Both Berkshire Hathaway and 3G prefer to invest in iconic, global brands, and Heinz certainly is that. 3G also has a reputation for aggresive cost cutting, and there appears to be room for that at Heinz as well.

In order to answer the oft-posed (last week, at least) question of "what's next", we took a look at the companies in the packaged food space in terms of how efficiently capital (human and fixed) was utilized. As it turns out, the answer at HNZ was "not particularly well". The companies positioned in the lower left corner of the chart below are at the lower end of the packaged food space on the following two metrics:

- Sales per employee

- Sales/Average Property Plant and Equipment (PPE)

Based on that analysis (admittedly, imperfect), CPB as a short might cause me some sleepness nights given that someone may see an opportunity there beyond what current management has been able to exploit. I think the analysis also supports our belief that HSH and POST could be targets at some point in the future.

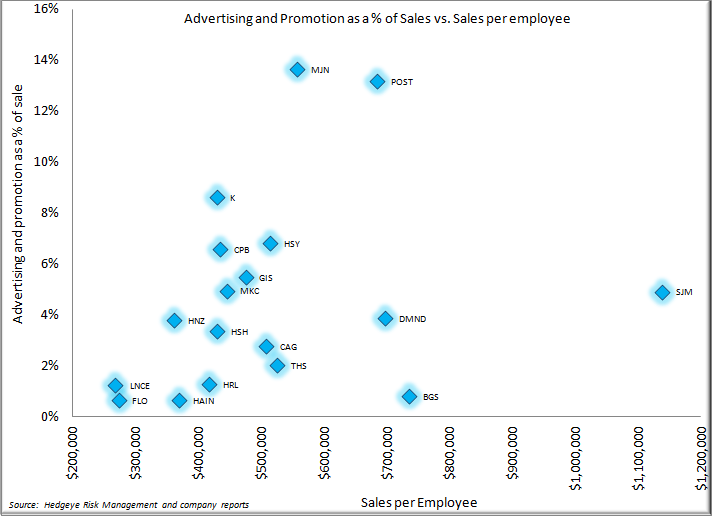

We next wanted to look for brands that might not be as well supported as could be, with an asssociated low sales productivity as measured by sales per employee - again, imperfect, but directionally helpful.

Again, Heinz appears in the "bad" quadrant, and HSH right next to it - though this is weakness recognized by HSH management, with a plan to improve upon the current level of brand investment. In this case, POST brands appear well-supported.

HAIN's position on the chart surprised us at first, then we thought about it and remembered that management there prefers to buy someone else's hard work and grow through acquisitions rather than do the heavy lifting required to build brands.

Where does that leave us?

Well, looking at the data here, we can see the opportunity that Berkshire Hathaway and 3G may be poised to exploit. Further, we continue to believe that HSH and POST could be targets at some point in the future. Finally, given it's proximity to HNZ on the metrics we discussed, a short position in CPB makes us somewhat uneasy.

Enjoy the holiday tomorrow,

Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC

Matt Hedrick

Senior Analyst