POSITION: 10 LONGS, 5 SHORTS @Hedgeye

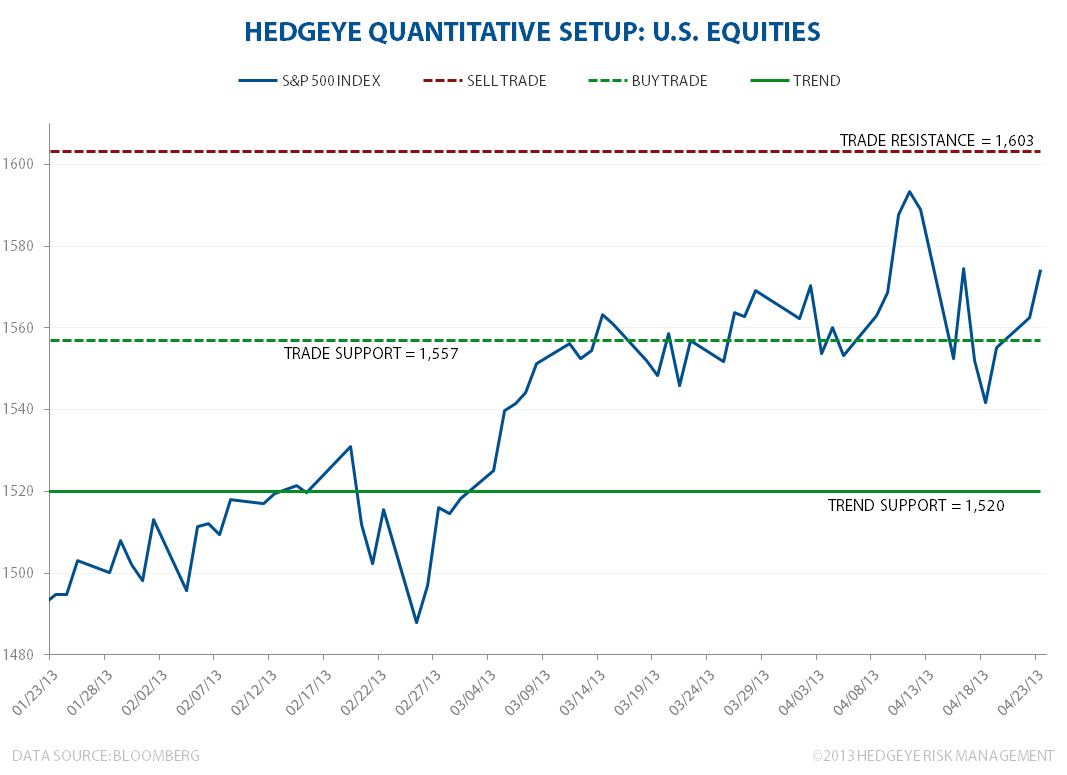

Below 1557 (TRADE bearish); above 1557, back to TRADE, TREND, and TAIL bullish. We call that a Bullish Formation.

If you want to get all beared up about something, short Bearish Formations (like Commodities or Mining Stocks).

Across our core risk management durations, here are the lines that matter to me most:

- Immediate-term TRADE resistance = 1603

- Immediate-term TRADE support = 1557

- Intermediate-term TREND support = 1520

In other words, I got longer (gross and net) as we crossed and confirmed 1557. Can we snap that again? Sure. And there aren’t any rules against selling on that again either. But remember, that’s all immediate-term talk.

From an intermediate (TREND) perspective, both the US economy (Consumption Growth) and the SP500 continue to look bullish.

If the SP500 tests 1603, the VIX will probably have a 10-handle. At least that’s what my model is telling me.

Prepare for what most consider improbable, when it becomes more probable.

KM

Keith R. McCullough

Chief Executive Officer