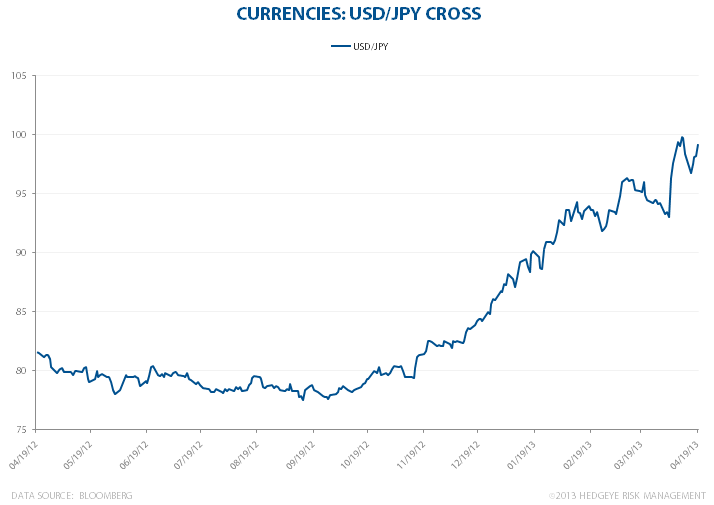

The Japanese Yen is down another -1.0% this morning versus the US dollar, hitting a new low. Japan's de facto currency has been devalued considerably over the past month (and beyond) as the country's central bank announced monetary stimulus plans that would help artificially boost the stock market whilst destroying the Yen.

Finance Minister Taro Aso and Bank of Japan Governor Haruhiko Kuroda have defended their actions, stating that the G20 nations will "understand" the need for stimulus. The Japanese people will likely have a hard time understanding why their food and gas prices have shot up; McDonald's recently announced it would be hiking burger prices by 20% due to commodity inflation.