TODAY’S S&P 500 SET-UP – April 9, 2013

As we look at today's setup for the S&P 500, the range is 22 points or 0.77% downside to 1551 and 0.64% upside to 1573.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.49 from 1.49

- VIX closed at 13.19 1 day percent change of -5.24%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: NFIB Small Bus Optimism, March, est. 90.3 (prior 90.8)

- 7:45am: ICSC weekly sales

- 8:55am: Johnson/Redbook weekly sales

- 9:30am: Fed’s Lacker speaks in Richmond, Va.

- 10am: Wholesale Inventories, Feb., est. 0.5% (prior 1.2%)

- 10am: Wholesale Sales M/m, Feb., est. 1.5% (prior -0.8%)

- 10am: JOLTs Job Openings, Feb., est. 3.730m (prior 3.693m)

- 11am: Fed to purchase $1.25b-$1.75b notes in 2036-2043 sector

- 11:30am: U.S. to sell 4W bills

- 1pm: U.S. to sell $32b 3Y notes

- 1pm: Fed’s Lockhart gives remarks at Atlanta Fed conference

- 4:30pm: API energy inventories

GOVERNMENT:

- House, Senate in session

- Officials from OMB, European Commission meet to discuss regulatory compliance, U.S.-EU trade deal, 9am

- Senate Armed Svcs panel holds hearing on counterterrorism, defense authorization, 2:15pm

- Alberta Premier Alison Redford speaks at Brookings Inst on Keystone XL Pipeline, 2pm

WHAT TO WATCH

- Bernanke says Fed to press U.S. banks to cut liquidity risk

- J.C. Penney’s post-Johnson options seen to include sale

- Billabong to assess $299m buyout by Sycamore Group

- KPMG fires senior partner over alleged inside trading: NYT

- Warsaw exchange said to hold merger talks w/Vienna bourse

- Microsoft, Nokia complain to EU on Google’s Android dominance

- Chevron resuming Brazil output signals end to spill dispute

- First Solar holds analyst mtg, to face questions as Brown leaves

- China tightening pressure eases with March inflation

- New Hampshire asks MTBE jury for $236m from Exxon

- Microsoft Surface tablet warranty criticized in China

- Airbus juggles order book on record demand for A320neo jet

- German exports declined in Feb. amid euro-area recession

- Qantas targets Hong Kong approval for airline by year end

EARNINGS:

- Pricesmart (PSMT) 4:05pm, $0.77

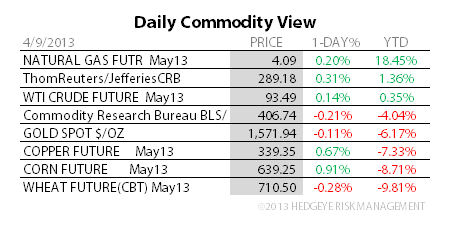

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Codelco Workers Begin Strike at Copper Mines for 24 Hours

- Corn Boom Goes Bust With U.S. Sales in Record Drop: Commodities

- Copper and Zinc Rise as China Inflation Eases Tightening Concern

- Corn Gains as Wet Weather May Delay U.S. Plantings; Wheat Falls

- Gold Swings as Investors Weigh Stimulus Against Recovery Signs

- Robusta Coffee Falls as Investors May Keep Selling; Cocoa Gains

- European Cocoa Processing Probably Dropped 2.4% in First Quarter

- Wheat Harvest in India Set for Record on High-Yield Seeds, Rains

- Crude Supplies Climb From 22-Year High in Survey: Energy Markets

- SGX Prepared for ‘Modest Pickup’ in AsiaClear Iron Ore Futures

- Killing Keystone Seen as Risking More Oil Spills by Rail: Energy

- Antofagasta Sees Copper Tight as Stock Climb Belies Price Bets

- Dinosaur Egg Carriers Losing Ground vs. Membrane LNG Tankers

- WTI Crude Advances a Second Day; Goldman Shifts Spread Forecast

CURRENCIES

GLOBAL PERFORMANCE

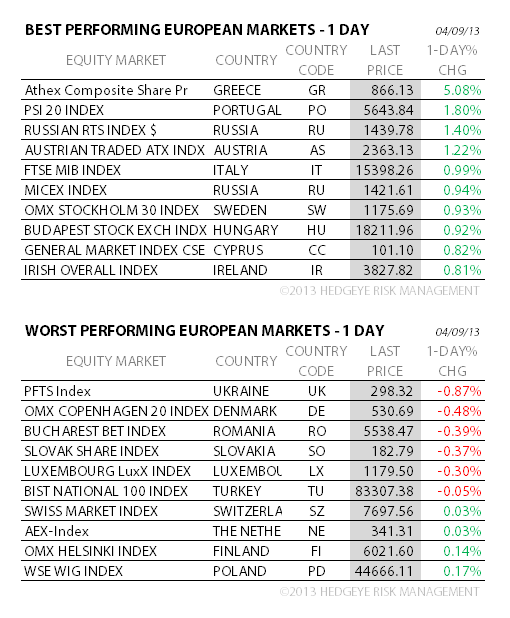

EUROPEAN MARKETS

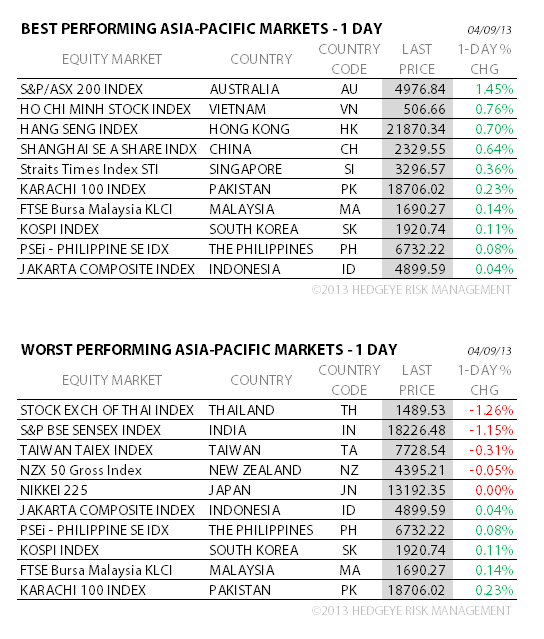

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team