I've been a long-term bear on Carter's due to the company's focus on maintaining EBIT margins in light of top line and gross margin pressure vis/vis cutting into bone on the SG&A line - instead of doing the opposite (i.e. take it on the chin with margin and get the right infrastructure in place to drive the business forward). I started to turn more positive when Fred Rowan was ousted, and with the comp stabilization in the recent quarter under CEO Mike Casey (new CEO - former CFO - who I like). But any confidence that the company in finally on track with proactively managing its brands for the 'New Reality' of retail was just stopped dead in its tracks.

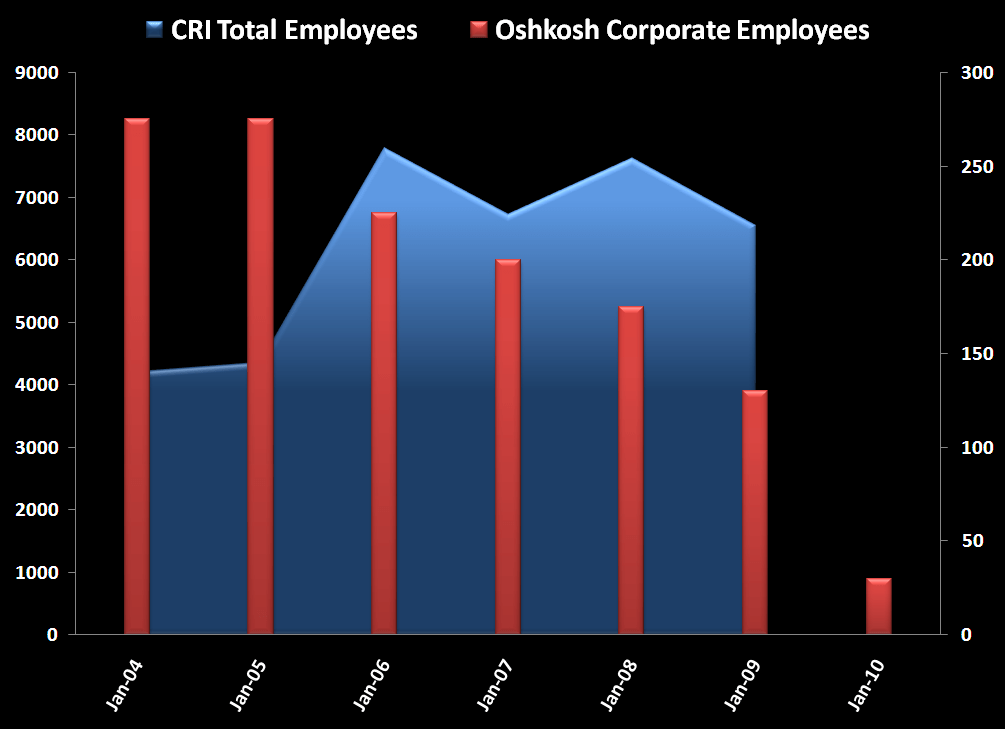

CRI just announced with headcount reductions at Osh Kosh - again. Let's put this into perspective. At the time CRI bought Osh Kosh in 2005 it had 275 employees. By 2007 that was cut in half to 135 as a way to buoy margins in light of top line challenges and the absence of sourcing savings that padded for the prior 5 years. Now it is laying off another 90 employees, and is consolidating another 10 into Carter's HQ. So basically, we're looking at 30 people (20 of which will be in consumer affairs, IT and finance) solely dedicated to growing a $300mm brand.

The momentum on the P&L looks quite good here, and the SG&A saves will likely help that near-term. I definitely would not be caught short this name here. But as the retail rally continues (which I think it will), there will be obvious candidates who have boosted earnings by cutting costs in and unhealthy and irresponsible way. CRI is one of them.

Get this name on your 'whack a mole' bench.