Keith and I spent the last few days talking Macro with some of the big boys in Boston. Not surprisingly, and as usual, the large Boston funds are ahead of the curve and asking many of the right questions. China was a focus, particularly as it relates to her need, or want, for commodities. Specifically, there was a good deal of discussion about copper, or Doctor Copper, as we like to call the industrial metal.

We noted the increased demand for copper from China this year in a note earlier this week, entitled “The Good Doctor Copper”:

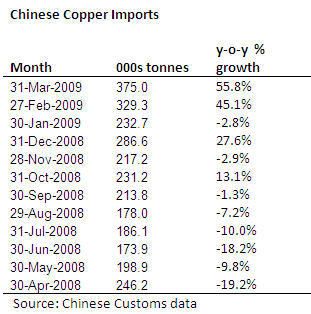

“Coincident with this increase in copper prices are data points supporting improving fundamentals from The Client (China). Preliminary reports out of China suggest that Chinese copper scrap supply may drop 700,000+ tons this year. The implication of this is that copper imports will have to increase, and perhaps dramatically, to offset the decline in copper scrap. March Chinese copper imports jumped to a record high of 374,957 tons, which could be the beginning of a longer term trend of increased imports from The Client.”

In the chart below, I’ve outlined the Chinese import data for the last 12-months. In aggregate the last four months have seen a real spike in imports.

As we were discussing the case for copper on our trip earlier this week, the key debate on the copper bull case was in trying to determine the key source of demand for copper. Was it physical demand, financial demand, or an emerging view of how the Chinese believe, or are advocating, the world financial system be ordered in the future? Daily we get more evidence that Chinese demand for copper, and other commodities, may be driven by motives other than intermediate term needs for the physical commodity. Specifically, Dr Zhou Xiaochuan, who is in charge of monetary policy for China, recently wrote the following in an essay that was posted on the website of the People’s Bank of China:

“Though the super-sovereign reserve currency has long since been proposed, yet no substantive progress has been achieved to date. Back in the 1940s, Keynes had already proposed to introduce an international currency unit named “Bancor”, based on the value of 30 representative commodities. Unfortunately, the proposal was not accepted.” (Emphasis is Research Edge’s.)

The Bancor was a world currency unit proposed by John Meynard Keynes in the negotiations establishing the Bretton Woods Agreements. The idea was that the Bancor was to be fixed to 30 commodities, of which gold was one. Keynes’ believe was that such a currency would stimulate domestic demand and promote global trade balances. Ultimately, Bretton Woods took a different path and used gold, solely, as the basis by which countries pegged and valued their currencies. As we know, Bretton Woods collapsed in 1971, after the United States acted alone to terminate conversion of dollars to gold. The result of this was that the U.S. dollar effectively became the world’s reserve currency for those countries that were signatories to Bretton Woods.

Obviously there was a series of events that led to the Bretton Woods agreement, most notably a global economic depression and World War 2. Additionally, as the only true global superpower, the U.S. was able to take the lead in these negotiations and in managing global monetary affairs. While the US still has the role as a superpower, the world is in a much lower state of duress, so a complete overhaul of the global financial system seems unlikely. Nonetheless, the Chinese are clearly stockpiling copper well beyond their immediate term physical needs and in a world where copper, and other metals, are the basis for the valuation of world currency, financial demand for copper could continue to increased dramatically.

Daryl G. Jones

Managing Director