TODAY’S S&P 500 SET-UP – March 5, 2013

As we look at today's setup for the S&P 500, the range is 23 points or 1.06% downside to 1509 and 0.45% upside to 1532.

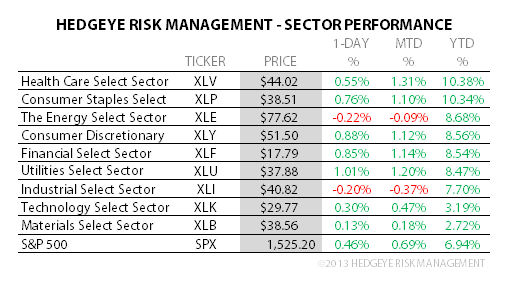

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.66 from 1.64

- VIX closed at 14.01 1 day percent change of -8.79%

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: ISM Non-Manf. Composite, Feb., est. 55.0 (prior 55.2)

- 10am: IBD/TIPP Eco. Optimism, March, est. 48.1 (prior 47.3)

- 11am: Fed to purchase $2.75b-$3.5b notes in 2020-2023 sector

- 11:30am: U.S. to sell 4W bills, $25b 52W bills

- 2pm: Fed’s Lacker speaks on monetary policy in Washington

- 4:30pm: API Energy Inventories

GOVERNMENT:

- Senate Budget Cmte holds hearing on tax code, 10:30am

- Senate HELP Chairman Tom Harkin, D-Iowa, House Education & Workforce ranking member Rep. George Miller, D-Calif., announce introduction of legislation to raise federal minimum wage to $10.10/hr from $7.25, then provide automatic annual increases linked to changes in cost of living, 12pm

- Agriculture Sec. Tom Vilsack among witnesses testifying on state of rural econ. at House Agriculture Cmte. hearing, 10am

- Nuclear Regulatory Commission staff meets officials from Duke Energy to discuss whether company violated license for fire protection at a South Carolina nuclear plant, 1pm

- Rep. Maxine Waters, D-Calif., FDIC Chairman Martin Gruenberg, SEC Commissioner Luis Aguilar speak at Greenlining Institute conference on diversity in financial industry, 8:30am

- Treasury Dept, OCC hold a meeting to discuss the minority depository institution industry, 8:30am

- House Fin Svcs panel holds hearing on Bernanke’s recent testimony on monetary policy, 10am

- North American Securities Administrators Assoc. releases 2013 legislative agenda, including measures to regulate crowdfunding and fiduciary duty rule for broker-dealers, 10am

- House Ways and Means panel holds hearing on tax provisions in Affordable Care Act, 11am

- U.S. Homeland Security Secretary Janet Napolitano discusses airport, airspace security at International Air Transport Assn conference in Brooklyn, N.Y., 9:30am

WHAT TO WATCH

- EU opens way for easier budgets after Italian austerity backlash

- Martha Stewart to testify today in J.C. Penney/Macy’s suit

- House budget bill would continue automatic spending cuts

- Compuware said to attract private-equity firms’ buyout interest

- Pearson CEO said to tell FT staff to brace for fewer jobs

- Commonwealth stock sales may be completed, U.S. judge rules

- Fannie Mae regulator sets securities platform for post-GSE world

- J&J, Bayer fail to win U.S. backing for expanded Xarelto use

- Heinz CEO Johnson would get $200m in post-Berkshire exit

- Rexnord said to draw Watts as suitor for water-management unit

- News Corp. said to start cable-sports challenge to ESPN

- Anadarko, Dhoot start sale of Mozambique gas stake: Reuters

- Artisan Partners Asset Mgmt IPO books close tonight, terms show

- Senate report faults JPMorgan’s “whale” disclosures: NYT

- Tribune said to aim to sell all newspapers in single deal

- Chavez health worsens with second lung infection, Venezuela says

EARNINGS:

- Bank of Nova Scotia (BNS CN) 7:30am, C$1.25

- Infinity Pharmaceuticals (INFI) 4pm, $(0.84)

- VeriFone Systems (PAY) 4:01pm, $0.49

- Smith & Wesson (SWHC) 4:05pm, $0.23

- First Quantum Minerals Ltd (FM CN) 5pm, $0.33

- Qihoo 360 Technology Co Ltd (QIHU) 5pm, $0.17

- Trilogy Energy (TET CN) 5pm, C$0.03

- Allied Properties Real Estate (AP-U CN) Aft-mkt, C$0.46

- Gibson Energy (GEI CN) Aft-mkt, C$0.34

- Uranium One (UUU CN) Aft-mkt, $0.02

- Taro Pharmaceutical Industries Ltd (TARO) Aft-mkt, NA

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Hoarders Turn Sellers as Bull Run Decays: Chart of the Day

- Rice Glut Expands With Farms Poised for Record Crop: Commodities

- Gold Rises for First Time in Five Days on Stimulus; Silver Gains

- Copper to Climb on Chinese Demand This Year, Jiangxi Copper Says

- Soybeans Reach One-Week High on Signs of Stronger Export Demand

- Sugar Rises for Second Day on Ethanol Outlook; Coffee Also Gains

- WTI Crude Rebounds From 10-Week Low; Brent Pipeline Remains Shut

- Cooparaiso Sees Brazil Reaping Record Off-Year Coffee Harvest

- Palm Oil to Trade at 1,950-2,500 Ringgit a Ton, Sauthoff Says

- CME’s Asian Business Expanding 35% Stoked by Gold to Currencies

- U.K. Natural Gas Stores May Empty in Two Weeks: Chart of the Day

- Oil Inventories Gain a Seventh Week in Survey: Energy Markets

- Scorpio Wins as U.S. Crude Curbs Spur Shale Refineries: Freight

- Copper Advances Most in a Week as China Maintains Growth Goal

CURRENCIES

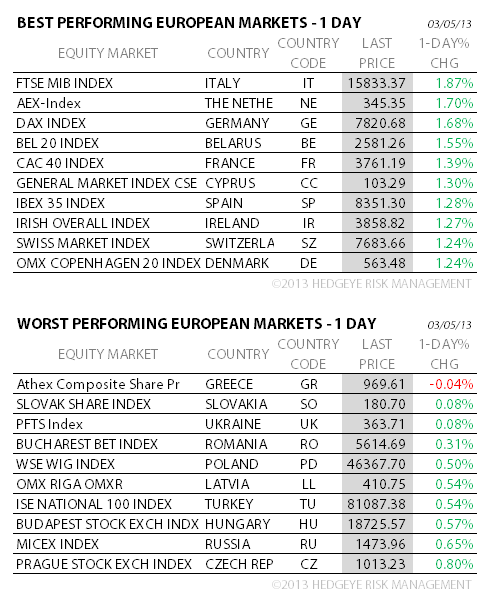

EUROPEAN MARKETS

ASIAN MARKETS

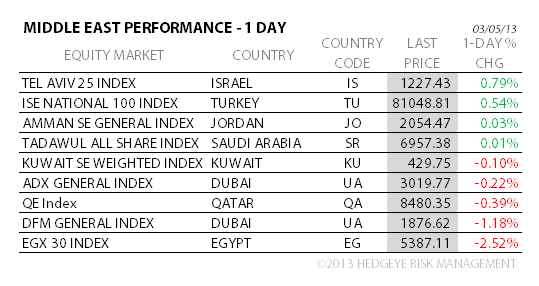

MIDDLE EAST

The Hedgeye Macro Team