We think IGT is sandbagging the numbers. Nobody can accuse us of being eternal optimists. This is the first time we've made the claim that guidance was conservative and we did bring our numbers down to 25% below the Street on Monday in our note "IGT: PLENTY OF EARNINGS POWER FOR PATIENT INVESTORS". IGT guided below even our numbers. This is exactly what we hoped the company would do, especially with a new CEO taking over. Smart move, Patti. Now we'll see if she is the aggressive and unemotional cost cutter that we believe her to be. Move over TJ, aka Mr. Nice Guy.

We've scrubbed the model after the quarter and our estimates actually went...UP! Our financing projections changed to now assume a one year extension of the credit agreement combined with a new bond deal. Previously, we expected a bond deal and a completely new credit facility. Essentially, this strategy allows IGT to smooth the interest cost mark-up over 2 years versus our previous assumption of a year. We are now projecting fiscal 2008 and 2009 EPS of $0.87 and $0.89, respectively.

Now that the earning cat is out of the bag, the real story here is IGT's long-term core earnings power. The probability of earnings meets and beats are high, in our opinion, so what is the true earnings power? Our conclusion from our 4/21 note still holds: $1.40. However, given the pent up replacement demand, we are likely to see a v-shaped recovery and IGT "over earning" the $1.40 for a few years.

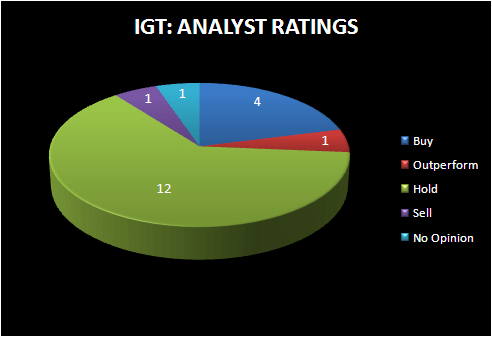

The market reaction to the awful quarter and guidance yesterday was to send the stock slightly higher. The bottom could be in. Estimates are likely to be met or exceeded. As shown below, only 5 out of 19 sell-side ratings are positive. Upgrades are coming, especially when they beat the next quarter. Finally, the valuation, even on our Street low 2010 estimate, is reasonable, and downright compelling on core EPS.