This note was originally published at 8am on March 20, 2013 for Hedgeye subscribers.

“There’s a kind of psychological ballet: who will outstare who?”

-John Vaillant, The Tiger

Sound familiar? After a 3-day correction of 1% from the YTD high in the SP500, look into my eyes and tell me how you really feel. And “you should not suddenly turn tail because the scent of fear passes quickly.”

“You must back off, slowly, slowly – especially if the tiger has a kill, or if she’s a mother with cubs: she makes a step, you make a step – you must not run away.” (The Tiger, pg 126)

To be clear, I remain bullish – and to the well known newsletter author (who sent me hate mail intraday yesterday) who wants me to roll-over and die… well, I say good luck. “Tigers will bluff-charge the same way bears do and, in most cases, all the tiger wants is an indication of submission.” (pg 150). If this market rips from here, I don’t want his apology – I just want him to publicly admit defeat.

Back to the Global Macro Grind…

I know, I know – fights are breaking out and it’s getting gnarly out there. Old Wall guys sending me emails, former Perma Bulls going bearish – it’s all out there right now. It’s a Psychological Ballet. And I like it.

I also liked buying on red yesterday. We bought the SP500 (SPY) after seeing the low-end of our immediate-term Risk Range (1538-1565) tested and tried. After 3 straight down days for US stocks, the US 10yr Bond Yield is down a whole 3 basis points.

End Of World (#EOW) or correction? Who will outstare who into month and quarter-end?

Let’s drop the Siberian tiger stuff and getting into the Global Macro meat of the matter (currencies, countries, fear, etc.):

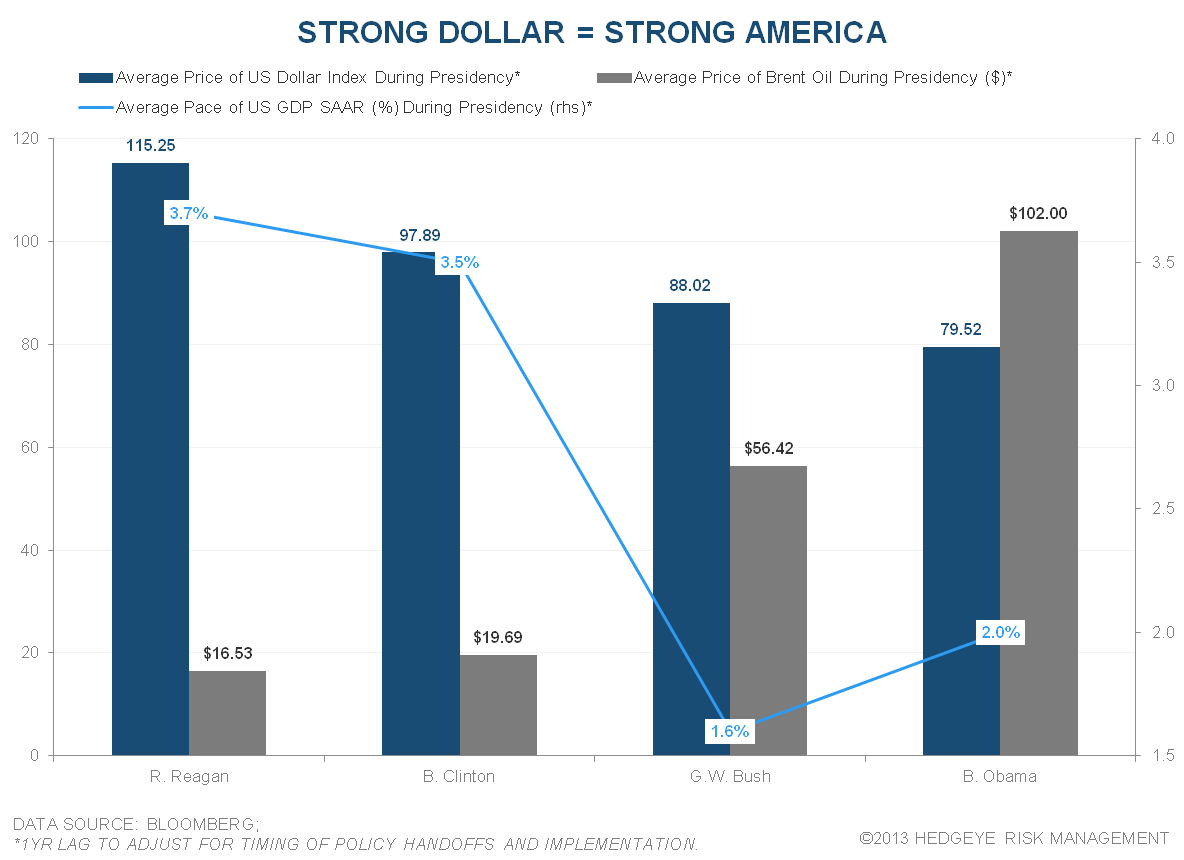

1. CURRENCIES: the fulcrum piece of our bullish case on Asian and US #GrowthStabilizing remains the US Dollar. What Cyprus Storytelling gave us this week was an even Stronger Dollar, and Weaker Oil. The US Dollar Index is now up for 6 of the last 7 weeks and, not ironically, the CRB Commodities Index is down for 6 of the last 7 weeks.

2. COUNTRIES: note that I wrote Asian and US #GrowthStabilizing; so, if you want to freak-out about Europe, just get over it and short Europe – but make sure you sell the right country (we prefer Italy, Russia, and France – in that order, short side). China’s Shanghai Composite ripped a +2.7% move overnight and Germany’s DAX is +0.8% testing 5-year highs. Not #EOW, yet.

3. VOLATILITY: the epicenter of fear is in both the front-month and term structure of US Equity Volatility (VIX). I’ve written about this exhaustively for 3-months because I want to be Fading Fear (buying High Short Interest, Shorting Gold, Shorting Treasuries, etc.). Front-month VIX just failed at immediate-term TRADE resistance of 14.74 and has no support to 10.77.

I could always smell them. Now that they are sending me idle threats of hereditary right, I can see the Old Wall very clearly now. So what is it, gentlemen? To be long or short of stocks here? Buy or sell? It really is an ok question to answer, transparently and accountably. I am watching you.

“There are two categories of people when it comes to extreme situations… One gets scared first, and then starts thinking; the other starts thinking first and gets scared after the fact. Only the latter survives in the taiga.” (The Tiger, pg 155)

Having made over 2,000 long/short calls (all #timestamped, since 2008), almost 50% of the calls I have made have been on the short side. Inclusive of having to manage plenty of risk to the upside, my batting average on the short side = 79.12%. So A) unlike some of these pundits, I get things wrong and B) I have no problem shorting markets when my process tells me to do so.

Fear of fiction or perceived top-calling wisdoms only computes one way into my process – as contrarian indicators. If it’s the Italian Election or Cyprus that you fear, I am not scared. If you’ve been bearish the whole way up and it’s your reputation you fear, I don’t blame you.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST10yr Yield, VIX, Russell2000, and the SP500 are now $1589-1613, $107.14-109.53, $82.61-83.29, 93.68-97.17, 1.89-1.97%, 10.77-14.74, 933-955, and 1538-1565, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer