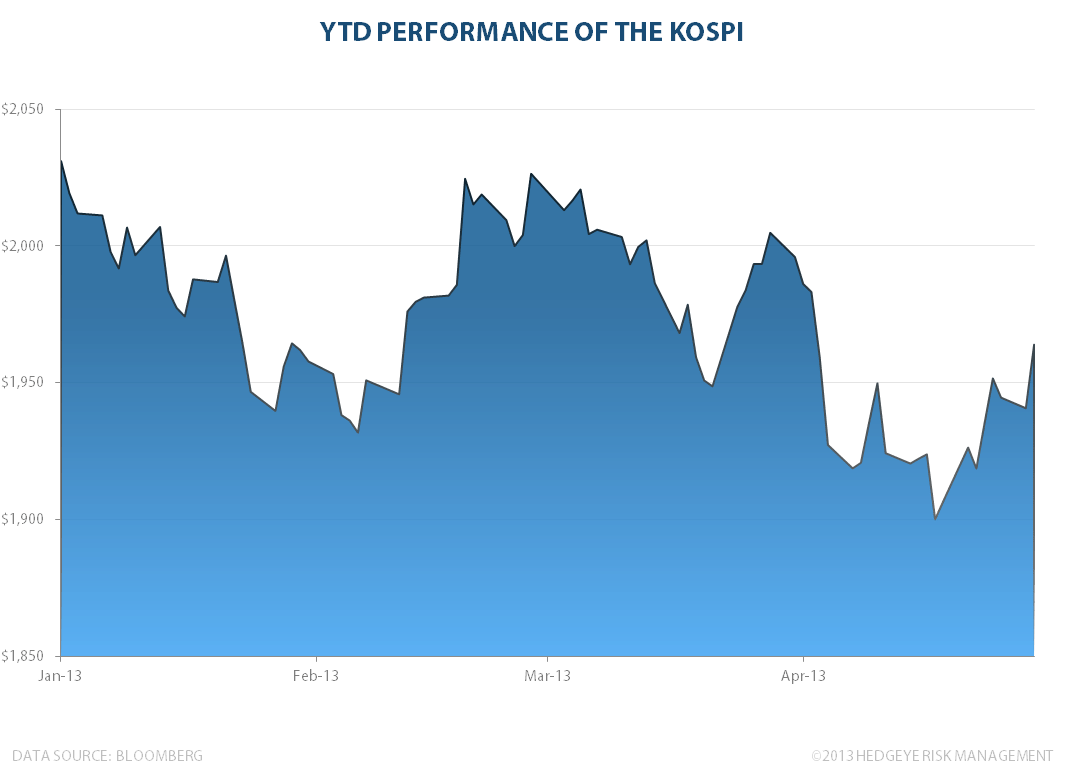

Korea's KOSPI index is heavily tied to the performance of severa outside factors, including the value of the Japanese Yen and the US tech sector. So with the S&P 500 hitting new all-time highs, it should come as no surprise that the KOSPI was up +1.2% this morning, heading above our TREND line of resistance at 1943 and closing at 1963. If the rally in US tech stocks can hold and the Yen can shield its fall from grace, expect more good times for the KOSPI.