This note was originally published at 8am on February 21, 2013 for Hedgeye subscribers.

“The Great Recession was not an unpredictable ‘Black Swan’ event, but an almost blindingly obvious certainty.”

-Steve Keen

Yesterday was emblematic of the news flow that dominates today’s financial markets. Speaker of the House, John Boehner, published a scathing op-ed in the Wall Street Journal that criticized President Obama over the looming sequester, calling it “a product of the president’s own failed leadership.”

Hours later, the Federal Reserve released the minutes from its January 29 – 30 Federal Open Market Committee (FOMC) meeting. As soon as the robots read that “Many FOMC participants voiced concern about risks of more QE,” gold gapped down, the USD jumped, and stocks slid into the close.

These are the days of our centrally-planned lives.

Given the undeniable impact that both monetary and fiscal policies have on the disposable income in your pocket, the interest earned on your life’s savings, and the asset prices in your portfolios, it’s fair to ask some tough questions of those making the decisions:

- What caused the financial crisis and subsequent “Great Recession” which we are still mired in (as a reminder, US real GDP was -0.1% in 4Q12)?

- Why didn’t you see the crisis coming?

- What are you doing to lift us out of the current recessionary-like environment, and why do you believe these policies will work?

At 2PM EST today, the Hedgeye Macro Team will host a conference call for institutional clients with economist Steve Keen to get his views on those questions and more. Email team@hedgeye.com if you would like to participate in the call.

Professor Keen predicted the financial crisis as long ago as 2005, and was recognized by his peers for his work when he received the Revere Award from the Real-World Economics Review for “being the economist who most cogently warned of the crisis, and whose work is most likely to prevent future crises” (Keen 2011). He collected twice as many votes as the runner-up, Nouriel Roubini. His book Debunking Economics and other works are super-critical of mainstream economics (“neoclassical” economics – think Bernanke and Krugman), and succinctly describe his own theories on monetary macroeconomics, which are built on the foundations of money, banks, debt, instability, and complexity.

Professor Keen quips, “Bernanke’s Essays on the Great Depression is near the top of my stack of books that indicate how poorly neoclassical economists understand capitalism,” and that “Krugman himself is unlikely to stop walking on two hind legs – he enjoys standing out in the crowd of neoclassical quadrupeds” (Keen 2011). Professor Keen likes to take shots at Bernanke and Krugman… Sounds like a Hedgeye kind of guy!

One topic that Professor Keen is an expert on that is generally absent from macroeconomic discussion is the relationship between private sector debt and growth. Debt of any kind – government, financial, mortgage, credit card – is often ignored in mainstream economics due to the argument that “one man’s liability is another man’s asset,” so that the total level of debt has no economic impact (which Keen refutes). It was really only after Carmen Reinhart and Kenneth Rogoff published their New York Times Bestseller This Time is Different, and sovereign bond yields in Europe’s periphery started to spike, that economists and market participants began speaking to the aggregate level of debt more seriously, but it was often only government debt.

The now widely-held opinion is that excessive sovereign debt will eventually impede growth. But Professor Keen has empirically demonstrated that this claim is too simplistic, and fails to explain why public debt increases in the first place.

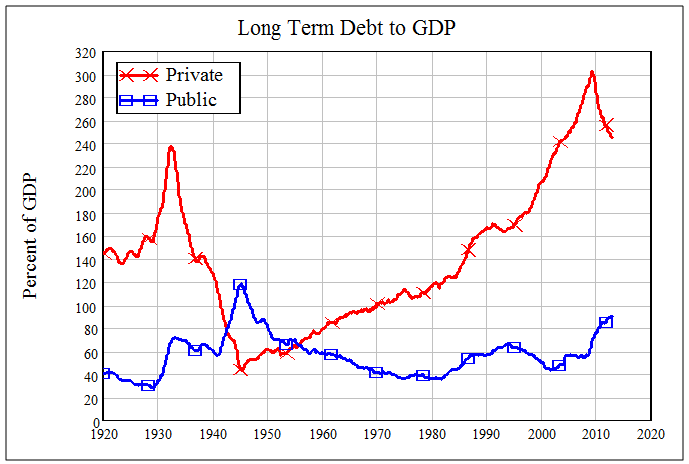

Consider that in 2007 US public debt was less than 60% of GDP, while private sector debt was 300% of GDP, up from 110% in 1980. A massive private sector debt bubble grew for nearly 30 years while public sector debt remained fairly constant (see our Chart of the Day below). It was only after the private debt bubble burst in 2008 that public sector debt began to lever up. Why?

The correlation (2000 – present) between private debt and unemployment is -0.94. The correlation between government debt and unemployment is +0.82.

In a recession tax payers lose jobs and go on some type of welfare – for a government that equates to tax receipts down and outlays up. To fund the delta, the government borrows. In 2007, US government revenues were 18.5% of GDP; that fell to 15.1% of GDP by 2009 and only recovered to 15.8% of GDP in 2012. On the other side of the ledger, outlays were 19.7% of GDP in 2007 and jumped to 25.2% of GDP in 2009 – the majority of that increase was “mandatory” outlays. In fact, only 36% of US government spending is deemed “discretionary,” and 17% is discretionary “non-defense.”

The point is that public sector debt is reactionary. While it’s popular to deride politicians about mounting debts and deficits (and indeed politicians do this to each other), they have less control than most know. Increasing public sector debt is the symptom, not the disease. The disease is a private sector debt bubble that bursts, and is slowly deflating from a still very high level (~240% of GDP today).

The blame lies with the economists that allowed, and in fact assisted, the private sector debt bubble to grow to a dangerous, unsustainable level (because debt doesn’t matter in their models) – the same economists that are today charged with cleaning up the mess.

In describing “The Great Moderation,” Bernanke said in 2004, “Improved monetary policy has likely made an important contribution not only to the reduced volatility of inflation but to the reduced volatility of output as well.”

Does Bernanke and co. still believe their monetary policies to be a panacea? Probably. But how can they solve for the crisis if they continue to ignore its cause – a heavily-indebted, deleveraging private sector?

Professor Keen believes that we could be in for many years of a drawn out deflationary crisis, as private debt is still ignored in public policy. We hope he’s wrong about that, but are looking forward to learning more from Professor Keen on our call with him today.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, and the SP500 are now $1558-1617 (bearish/oversold), $112.94-115.89, $80.29-80.99, 92.64-94.36, 1.97-2.05% and 1507-1530, respectively.

Kevin Kaiser

Senior Analyst