Conclusion: We're adding WWW to our Best Ideas list and think it's a 2-year double. We think that the prevailing bear case is weak and backward-looking, and that WWW has a little bit of everything that's needed for a long to attract new money and grind higher over a multi-year time period. Aside from having a high quality management team and a very consistent long-term track record, we think that new market share opportunity on a consolidated cost structure and asset base will accelerate organic growth, while taking incremental margins and returns higher. The ensuing cash flow will be used to de-lever, which provides a powerful kicker to propel earnings growth into the 20-30% range. Ultimately, we think that WWW has 3 to 1 upside/downside over the next 12/18 months.

The outline below is a summary of our investment case. We plan to release a Black Book with a deep-dive analysis over the next two weeks.

DETAILS

The bear case on WWW is simple. The company started to see a slowdown in its core footwear business, so it went ahead and did a transformational acquisition by paying a steep price for Collective Brands’ PLG division potentially near the peak of the cycle for its largest and most defendable brand – Sperry. Other brands like Saucony and Keds have upside, but are not in the 'great' category like Sperry arguably is. On top of that, the stock is trading at a high teens multiple on the company’s guidance. There are two realities associated with this bear case. 1) Most of it is correct. And 2) all of it is irrelevant.

First off, let’s look at the sentiment on WWW and all agree that people are more bearish on the name than we’ve even seen in the modern history of the company (ie even in the years not displayed by this chart). We’re likely seeing some covering on today’s print, but it still leaves the name in record bearish territory according to our sentiment monitor.

Secondly, we think that this bearish view is very backward looking and leaves out a big piece of the WWW story, which is that integration of these brands into the WWW portfolio will allow the former PLG group to achieve what it could not under its former owner (most notably – international growth, and leverage a more diverse selling infrastructure in the US). Furthermore it will grow without needing to add the capital we’d otherwise expect as a stand-alone company – especially given WWW’s consolidation from four divisions into three -- which improves asset turns and RNOA. Specifically, our math suggests that in the three years following the initial acquisition year (where there will be outsized accretion) we should see the following…

a) The addition of over $700mm in revenue – split fairly evenly between the Performance and Lifestyle groups.

b) $150mm in incremental EBIT (20% incremental margin on top of the 8.4% reported last year).

c) The asset base should remain relatively flat over that time period at about $3bn. The cash cycle can, and should, come down 20-30% from 2012 levels. There’s no reason why this business should have 115 days inventory and DSOs of over 60.

d) Over that same time period, interest expense should come down by 40% as WWW uses free cash to repay debt. As a result we should see shareholder’s equity double from $644mm ($13 per share) in 2012 to $1.3bn ($27 per share) in 2016.

e) Importantly, RNOA should climb from 10% up to 16%, with steady improvements each year. Admittedly, the one catch is that this is a company that once had returns of 30%. The PLG deal changed that – likely permanently (or at least for a very long time). Nonetheless, returns have bottomed and are headed up systematically. It's very important to note that it's near impossible to find an example where a company's RNOA roadmap went up (margins improving) and to the right (turns improving) simultaneously without the stock meaningfully outperforming peers.

In the end, we’re modeling 30%+ growth in earnings over each of the next two years, and 20%+ at a sustainable rate for at least the next three years. Our estimates are only 5% ahead of consensus this year, but by the end of our modeling time horizon (2016) we’re 25% ahead of the Street.

At the end of the day, this is probably one of the best managed and most consistent companies in retail. Accretion is ahead of plan, inventories are in very good shape, and though there is admittedly a permanent impediment to achieving asset turn levels WWW saw prior to the deal (acquiring as opposed to growing organically), WWW has a multi-year platform from which to grow. Add on accelerated cash flow generation and subsequent debt paydown, and we think that this story has legs (look at HBI over the past year – it’s the mother of deleraging stories. We’d put FNP in a deleregaing bucket as well – at least as it relates to expectations for proceeds from its asset sales.)

The stock is hardly washed out – we get that. But the reality is that this for a high quality globally diversified portfolio that has consistent 20-30% EPS growth and improving returns we don’t think that arguing a high teens multiple is a stretch. 18x our 2014 estimate of $3.55 gets us to a $64 stock, or 36% above current levels. Take that out to 2015 and 2016 and we’re looking at $75 and $95, respectively. When we juxtapose that alongside 15x ehat we think is a worst case $2.50 in EPS power, we’re looking 3 to 1 upside/downside over the course of a 12-18 months.

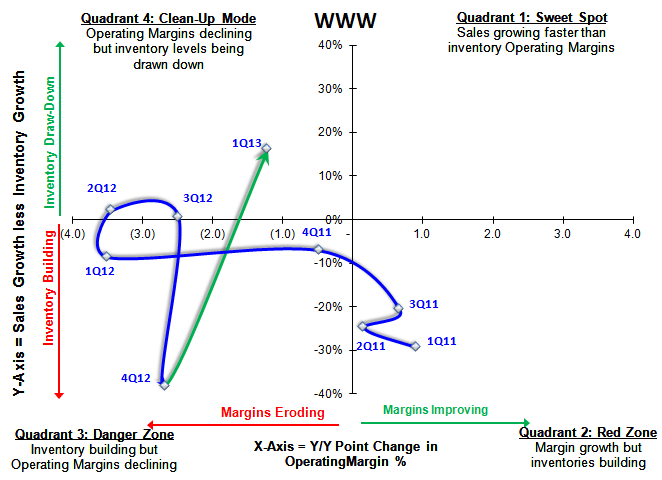

WWW SIGMA: Inventories are extremely clean, which has continued bullish implications for gross margins.