This note was originally published March 05, 2013 at 22:08 in Retail

Conclusion: Pick your duration. It matters -- as much today as it did when evaluating it as a short at $40. If you need to make money in a name before June, don’t look to JCP. The first quarter will be weak, 25% of square footage is unshoppable during the quarter due to construction, and EPS expectations might not be low enough. But if you can you can look to a TREND (2H) or TAIL (3 Yr) duration, we think the risk/reward favors the upside. Here’s an overview of the incremental changes in our thought process on JCP over the past week.

Full Details

We were short JCP since Ackman first brought in Johnson starting in June 2011. The crux of that call was that there was a duration mismatch between the time period Johnson was incentivized to fix JCP compared to how quickly Wall Street was being led to believe (by management and Ackman alike) that a turn would take place.

That call worked quite well, but we turned positive earlier this year at $19, however, as we thought that the risk/reward was to the upside and that all the bad news was priced into the stock. That was clearly a wrong assumption. We go through the puts and takes below, but with the downward spiral since the quarter we’re left with the question as to whether we should fish or cut bait.

We’re not going to sell into the emotion-fueled debate we see out there today. Instead, we think that the real answer to the buy/sell question is different based on each of our three durations, TRADE (3 weeks or less), TREND (3 months or more), and TAIL (3-years or less).

1. TRADE: While we won’t bow to the negativity that’s currently swirling around this ticker, the fact of the matter is that there’s nothing we can point to before June that will make this stock go up. There’s a) the Martha Stewart/Macy’s trial (which could go either way), b) nearly 25% of JCP’s square footage that will be under construction (and therefore unshoppable), and c) the start of JCP’s cash burn into spring while catching up on vendor payables. Package all of this with zero guidance from management on the quarter, and the Street looking for a relatively rosy -7.8% comp in the quarter (a 500bp acceleration on a 2-year basis), and the setup into the May 1Q earnings report is nothing to write home about.

2. TREND: Once we’re past 3-months, we think that that the ‘rate of change call’ as it relates to JCP’s top line will start to unfold. Maybe that did not matter as much when the stock traded through $23 in advance of the quarter, but we think it matters at $15. Even if JCP needs to buy the comp, we think that sales trajectory will be the sole factor over a TREND duration that people will care about in answering the question as to whether it actually has connectivity to its consumer or not. As goes customer connectivity, so goes the stock.

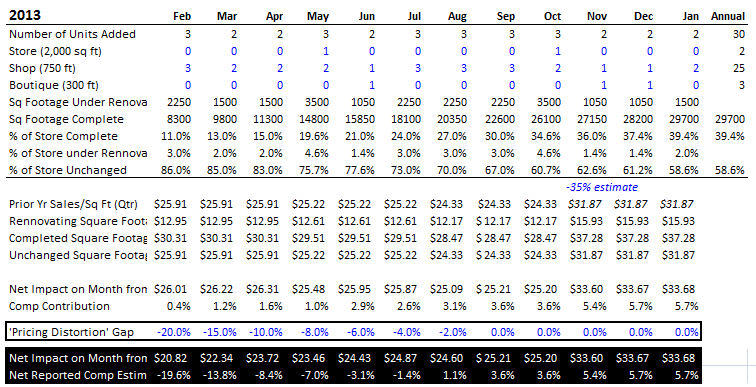

For the year, our key modeling assumptions vs consensus are outlined in the table below. Assuming that JCP still runs at a whopping ($2.12) loss per share, we have the company using up $1.1bn of its revolver in order to maintain a cash balance of about $450mm. This assumes a very conservative -$500mm hit to working capital after cutting into too much bone last year, and also assumes no cuts to the company’s $1bn capex plan.

3. TAIL: While our TAIL duration is 3-years or less, we’re going to cheat a little bit and take this model out a full 5-years. We think we can get to earnings power starting with a $3 over that time period assuming that JCP only flirts with its former glory when it was simply a ‘bad’ instead of a ‘horrific’ retailer. Let’s be clear about one thing…we’re not parroting the Ackman earnings power of $14-$22 per share (yes, he actually said that). But our point is that we don’t need that kind of earnings power for the stock to work over a TAIL duration.

Our Updated Thoughts On Key Issues Impacting The Stock

Here’s an overview of what has changed since the print, where we think were wrong, where we’ve been challenged by investors, as well as our response.

- Expectation Mismatch: in reflecting further in the quarter, you don't have to be a genius to see that we got the near term research call wrong. Ironically, for the quarter, we modeled a -35% comp, 24.5% gross margin, and a loss of -$2.50 per share, which is pretty darn close to where JCP came in. Trade receivables were worse than we expected, but net cash on hand was still greater than the $550-$650mm we said we needed to see to prevent liquidity concerns. Our mistake was assuming that these below-consensus estimates were ‘in the stock’. Lesson learned = a large scale negative headline is rarely ‘in the stock’.

- VNO Stock Sale: The second largest shareholder selling a 10mm share block on the day Ron Johnson was on trial being grilled by Macy’s lawyers about the dispute surrounding Martha Stewart product was tough to see coming. That said the stock traded down over 5% in the session leading up to the announcement – so someone not only saw it, but unethically profited from it.

- Timing of Shop Rollouts: If the Martha Stewart trial goes against JCP, we have a very hard time believing the news headlines saying that ‘shelves will be empty’. Rather, we think it’s more likely than not that the product branding or design will need to change in a way to make it clearly not conflict with Macy’s. We don’t think that it will delay the shop opening by more than a month or so, but we think that it could delay the Martha Stewart productivity ramp by 1-2 quarters.

- Consumer Sentiment: This whole debacle has gotten so much negative press. Check out $JCP on twitter. No exaggeration that 99% of mentions are negative. The company, the management and the brand seemingly has no support – at least by this audience (we trust twitter more than Wall Street sentiment factors in this regard). Usually such negative sentiment supports a bull case, but the bear case would be that such negativity actually manifests itself in the form of backlash against shopping at the store. In other words, after firing the existing customer and being consistently in the hot seat in front of the American Consumer at large, could it actually prevent the new shop rollout plans from working? It’s a question that we need to be asking ourselves.

- How Many Shops Should There Be? We debated this one with several clients, and we think that it’s a very valid question. JCP is reconfiguring 700 of its 1,100 stores. But the question is how JCP arrived at that 700 number. Why not 500? 300? It can do all the studies it wants, but the reality is that it won’t know the appropriate number of stores for this new format until it goes too far. The solace we have from a modeling perspective is that we’ll assume that management has the common sense to start at the very top as it relates to attractiveness and potential likelihood for success. It’s going after 500 over the immediate-term, so it clearly has room to stall or alter capex plans if the data suggests that their 700 estimate is too high.

- RJ’s Job Security: Better than 50% of investors we talk to think that Ron Johnson won’t be working at JC Penney in 2014. We disagree. Simply put, JCP was a horrible retailer before he joined. Then the Board gave him a mandate to change the model. They expected disruption in sales. Did they expect first year sales to be down 25%? Probably not. Did Johnson make some serious errors? Absolutely. But the Board is getting what it asked for – a radical transformation in the business model.

What are they going to do…fire Johnson and bring in another person to return the company to its former glory? No way. In fact, we think that vendors still hold Johnson in high regard and buy into his vision as to what JCP should become. If he personally ceased to exist in his role as CEO, there’s serious risk to vendors pulling out of JCP en masse to protect their own brands.

- Real Estate Value Support: When Ackman did initial storytelling about JCP, he talked up a replacement value of $11bn, or about $50 per share. That’s fine, but there’s a pretty big flaw in that analysis – we’d argue that if JC Penney stores are so grossly underperforming, there’s no need for them to be replaced. Hence we could argue a theoretical replacement value of zero. We can, however, argue something closer to $8-$10 per share. Our assumptions are as follows.

A ) Cap Rates: While cap rates have been drifting lower, JCP would still command among the highest cap rates due to its sub-prime real estate locations. Let’s assume 8.5% vs Power Center/Strip/Regional Mall average of 7.0%.

B) Rent: Current JCP rental rate is about $4 per square foot on its leased property. It’d be tough to argue something higher than that today. Let’s assume something between $3.50 and $4.00.

C) Combining the two, we’re getting to a value of $8-$10.

The key here is not that the portfolio will be liquidated overnight. But rather that it has about $1.8bn-$2bn of near-term liquidity it can access if need be.