This note was originally published at 8am on February 25, 2013 for Hedgeye subscribers.

“We live by emotion, prejudice, and pride.”

-Dwight D. Eisenhower

That’s what President Eisenhower wrote in a letter to Winston Churchill in the early 1950s after the Korean War. He added: “It is remarkable how little concern men seem to have for logic, statistics, and even, indeed, survival.” (Ike’s Bluff, pg 105)

Sounds a lot like risk managing the 2013 Global Macro market to me. So far, with the underpinnings of real (inflation adjusted) global economic growth stabilizing (instead of slowing), the best way to survive the game has been to be long growth, not gold.

We all have our investment-style prejudices. We all have plenty of emotion too. The hardest thing to do is keep that all checked at the door before we turn on our screens every morning. The Behavioral side of this game has never been so important.

Back to the Global Macro Grind…

Admittedly, I was all fired-up covering shorts and getting longer (equities) during last week’s 2-day correction. Was I being emotional? Or were the sellers? Now I’m questioning whether I got Bullish Enough?

At Augusta in 1954 the legendary Sam Sneed told Ike, “you’ve got to stick your butt out more, Mr. President” (Ike’s Bluff, pg 115). While Eisenhower didn’t like having other people tell him what to do, he listened. Sneed’s advice wasn’t from some local pro.

When I stick my old hockey bubble-butt out and make a market call, I don’t ask a local pundit for permission. It’s always based on two very important things that we are trying to hammer home with clients – they are both critical to our process:

1. The Risk Management Signal

2. The Team’s Research Views

Note which one of the two comes first. Indeed, it is the signal I prioritize over what can often become research noise. All that said, when both are aligned, I’m learning to get over how I look - and I just do it (stick out my butt).

When you boil down the difference between our bullish Research View on growth versus competitor views, it’s quite simple:

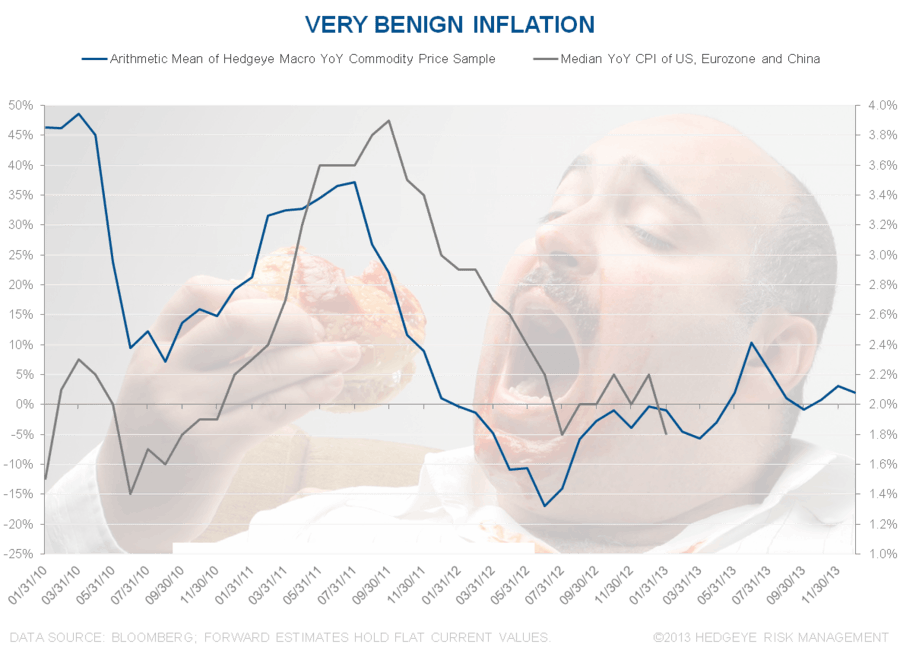

- Our view is Dollar centric: Strong Dollar = Down Commodities (deflation) = Stronger Consumption

- Their view is Commodity centric: they are either calling for inflation OR thinking deflation is a bearish leading indicator

Irrespective of your research team’s view, this is what Mr. Market’s signals think:

- Strong Dollar = up another +1.1% last week; up for 3 consecutive weeks on a +3% run

- Commodity Deflation = down another -1.7% last week; down for 3 consecutive weeks (-3.9% all in)

No, the world’s economies and stock markets didn’t end on that. In fact, despite Oil prices reacting late relative to Gold (Brent Oil finally down -2.9% last wk), the two key US consumption demand points we care on (US employment growth and housing) held up quite well. The question now is how well do they react to prices at the pump falling, instead of rising?

If you Embrace Uncertainty at the core of your process, the simple answer is usually going to be ‘I don’t know.’ You’ll know when market prices and high-frequency economic data either refute or support your thesis. Advice: don’t marry your thesis.

If you were buying commodities futures and options contracts since the Bernanke Top (September 2012), the CRB Commodities Index is one of the worst places you could have been invested (down -9% from there to here). And finally, in the last few weeks of Commodity Deflation, the net long (CFTC futures/options position) has capitulated to its lowest level since DEC 2011:

- Copper contracts crashed last week, down -51%! to +11,413 (lowest since NOV 2012)

- Gold contracts crashed (again) last week, down another -40% to 42,318 (lowest since JUL 2007)

- Farm Goods contracts capitulated too, down -44% last week to 190,892 (lowest since March 2009)

Farm Goods still has the biggest net long position because food prices were the last of the commodities to put in their all-time tops. Corn’s all-time high was in August of 2012. Corn prices are now on the verge of crashing (greater than 20% peak-to-trough decline) from that all-time top and net long contracts in corn were down -48% last week to +65,303.

Are falling food prices good for you? Do you eat? If you don’t (or someone in Washington buys all your meals with our tax “revenues”), you can safely assume, with no emotion or prejudice, that the rest of the world does.

Hedgeye reiterates our 0% asset allocations to both Commodities and Fixed Income this morning. Sure, we will take down these equity asset allocations when the signals tell us too. But we didn’t get those signals at Thursday’s lows. Emotional sellers did.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, USD/YEN, UST 10yr Yield, and the SP500 are now $1548-1611, $112.61-115.15 (Oil is bearish TRADE now), $3.51-3.65 (Copper is back in a Bearish Formation), $80.57-81.71 (USD = Bullish Formation), 92.72-94.41 (we re-shorted Yen last wk), 1.96-2.05% (Bond Yields = Bullish Formation), and 1502-1530, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer