On Thursday the ECB convenes to discuss an interest rate cut. This is a highly anticipated meeting, with 43 of 70 Bloomberg economists estimating a 25bps cut to the main refinancing rate (to 0.50%), 26 of 70 on HOLD, and 1 of 70 forecasting a 50bps cut. The last major inflection point in ECB policy came in the September 2012 meeting in which Draghi announced the OMT facility. Since then our call has been for no change in rates.

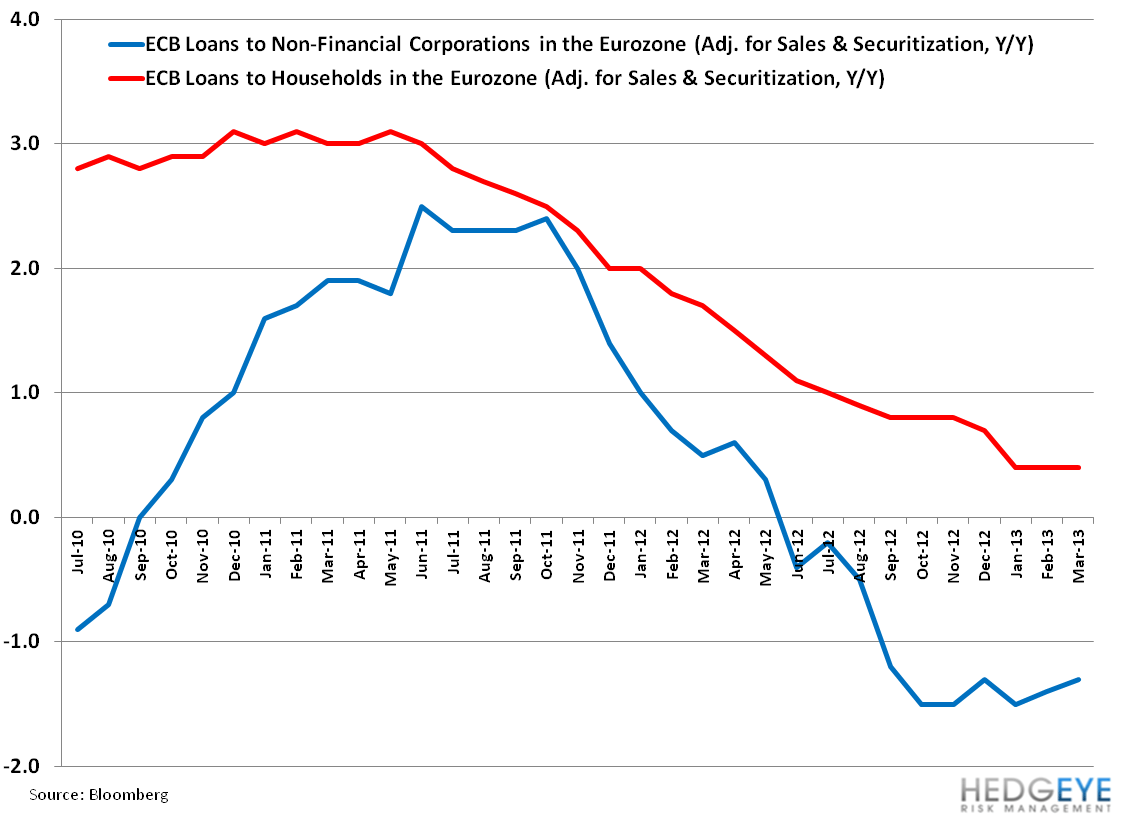

We’ve been calling for an interest rate cut in 2H 2013 but think the probability of a 25bps cut has gone up in recent weeks and it may come as soon as this Thursday. In the Early Look today Keith noted that the EuroStoxx600 outperformance last week, closing +3.7%, is one indication of increased expectations around a cut. That said, we’re less optimistic that a cut will be an outright panacea to the real economy that shows (among other factors) lending activity clogged (chart below), even if fundamentals are beginning to show a bottoming process.

We continue to expect the ECB to move in a reactive fashion and therefore to save its powder until economic conditions get noticeably worse. Assessing where we’re at on the front shows a mixed picture:

Of the positive signs (= no rate cut): Cyprus is rear view; Slovakia is out of sights (for now at least); Italy formed a coalition government (confidence vote pending); the European Commission (alongside the key Eurocrats) remain dovish and positioned to extend deficit targets (in Spain, France, Portugal, to name a few) and lessen the bite of austerity; there’s an improved risk picture, with 10YR sovereign yields across the periphery at some of their lowest levels in years (Italy hit 3.94%, this morning!), and bond issuance YTD has largely been priced at lower yields. Equities continue to reflect weekly headline risk, but here again we see continued support behind Draghi’s OMT to prevent an exit of any countries and stabilize the EUR.

Of the negative signs (= rate cut): high frequency data continues to show that the bottom may not in fact be in. For example, Eurozone confidence figures out today were all down versus consensus and last month’s print. Political and sovereign risk remains high in Spain, Portugal, and Italy given the tenuous popular support for governments and the impact of Austerity’s Bite.

EUR-USD

If the ECB cuts the main interest rate, we believe that’s bad for the EUR, good for the USD, and bad for commodities, which is in turn good for the consumer.

Our critical quantitative lines on the EUR/USD are outlined in the chart below. Beyond immediate term TRADE support of $1.29 we do not see any meaningful support until around $1.22.

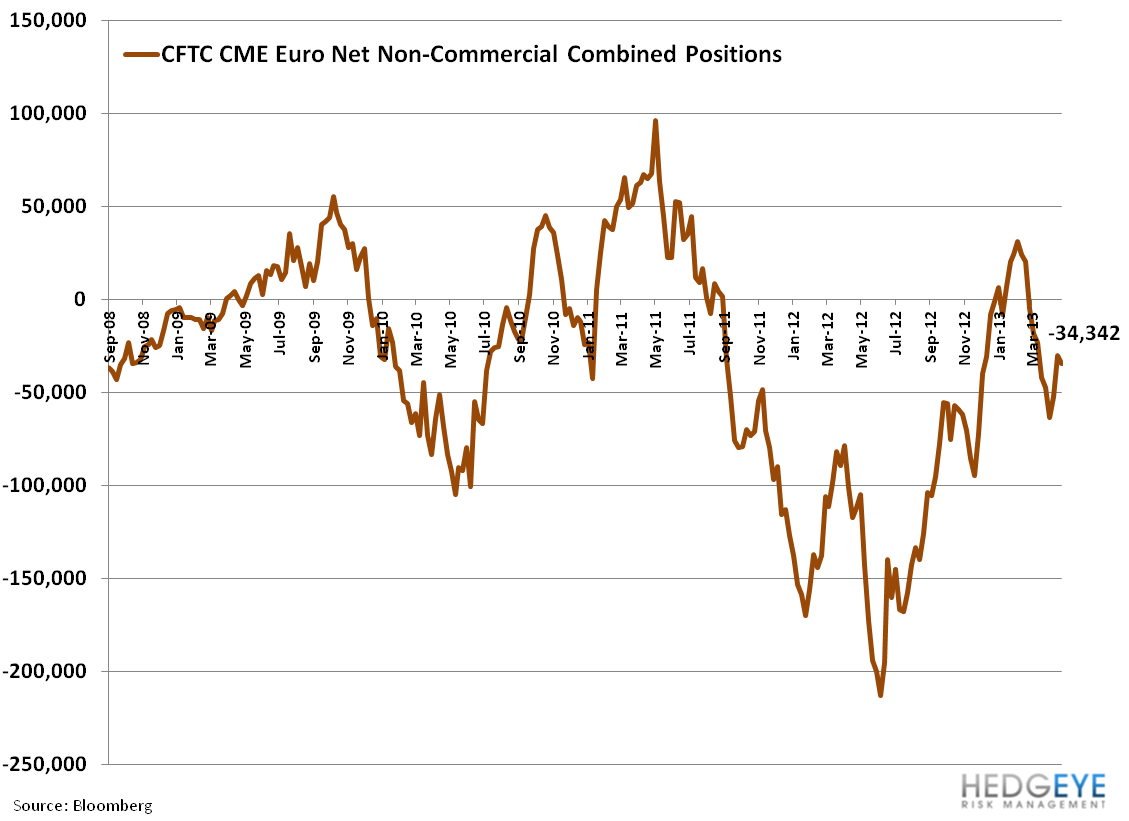

The most recent weekly CFTC data is somewhat stale (from 4/23) but shows that April has largely been a less bearish month for the cross.

Without a crystal ball we will be waiting and watching for market price signals into Thursday.

Have a great week!

Matthew Hedrick

Senior Analyst