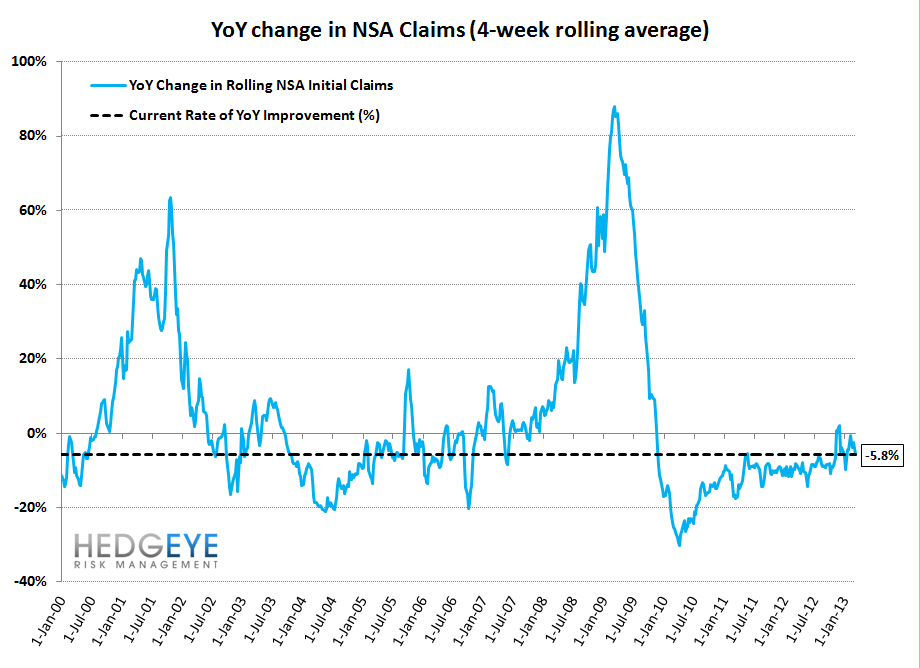

Labor Market Strength Accelerates

This past week's NSA (non-seasonally adjusted) initial jobless claims were lower YoY by -7.3%, which is roughly consistent with the rate of improvement over the previous two weeks (-8.9% and -8.0%). This brought the 4-week rolling average YoY change in NSA claims to -5.8% as compared with -4.2% in the previous week. What this signals is that the real labor market is experiencing accelerating improvement, and this has been the case for the last five weeks.

On the SA (seasonally-adjusted) front, the numbers also looked good. This is what the market is paying attention to. As a reminder, the SA data is now facing a small, but growing headwind over the coming six months. The first chart in the note tells the story well.

The Data

Prior to revision, initial jobless claims fell 8k to 332k from 340k WoW, as the prior week's number was revised up by 2k to 342k.

The headline (unrevised) number shows claims were lower by 10k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -2.5k WoW to 346.75k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -5.8% lower YoY, which is a sequential improvement versus the previous week's YoY change of -4.2%

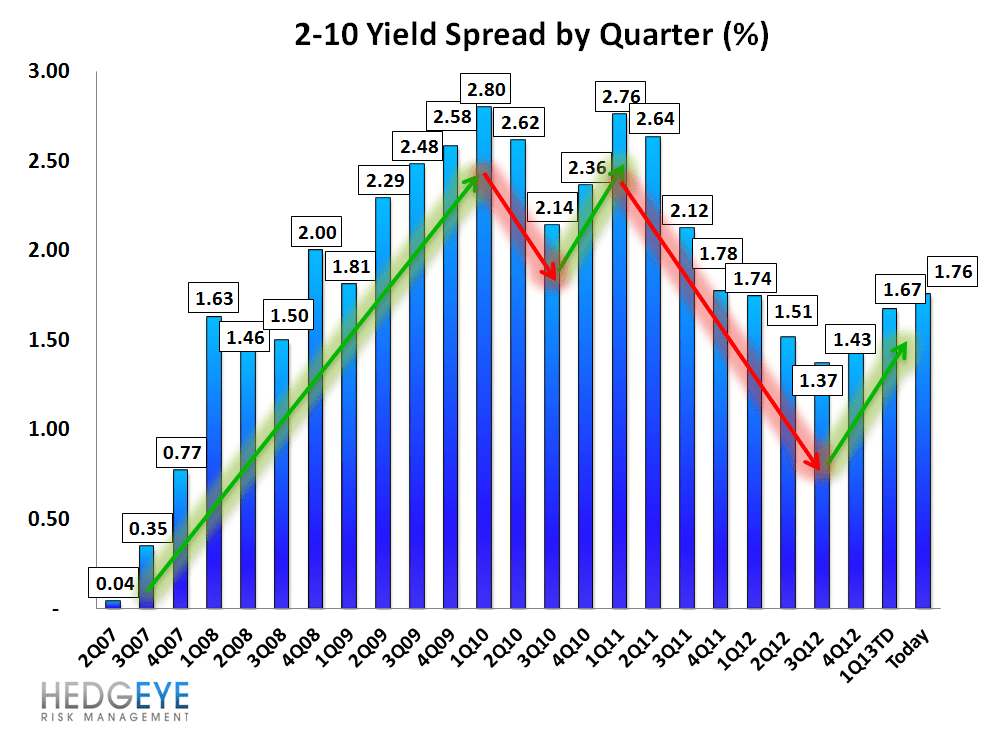

Yield Spreads

The 2-10 spread rose 7.0 basis points WoW to 176 bps. 1Q13TD, the 2-10 spread is averaging 167 bps, which is higher by 25 bps relative to 4Q12.

Joshua Steiner, CFA