TODAY’S S&P 500 SET-UP – April 10, 2013

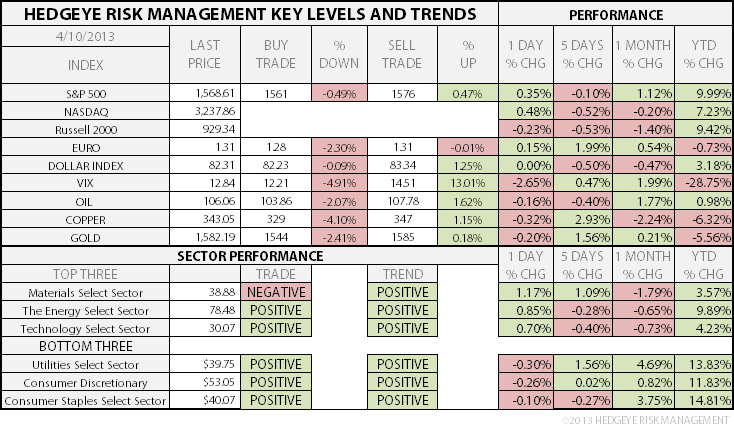

As we look at today's setup for the S&P 500, the range is 15 points or 0.49% downside to 1561 and 0.47% upside to 1576.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.54 from 1.52

- VIX closed at 12.84 1 day percent change of -2.65%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, April 5 (prior -4.0%)

- 7:30am: Fed’s Lockhart speaks at Atlanta Fed conference

- 8:45am: Bloomberg U.S. Economic Survey, April

- 10:30am: DOE Energy Inventories

- 1pm: U.S. to sell $21b 10Y notes in reopening

- 2pm: Monthly Budget Statement, March

- 2pm: Fed releases minutes from March 19-20 FOMC Meeting

- 5pm: Fed’s Fisher speaks on economy in El Paso, Texas

GOVERNMENT:

- 9:30am: Senate Homeland Security Cmte hears from U.S. Border Patrol Chief Michael Fisher, acting Customs chief Kevin McAleenan

- 10am: House Ways and Means hearing on govt’s ability to keep operating if Treasury reaches statutory debt limit

- 10am: House Energy and Commerce panel hearing on Keystone bill intended to bypass the need for a presidential permit for the pipeline’s construction; TransCanada’s Alexander Pourbaix, NRDC’s Anthony Swift among witnesses

WHAT TO WATCH

- President Obama sends budget plan to Congress

- Universal Entertainment’s Okada under U.S. criminal probe

- Swap users win staggered delays in Dodd-Frank reporting rules

- Apple said to discuss closer mobile collaboration with Yahoo

- Citigroup hires McKinsey’s Chubak to help Corbat pare expenses

- Home prices to decline in some cities as rates rise: Zillow

- Exxon to seek second MTBE win in New Hampshire appeal

- Microsoft says Surface tablet 2-yr warranty follows China law

- Deutsche Telekom tallies MetroPCS votes to weigh higher bid

- UnitedHealth units to pay $500m over hepatitis doctor

- China exports miss forecasts as “absurd” data defended

- Toyota says Corolla surpassed Ford Focus in 2012 global sales

- Yahoo CEO Mayer puts Reses in charge of talent management, M&A

- UBS plans to expand Asia corporate advisory headcount by 10%

- Navistar accused in suit of misleading on engine compliance

- APA expects offers for Australian gas pipeline in next week

EARNINGS:

- Family Dollar Stores (FDO) 7am, $1.22

- Fastental (FAST) 7am, $0.37

- MSC Industrial (MSM) 7:30am, $0.90

- Constellation Brands (STZ) 7:30am, $0.45 - Preview

- CarMax (KMX) 7:35am, $0.46

- Progressive (PGR) 8:12am, $0.44

- Bed Bath & Beyond (BBBY) 4:15pm, $1.68 - Preview

- Novagold Resources (NG CN) Aft-mkt, C$(0.03)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Halts Two-Day Advance as Supplies Rise to Three-Decade High

- Mine Town Rents Beating Manhattan Show Aussie Pain: Commodities

- Copper Drops as China Exports Fuel Concern Supply to Top Demand

- Gold Declines From One-Week High on Economic Recovery Outlook

- Wheat Drops as USDA Report May Show Higher Reserves; Corn Climbs

- Robusta Coffee at One-Week Low as Investors Sell; Cocoa Retreats

- Goldman Lowers Gold Price Forecast Through 2014 as Cycle Turns

- India Said to Consider Increasing Oilseed Prices to Boost Output

- China’s Crude Imports Fall to Lowest in Six Months in March

- Rebar Trades Near Two-Week High on Gain in Seasonal Demand

- Asian LNG Set to Rise as Premium at Two-Year Low: Energy Markets

- Gold in Yen Surges as Stimulus Erodes Currency: Chart of the Day

- Mechel Said to Consider Revising Plan to Sell Eastern Coal Asset

- Ex-Viterra Staff Join MAG Commodities to Trade Black Sea Grains

- China Gold Imports From Hong Kong Rebound on Decline in Prices

CURRENCIES

GLOBAL PERFORMANCE

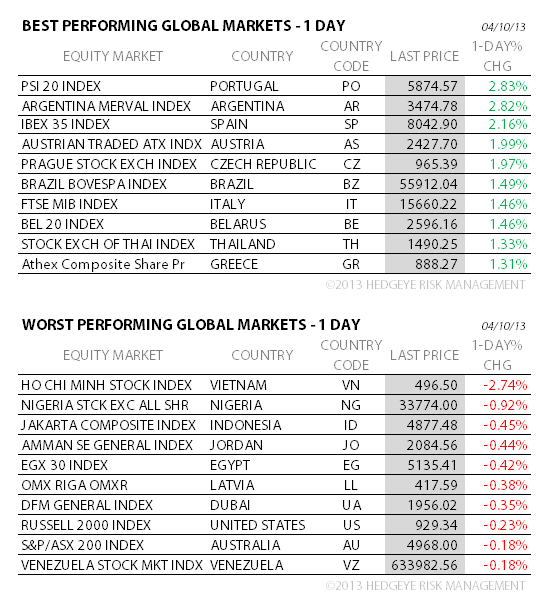

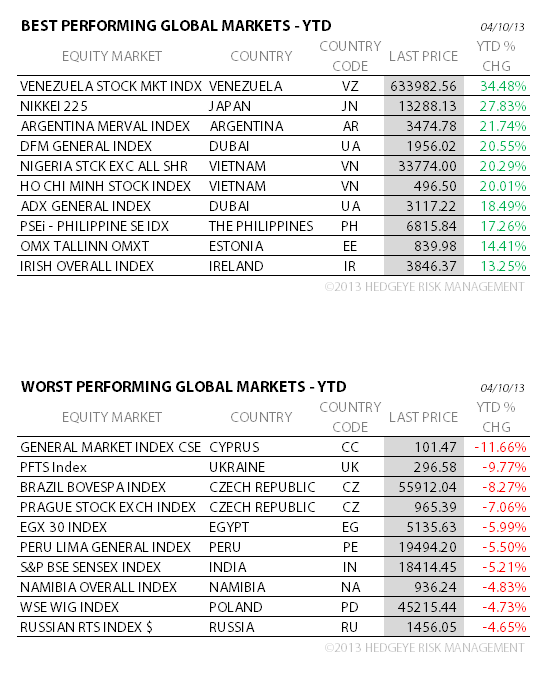

EUROPEAN MARKETS

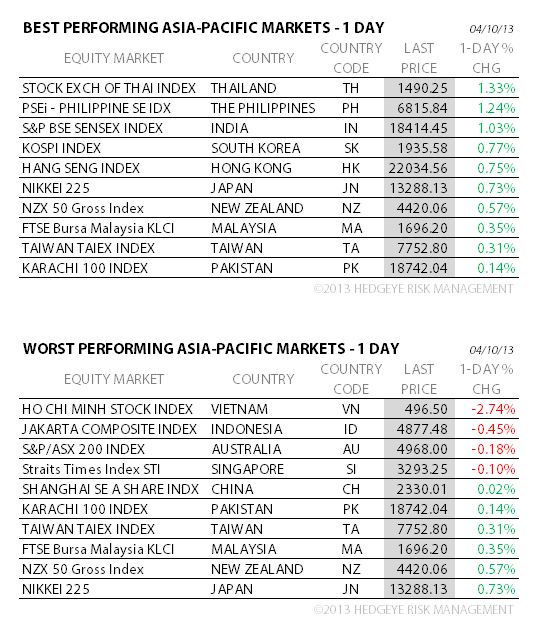

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team