TODAY’S S&P 500 SET-UP – March 20, 2013

As we look at today's setup for the S&P 500, the range is 27 points or 0.67% downside to 1538 and 1.08% upside to 1565.

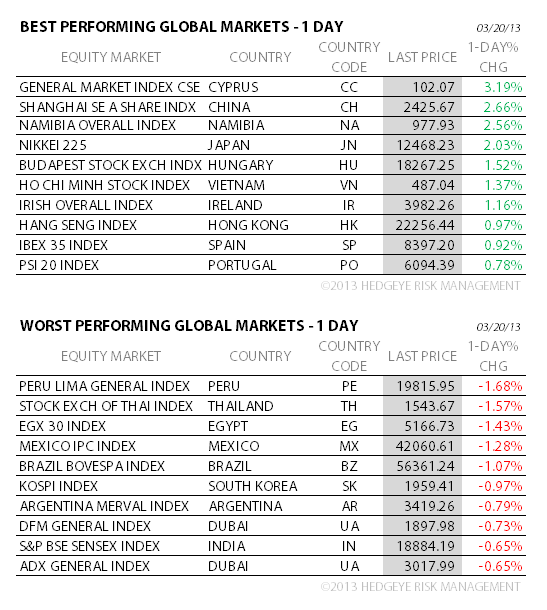

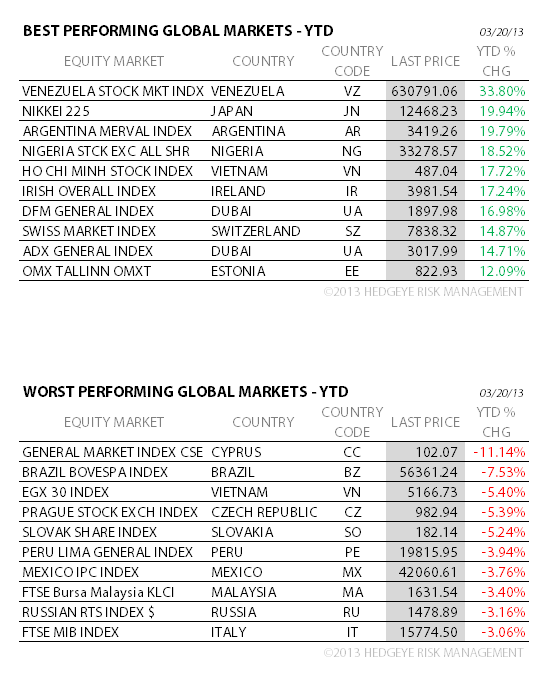

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.69 from 1.66

- VIX closed at 14.39 1 day percent change of 7.71%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, March 15 (prior -4.7%)

- 10:30am: DOE Energy Inventories

- 2pm: FOMC announces rate decision, releases summary of economic projections

- 2:30pm: Fed Chairman Ben Bernanke holds news conference

GOVERNMENT:

- Obama’s first visit to Israel; 3-day trip includes mtgs, news conferences with Palestinian Authority President Mahmoud Abbas, Jordanian King Abdullah II in Amman

- 10am: Sen. Judiciary Cmte hold hearing on domestic drones, law enforcement, privacy issues

- 11am: Interior Dept opens bids to lease 38.6m acres off coasts of La., Miss., Ala., for exploration that may tap 1b barrels of oil, 4t cubic feet of natural gas

- 2:30pm: FAA Admin. Michael Huerta, NTSB Chairman Debbie Hersman testify at Senate Commerce Cmte hearing on FAA’s safety initiatives and the effect of sequestration

- 3pm: Japan Intl Transport Inst forum on vehicle safety w/ speakers from NHTSA, Japanese regulator and Toyota

WHAT TO WATCH

- Bernanke seen keeping QE pace until 4Q as Fed meets

- Freddie Mac sues BofA, UBS, JPMorgan for alleged Libor rigging

- Europe weighs Cyprus’s fate after lawmakers reject bank levy

- BlackRock’s CEO Fink says Cyprus is not major problem

- HP holds annual meeting amid dismay over Autonomy purchase

- Apple may face sanctions in privacy suit over document sharing

- Hostess wins approval of asset sales of more than $800m

- MF Global trustee reaches agreement with JPMorgan

- Chesapeake trial over $1.3b bond call set for April 23

- Wall Street may win swap-rule reprieve in House legislation

- Vodafone said to be ready to accept lower debt rating on M&A

- Yahoo may buy stake in France Telecom’s Dailymotion: WSJ

- Norwegian Air plans follow-on order for stricken Boeing 787

- Transocean “should have done more” before blowout, CEO says

- Los Angeles to halt purchases of coal-generated electric power

EARNINGS:

- Lennar (LEN) 6am, $0.16 - Preview

- General Mills (GIS) 6:59am, $0.57

- FedEx (FDX) 7:30am, $1.38 - Preview

- Actuant (ATU) 7:30am, $0.37

- Herman Miller (MLHR) 4pm, $0.28

- Oracle (ORCL) 4:01pm, $0.66

- Tumi (TUMI) 4:01pm, $0.26

- Guess (GES) 4:03pm, $0.87

- Jabil Circuit (JBL) 4:30pm, $0.54

- Clarcor (CLC) After-mkt, $0.46

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Crude Oil Rebounds in New York After Biggest Drop in a Month

- Arabica’s Allure Returning for Roasters After Rout: Commodities

- Gold Trades Below Three-Week High as Investors Weigh Cyprus, Fed

- Gold Falls From Three-Week High as Investors Weigh Fed, Cyprus

- Wheat Gains on Signs of Increasing Demand, U.S. Weather Concerns

- Biggest Exporter Australia Increases Iron Ore Forecast on China

- European Council Votes to End Sugar Quotas in 2017, EU Says

- Physical Lead Market Seen by Macquarie Under Downward Pressure

- Rebar Rises for Second Day as Moving Average Signals Rebound

- Milk Jumps to Record on New Zealand’s Worst Drought in Decades

- Russia, Egypt Yet to Contribute to AMIS Farm-Commodity Database

- Wheat Buying by Bangladesh to Climb as Price Drop Boosts Demand

- Olam Shares Top Level Last Reached Before Carson Block Attacked

- Arabica Coffee Gains as Roasters May Switch Blends; Sugar Rises

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team