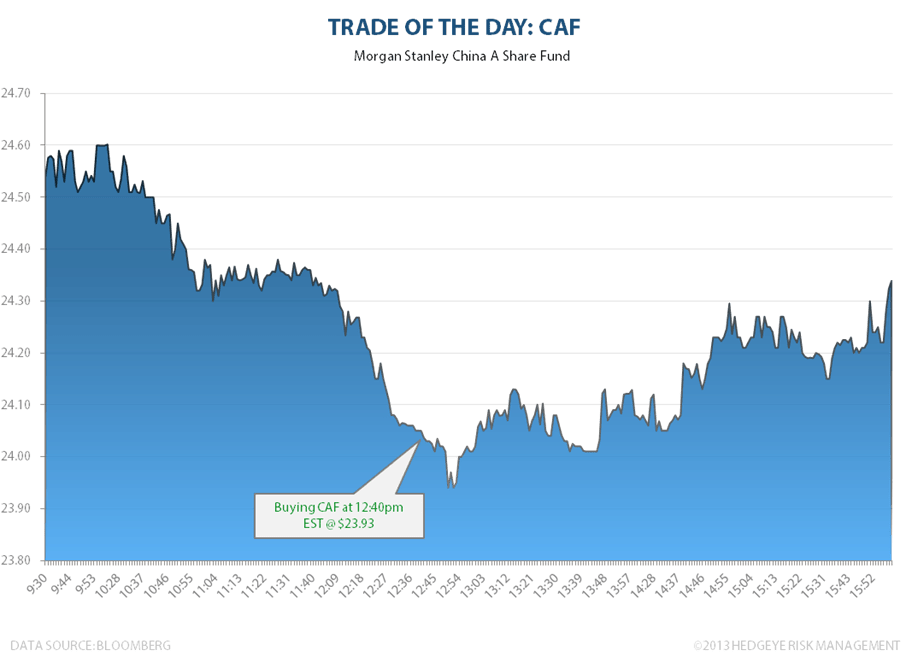

Today we bought the Morgan Stanley China A Share Fund (CAF) at $23.93 at 12:40 PM EDT in our Real-Time Alerts. Buying China back on an immediate-term TRADE Oversold signal in the CAF. See Darius Dale's intraday note on China for details in risk managing the catalysts for this position.