Yesterday we hosted our 2Q13 Macro Investment Themes call ( you can access the replay info HERE). Below is a visual review of the 1Q13 strategy playbook from the call: In short, strong dollar driven energy and commodity deflation is bullish for domestic consumption and negative for commodity leveraged exposure (XLE, XLB, Gold, Brazil, Russia, etc). We think this theme still has some legs in 2Q13.

(Prices as of 4/15/13)

Yesterday’s inflation and housing data typified this dollar based flow cycle and exemplified the macro dynamics we’d like to see persist for us to stay positive on domestic consumption. While housing starts breached the 1M threshold (note also that this morning’s mortgage applications index printed a new high & remains positive for forward housing activity), Headline CPI declined -0.2% M/M on the back of broad Food & Energy price deflation.

With the dollar in bullish formation (Bullish across TRADE, TREND & TAIL durations) and the U.S. economic data and forward policy outlook looking okay on an absolute basis and a bit better than okay on a relative basis, we expect the strong dollar - commodity deflation relationship to extend itself further.

Collectively, Energy and Food represent 24.26% of the CPI index and ~13.4% of personal spending (PCE). Given the persistent and generally strong inverse correlation between the dollar and Oil/Gasoline and the fact that the commodity settles in dollars, the flow through impact to price is rather direct.

Ag and Soft commodity prices, however, are hostage to a host of disparate influences that could predominate price trend over a given duration (think dollar strength, speculation, weather, etc). All else equal, the impact of a strong dollar on food prices should manifest disproportionately across foodstuff categories that are pure commodity with limited branding (no branding or large private label presence) and strong industry competition.

For food categories such as protein or select dairy where these strong dollar leverage dynamics exist (branded is proportionally lower and competition is multitudinous) the impact should be more apparent as price throughout the distribution chain should tend to more accurately and rapidly reflect current input price costs. We’re seeing some evidence of that in the March report and will continue to monitor the relevant food categories for ongoing impact.

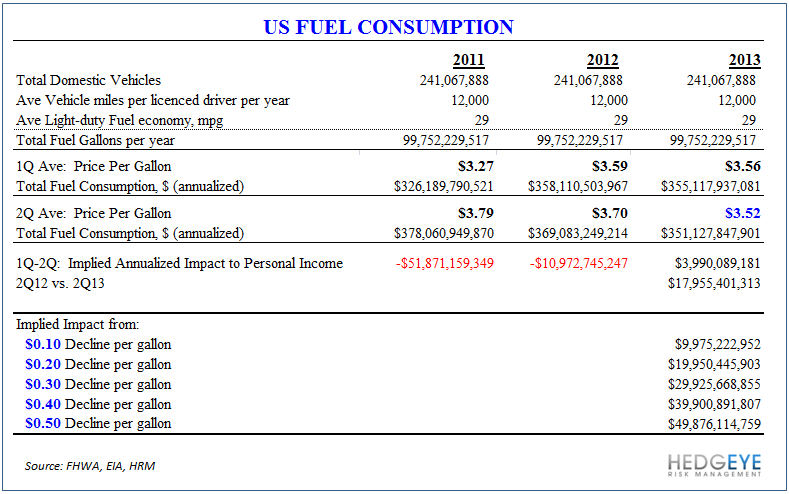

Households spend >$431B on gasoline and motor fuel on an annual basis which equates to approximately 3.8% and 2.7% of total household spending and GDP, respectively. The idea that lower gas prices support other discretionary consumption is intuitively appealing and stands as perhaps the most accessible example of scalable impact – a single consumer saving $5/wk at the pump is fairly insignificant, but multiplied and annualized across a registered vehicle base of 240 million and the numbers compound to something material rather quickly.

According to FHWA and EIA data, total registered vehicles, total vehicle miles, average vehicle miles per licensed driver and average fuel economy have been relatively stable in recent years. If we make the simplifying assumption of static totals for those metrics over the 2011-2013 period, it allows for a digestible, if imprecise, estimate of the implied impact of gas price changes on personal income and capacity for other discretionary purchasing. In short, each $0.10 decline in gas prices from the 1Q13 average level of $3.56 implies approximately $10B in increased capacity for other discretionary purchasing. On a year-over-year basis, the current national average gas price of $3.52 (vs. a 2Q12 average of $3.70) equates to an ~$18B annualized difference in non-fuel related spending capacity.

Notably, given the prevailing $USD strength and the accelerating collapse pervading the commodity complex, it appears likely we break the normal seasonal pattern of sequential acceleration in fuel prices from 1Q to the typical annual peak in 2Q.

This simplified view ignores price sensitivity of demand for gas consumption itself and the marginal propensity for other, non-fuel consumption, but it does provide a tractable framework for viewing the magnitude and direction impact of significant fuel price changes on the capacity for alternative consumer activity.

Collectively, some measure of housing wealth effect, emergent positive real earnings growth, the resolution of tax refund delays, and a real-time tax cut via fuel and food price deflation should help to buttress consumption in the face of tax law changes and concentrated, sequestration related fiscal drag impacts over the next couple quarters.

Christian B. Drake

Senior Analyst