TCF Financial (NYSE: TCB) is one of our Financials Sector team’s favorite stocks on the long side. That’s because TCB, a bank holding company based in Chicago, stands to be a beneficiary of the overall recovery in the nation’s housing market. Now, TCB’s home market, Chicago, is really showing signs of life, too.

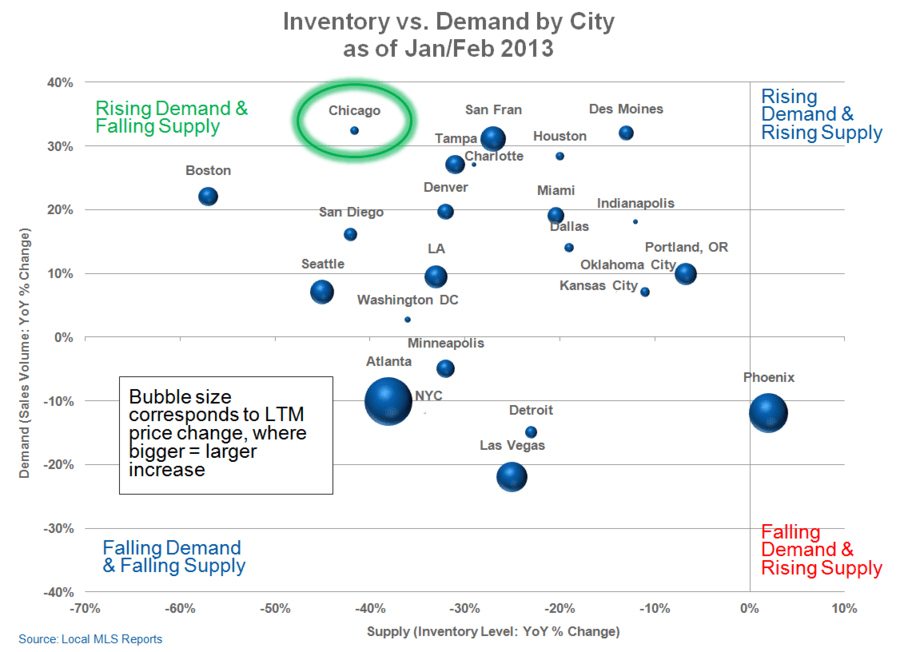

Take a look at the chart below. We're showing inventory (x-axis) and volume (y-axis) changes on a year-on-year basis by market as of either January or February, depending on the market. The Financials Sector team’s work has shown that prices lag both demand (sales volume) and supply (inventory) in housing by 11 to 18 months.

Currently, Chicago is one of, if not the strongest looking market on a prospective basis. The change in inventory over the past year is -41.6%, while the change in demand is +32.3%. Putting those two factors together creates a very powerful tailwind for the coming year. Given how much exposure TCB has to this market, we think they will be a primary beneficiary of Chicago's coming property recovery.