Rate cuts in India have not yet created real liquidity ...

The reserve bank reduced benchmark rates by 25 basis points today, the 6th cut in 6 months. Although the timing of the cut was a surprise to most economists, collapsing wholesale inflation and declining production levels had clearly left the potential more cuts by the central bank baked in.

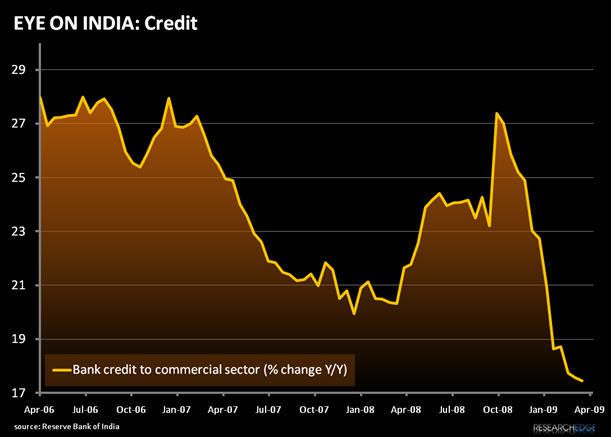

At this point, the big question is not when there will be more rate cuts, but rather when that liquidity will pass through to the real economy. To date, the spread between average commercial rates and RBI benchmarks have hardly contracted while growth of commercial credit continues to decline on a sequential year-over-year basis.

To date, our opinion on prospects for India's recovery has diverged wildly from Street consensus because of a fundamental difference in how we interpret internal demand there: While our competitors see strength in India's lack of export dependence, we see weakness in a dependence on an agrarian sector which currently keeps over half the population employed on a bare subsistence level. One thing that both they and we can agree on however is the need for credit liquidity to help drive internal demand.

With the election cycle in full swing (a complex, manual process that will take weeks to conclude) political tail risk takes precedence in our model, but we will continue to watch the Indian market closely for signals that government measures are having an impact. Until we see some confirmation of that, we will retain our short bias on the India equity markets.

Andrew Barber

Director