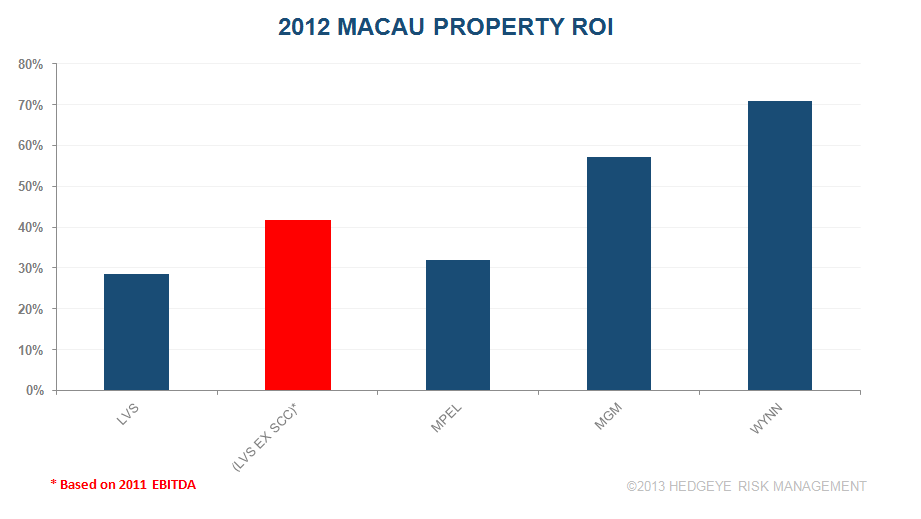

- WYNN leads the pack with an amazing 71% ROI (based on 2012 EBITDA) on Wynn Macau and Encore

- LVS’s $4 billion and climbing investment in Sands Cotai Central has depressed its ROI

- Peninsula investments earned much higher ROIs but Cotai still looks like a great investment