Our bullish stance on Brinker remains firmly in place as the Investor & Analyst Conference was starkly different in tone to the unsettling Darden Analyst Meeting the couple of days prior. Here are our summary thoughts on EAT:

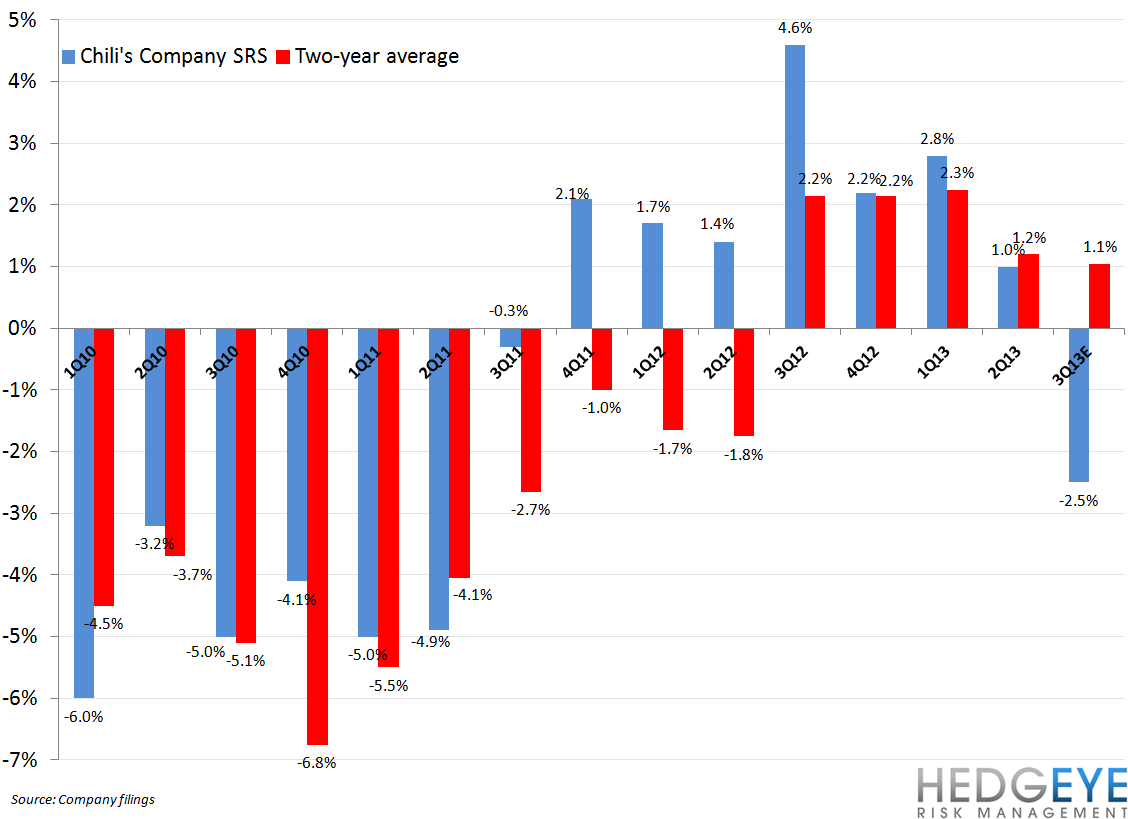

- Consistent with other industry players, Brinker said that Chili’s quarter-to-date same-restaurant sales are down 2-3%. This implies industry sales are down more than -3.5% if the Gap-to-Knapp this quarter has remained constant versus that of 2QFY13.

- EAT guided FY 2013 to the low end of its prior guidance for EPS of $2.30-$2.45 but in line with consensus expectations.

- The strong margin trends are insulating the company’s earnings from the current top line softness

- Brinker indicated that it could meet its long standing $2.75-$2.80 EPS target in FY 2014, a year earlier than the initial goal that was set back in 2010.

- Brinker's disclosed goal to double EPS again to $4 per share by FY 2017, driven by familiarity, variability and the continued benefit of new technology.

- To reach that goal the company will drive 3-4% revenue growth and 10-15% EPS growth.

- EPS will also benefit from the share repurchases are expected to exceed $1 billion over the next five years or 40% of the market cap of the company.

- The company highlighted a diversified business model comprising of Chili’s and Maggiano’s, franchising royalty streams and the 2nd largest casual dining company in the world.

- Management has earned the respect of Wall Street delivering 330bps of a targeted 400bps improvement in Chili's stet back in 2010.

- EAT remains of the best run companies in the restaurant industry and a LONG on the Restaurant Position Monitor.

Conclusion

We believe that Brinker is well poised to deliver on its stated goals and remains one of our favorite names in the restaurant space. The company is offering investors a differentiated focus on returns with a clear capital allocation strategy. EAT is one of our favorite names in the restaurant space, even after this past three years.

Howard Penney

Managing Director

Rory Green

Senior Analyst