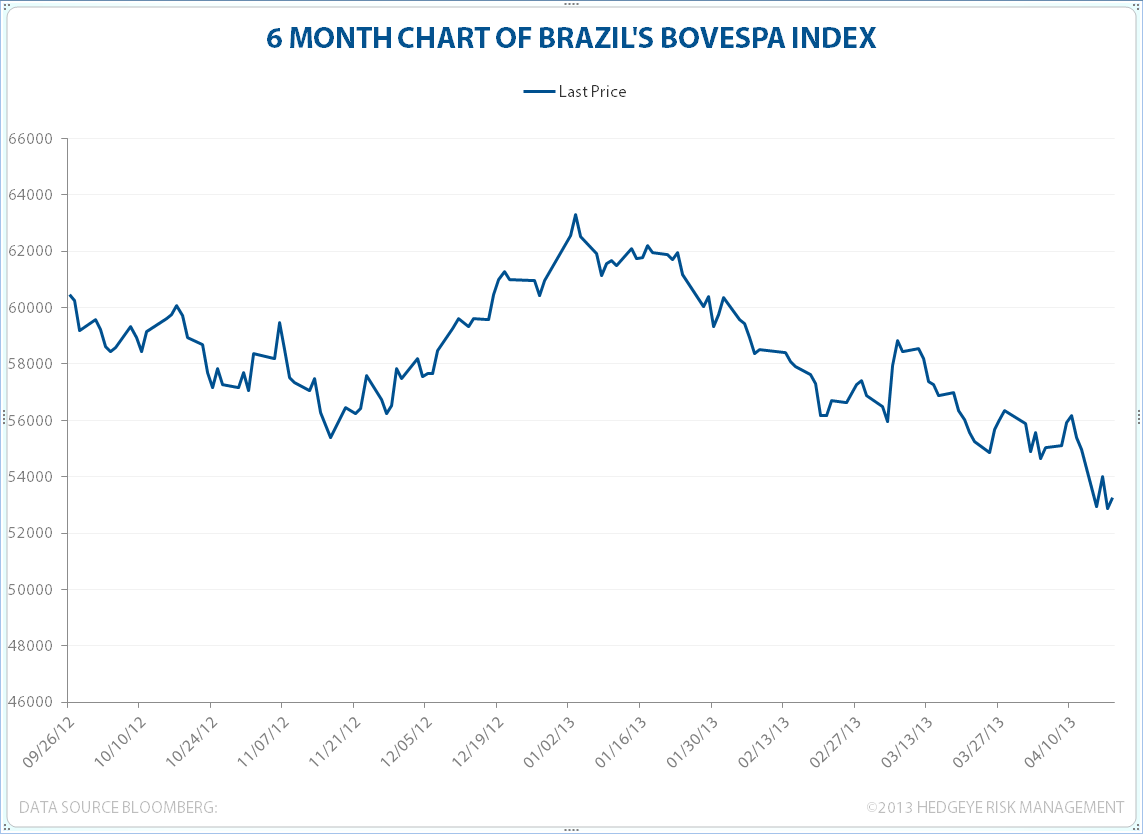

Brazil's BOVESPA Index dropped -2.1% yesterday and is down -13.4% year-to-date. One of the worst performing markets on the planet, the country just experienced a 0.25% rate hike to 7.5% on central bank borrowing rates by Alexandre Tombini, the governor of the central bank of Brazil. It's the first rate hike since July 2011 and has given investors plenty to worry about. We like staying short commodities and short Brazil through the iShares MSCI Brazil Index ETF (EWZ).