Panera Bread’s stock has been upgraded two times in as many days and the stock has soared in response. We believe there is an opportunity to short PNRA at current levels for a trade (three weeks or less).

Fundamental Setup Less Positive (summary bullets)

- Traffic trends suggest that the consumer may be tiring of consistent price increases at Panera Bread

- Comp sales growth has become increasingly dependent on mix

- Total revenue growth continues to slow from the peak in 3Q11. 4Q13’s figure will be skewed because of an extra week

- Same-restaurant sales, margin guidance at risk

- Earnings estimates revisions unlikely to go higher absent sales acceleration

- Valuation is likely stretched at current levels

Traffic Trends

As the chart below illustrates, Panera’s traffic trends have been decelerating over the last three quarters. Embedded in some of the optimism in recent upgrades has been an idea that easier comparisons may play a part in better traffic trends in 2013. Traffic trends may improve sequentially but we see the 4Q traffic number, against an easy comparison, as an indication that Panera could have a traffic problem.

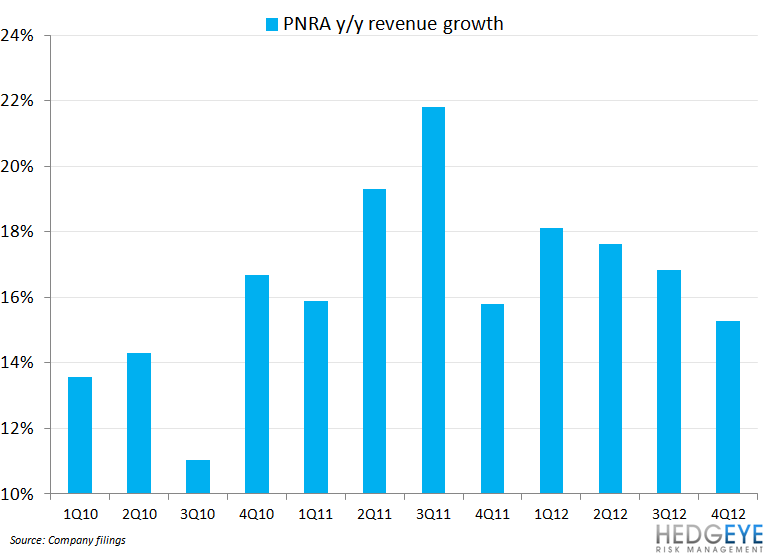

Revenue Growth

Along with traffic trends, total revenue growth has been decelerating for the three quarters, If this trend continues, we believe that the multiple implied in the stock’s price could compress (more below).

Comparable Sales Trends

The company has guided to company-owned same-store sales growth of 4.5% to 5.5% for fiscal 2013 and 4.0% to 5.0% for 1Q13. Consensus expectations are for the company to post 4.3% same-store sales and sequential improvement thru the balance of 2013. We believe there is sufficient risk to traffic expectations to bet against the sequential improvement that the Street is forecasting.

Earnings

Earnings revision growth has slowed and, absent meaningful acceleration in sales trends, there may be no additional upside to estimates. The company is guiding to 2013 EPS growth of 17-19%, inclusive of the 53rd week impact.

Valuation

We don’t anticipate any catalyst materializing to drive PNRA’s multiple higher over the next year. Particularly if our concerns about traffic growth are well-founded, it could be difficult to argue for a higher multiple. The last time the stock was trading a turn higher than current levels, on an EV/EBITDA basis, the company was posting high-single-digit same-restaurant sales growth and low-single-digit traffic trends. If traffic trends don’t accelerate, we believe that the multiple has significant downside.

Howard Penney

Managing Director

Rory Green

Senior Analyst