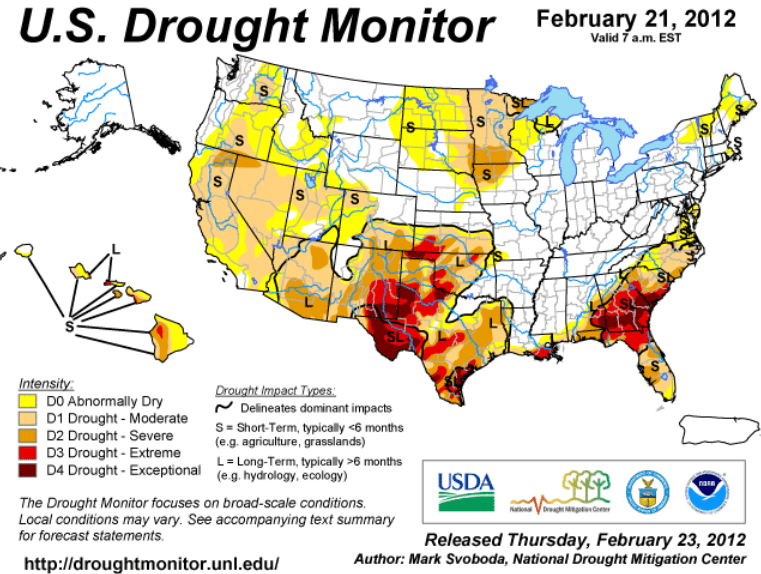

Worse Start to Year versus 2012

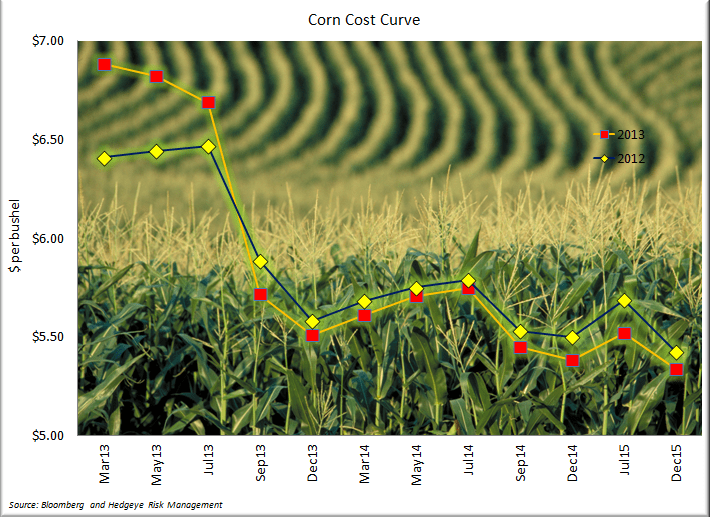

Current moisture conditions in crop regions (in particular west of the Mississippi) are no doubt much worse than a year ago (see progression below). However, conditions have improved since the start of the year and with some projected moisture events coming up, we continue to think the bias is downward in terms of corn prices. The futures curve would seem to agree with us. Further, the set-up on the futures curve appears identical to this year versus 2012.

We think it’s very difficult to be long corn at this point (as supported by recent CFTC data that shows non-commercial buyers becoming less long corn), with significant time (and weather) remaining until the crop goes in the ground. As it currently stands, we would not be surprised to see 97 million acres of corn planted in the U.S this year – the USDA’s current estimate stands at 96.5 million acres. The incentive certainly exists for farmers to plant as much corn as possible.

We aren't in the habit of making bets on Mother Nature, but we do try to estimate what is currently priced in with respect to various assets and it appears to us that ADM at current levels remains a reasonably priced option with respect to the quantity and cost of the upcoming corn crop.

After a very nice run post EPS and with the news that Berkshire Hathaway is an investor, ADM has traded off its highs as the balance of the agricultural complex (fertilizer stocks) have languished in the face of broadly weaker commodity prices. To be clear, ADM is not a play on higher corn prices – lower corn prices benefit ethanol margins and a larger crop benefits merchandise and handling margins – think big crop with no price spikes, and ADM can continue to work from its current level.

Lower corn prices would also be constructive for protein stocks (SFD, TSN, PPC, SAFM) - though at current levels, only SFD interests us on the long side.

Have a good week,

Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC

P:

Matt Hedrick

Senior Analyst