Belying the broader slowdown in the domestic macro data in March is the continued improvement in the principal Household Balance Sheet and Income Statement metrics we've been focused on relative to our view on consumption – specifically, Housing & Employment.

Housing: Home prices have continued along their path of parabolic acceleration while the prevailing trend of strong demand and tight supply continues to support our bullish expectations for ongoing Home Price Appreciation over the intermediate term.

While Home price acceleration has been discrete, the market has shown some recent (apparent) disappointment with the volume of residential real estate activity. As our head of Financials, Josh Steiner, recently commented following the release of the March Existing Home Sales data, we think this concern is misplaced:

“There's a paradox of inventory right now. On the one hand, low inventory precipitates rising prices, while on the other hand low inventory marginally constrains volume growth. All things equal, low inventory helps the housing market far more than it hurts. In other words, the market should be more focused on prices rising due to tight inventory than on volume going sideways for the same reason”

So, in the context of our view of Housing as a Giffen Good, price should be the key metric of investor focus as price growth serves to drive demand in a reflexive cycle. Capacity will follow rising demand on a lag in the new home market and rising prices should drive existing home transaction volumes as housing equity turns positive for underwater borrowers alongside rising home values.

Recapping the recent housing data:

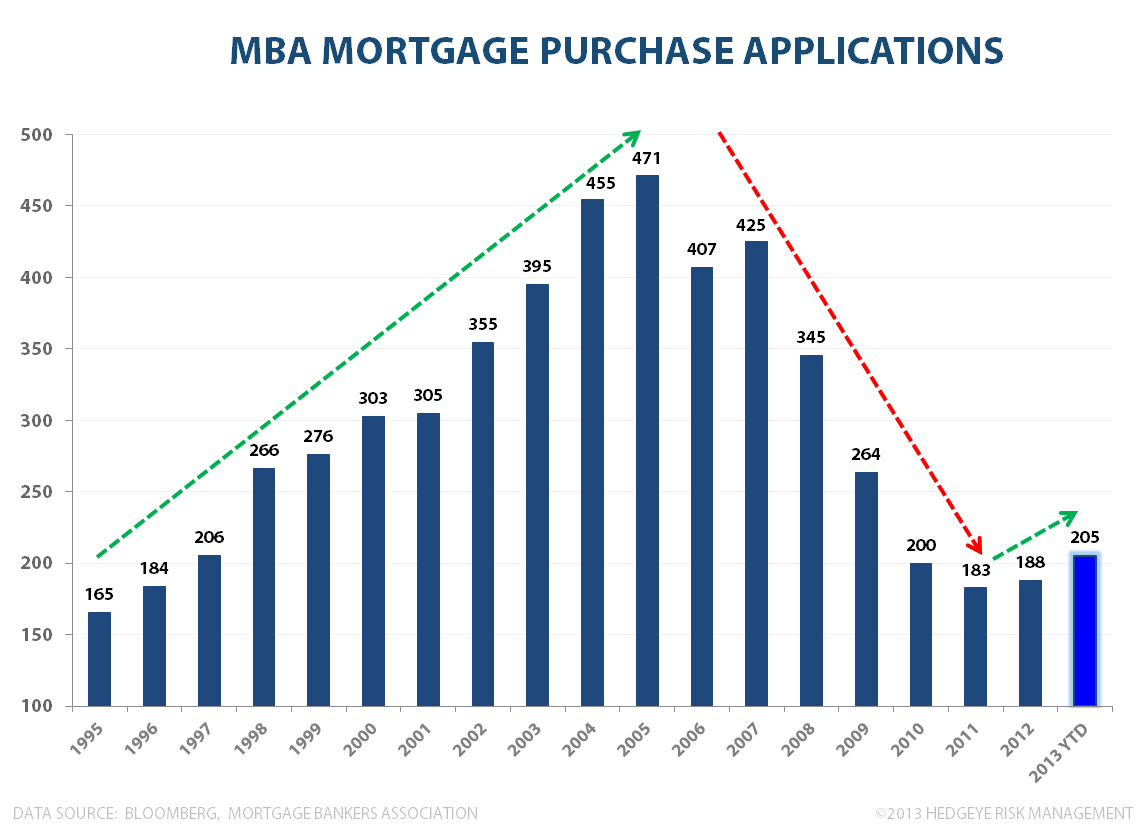

- Mortgage Purchase Applications: Mortgage Purchase Applications are showing no signs of slowing with this week’s data registering another higher YTD high.

- Existing Home Sales: Inventory was largely unchanged in March at 1.93M units, just north of the recent trough. Median Home Prices rose 11.8% y/y, the fastest rate of growth since November 2005.

- New Home Sales: New Home Sales rose 18.5% Y/Y in March to 417K units. From a mean reversion perspective, if new home sales as a percentage of total home sales returns to it’s 1 average, new home sales could double from current levels. With household formation trends currently tracking at ~2.0M in implied demand, and new housing starts running at 1M, both mean reversion and organic demand should support ongoing strength in the New Home market.

- Corelogic & FHFA Home Price Index: Preliminary Corelogic data for March estimates home prices grew 10.2% y/y, flat with growth in February, and up from 9.41% y/y growth in January. Yesterday's FHFA Home Price index data reflected similar trends with prices accelerating 70bps m/m to 7.07% y/y growth in February, marking the fastest pace of growth since November 2009.

- NAHB Homebuilder Survey: The NAHB Homebuilder HMI index registered a third consecutive month of softening, declining from 44 to 42 in the latest April reading. The decline was almost exclusively related to concerns over cost pressure as material and labor input costs have risen alongside rising demand and emergent, marginal capacity constraint. We think the concern is largely misplaced with respect to the broader housing trends. Pricing trends are strong, organic demand should remain supportive, and capacity issues will be transient. We would also note that, historically, 6M Forward Expectations for activity always run at a positive spread to the composite index while the Current Traffic reading typically runs at a negative spread to the composite reading. The recent widening of those spreads is more reflective of a return to normal then it is an outlier divergence.

source: Hedgeye Financials

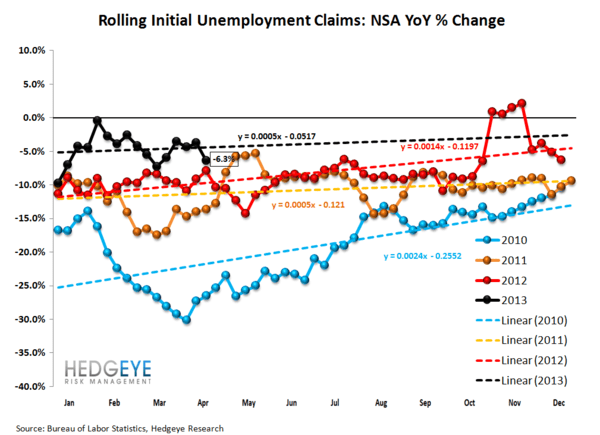

INITIAL CLAIMS: This week’s Initial Jobless Claims data was again positive with both the SA and NSA series showing sharp sequential improvement. We consider the 4-week rolling average in NSA claims to be the more accurate representation of the underlying labor market trend and on that metric, the trend improved 250bps w/w as the y/y change in 4-wk rolling claims went from -6.3% Y/Y from -3.8% Y/Y the week prior. The headline number fell 13K to 339K w/w versus the prior week’s unrevised number while the 4-week rolling average in SA claims dropped 4.5K w/w to 358K.

So, despite initial sequester related impacts beginning in April and the seasonal distortion in the seasonally adjusted data shifting to a headwind, labor market trends continue to show steady improvement. We continue to expect a ~10K drag on claims on a smoothed basis (with the potential for a negative shock to any given release) related to sequestration alongside the slow build in the negative seasonal impact through August.

source: Hedgeye Financials

Positioning: Strong Dollar – Strong Domestic Consumption remains the simplified Macro strategy playbook. The Dollar remains in Bullish Formation (Bullish across TRADE, TREND & TAIL Durations) in our Risk Management model and we expect further upside given our bearish view on the Yen, slowing growth and an increasingly dovish policy outlook in Europe, decent domestic economic data, declining federal deficit spending and an incrementally hawkish fiscal and monetary policy stance.

Continued USD appreciation should drive ongoing energy/commodity deflation, further relative underperformance in commodities and commodity levered exposure (XLB, XLE, Russia, Brazil, Peru, etc), and relative outperformance for domestic consumption oriented exposure (XLY, XLV) as discretionary share of wallet rises.

Keith bought the Dollar (UUP) and shorted Oil (OIL), Gold Miners (GDX), and Freeport-McMoran (FCX) in our Real-Time Alerts this morning.

Christian B. Drake

Senior Analyst