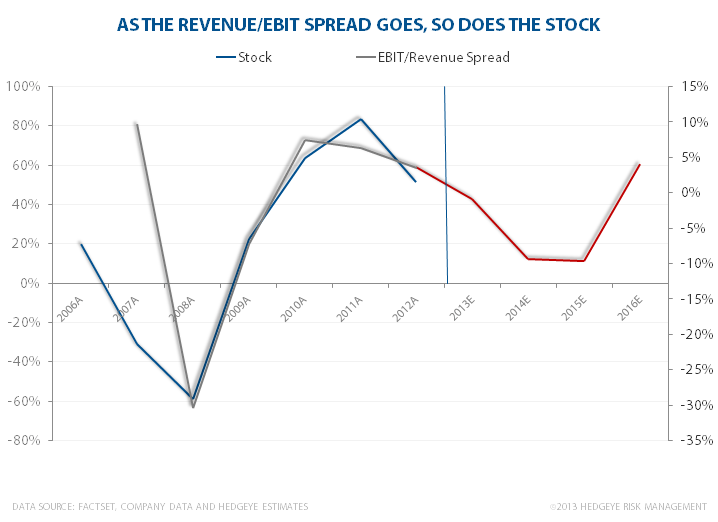

We think UnderArmour is seeing a nice pop in its first quarter performance at retail, buoying our view that there will be a bifurcation this year in the company’s earnings trajectory. The Street is at $0.03, we’re at $0.09, and the company earned $0.14 last year. We think that UA set itself up for a beat in 1Q, but then by 2H when it needs to rely on Footwear and International, we’ll see its EBIT growth rate slow down as it invests more SG&A to grow those newer businesses.

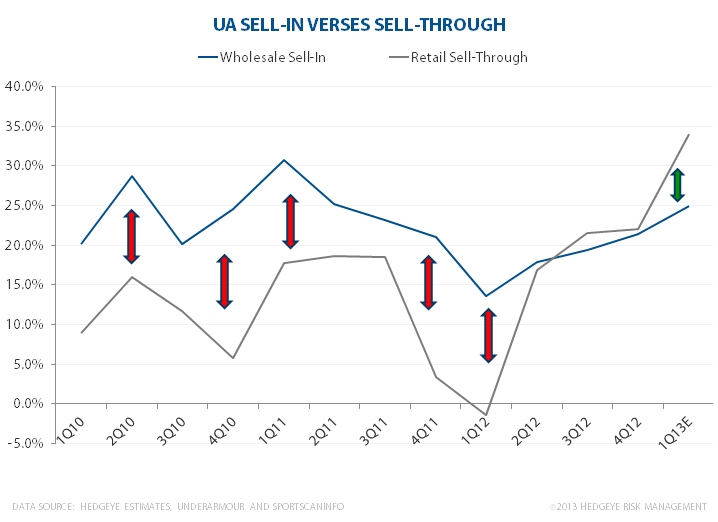

What gives us confidence in the first quarter? Simply put, for 10 quarters, UA’s wholesale sell-in to retail outstripped sell-thru by about 1,000bps. To get those numbers, we took total apparel sales, backed out International, e-commerce and company retail to get a true like-for-like US wholesale number. Then we compared to the weekly SportscanINFO sell-through data. That fueled an average Gross Margin decline of over 100bp over the past two years.

The good news is that in 1QTD, the retail sales data suggests that UA’s sell-through has been up near 30%. We should caution against simply jacking up UA’s top line in you model or taking up Gross Margins. Rather, this is the retailers clearing out inventory that has been building up for some time. But at a minimum, it should clear the way for the channel to accept Spring product at a clip sufficient enough for UA to deliver 20%+ growth in the upcoming quarter.

But Watch Out in 2H

We continue to think that UA will join the band of companies in the retail supply chain that is stepping up capital investment this year – both in capex and in SG&A -- but at the higher end. Growth in Footwear and International are both absolutely critical to UA’s aggregate top line. When that happens, we think that revenue and EBIT growth will diverge. If we’re wrong, then we think it is a matter of time until the top line slows, which would be even more damaging to UA’s multiple.

We still think that this is an exceptional brand, but simply think that it belongs to a company that needs to go through some growing pains before it could deliver upon the expectations currently embedded in the stock.

We think it’s more likely than not that earnings growth gets pushed out by a year sometime in 2H, and that investors should take advantage of this on or just after the 1Q print.