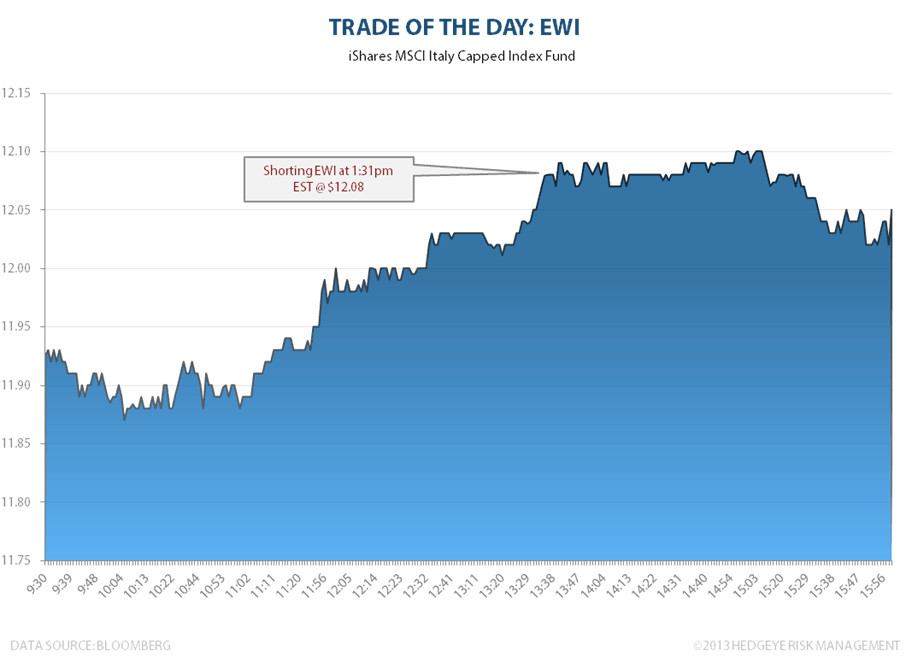

Today we shorted the iShares MSCI Italy Index ETF (EWI) at $12.08 a share at 1:31 PM EDT in our Real-Time Alerts. Back to the well as Italy bangs the top end of our risk range - bearish on the intermediate-term TREND duration. We'll cover when our signals tell us to. It's about sticking to your process and we're doing just that.