Red start to the year likely

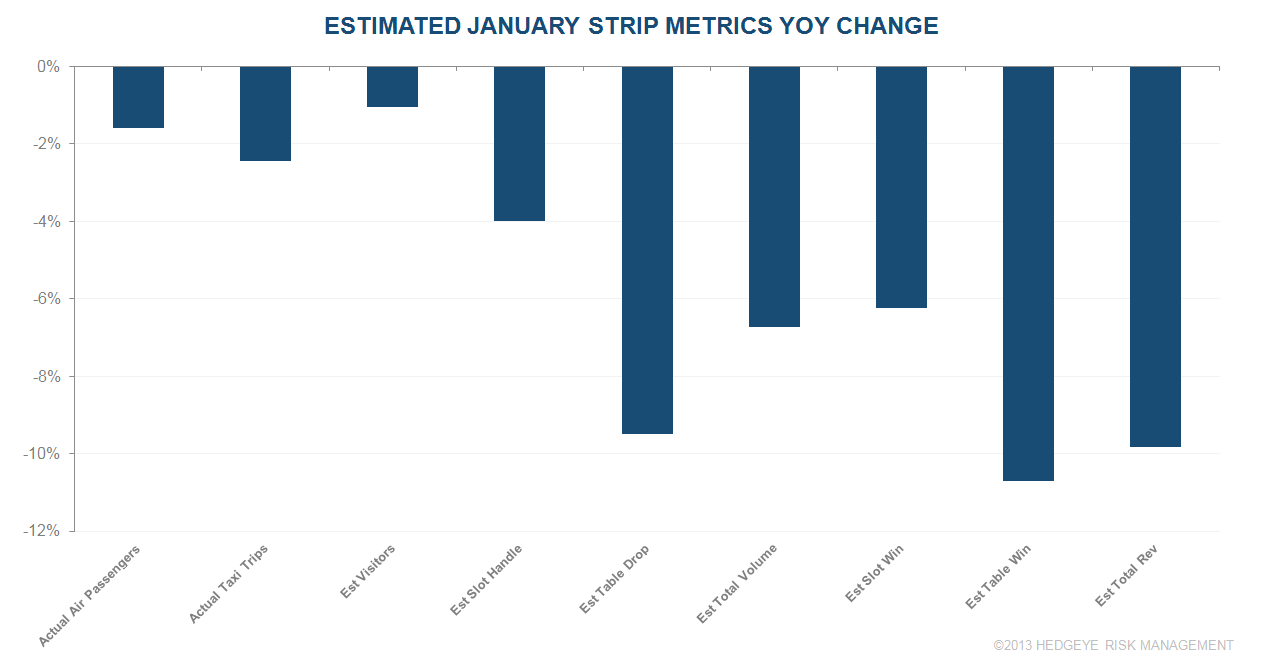

According to our proprietary model, assuming normal slot and table hold, January Strip gaming revenues may have fallen between -8% to -12%. We believe gaming spend per visitor will tumble 8-10% YoY. Due in part to the Chinese New Year (CNY) shift, Baccarat gaming volumes were up 163% last January to $1.56 billion. CNY fell into February this year so the comp is very tough. It's not all Baccarat though. We do think table volume ex bacc and slot volumes will be slightly lower YoY this January.

The traffic numbers continue to be weak. McCarran Airport visitation fall 1.6% YoY and Taxi trips dropped 2.4%, the 5th and 7th consecutive monthly decline in the respective metrics. We should get numbers from Nevada in 2 weeks.

Here are our projections: