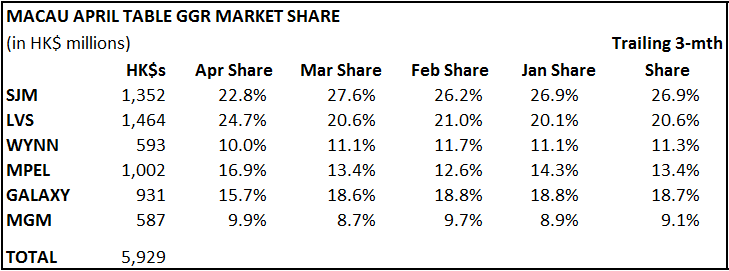

ADTR up 10% YoY - too early to make any calls

Daily table revenues (ADTR) averaged HK$847 million during the first 7 days of April, up 10% YoY. Our full month projection is for GGR of HK$26.5-27.5 billion which would represent YoY growth of 9-13%. MPEL and LVS are off to great starts. Still too early in the month to make any real conclusions about trends or market shares.