Buffalo Wild Wings is talking a big FY13 game but we believe they are running the risk of disappointing for a second consecutive year. Raising guidance to 25% earnings growth (from 20%) is a big statement for a company facing some top-line uncertainty. Time will tell whether the company can walk the walk.

Recap

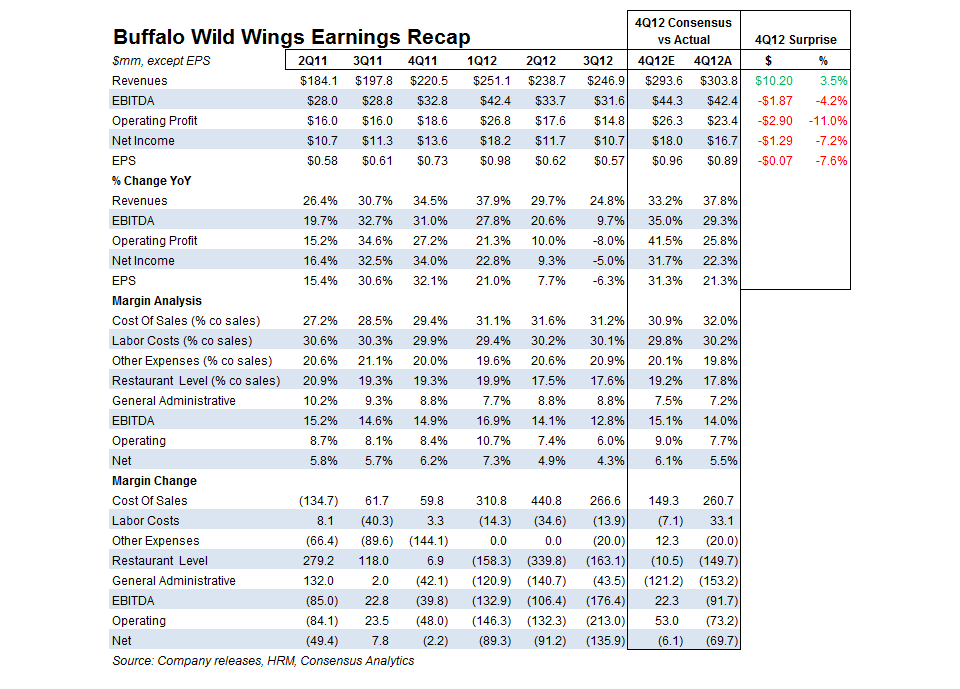

BWLD reported 4Q12 and FY12 earnings after the market close today. 4Q earnings came in at $0.89 versus $0.96 expected. FY12 EPS grew by $0.26 cents year-over-year, $0.19 (73% of the full-year EPS growth) of which came from the extra week in 4Q.

Buffalo Wild Wings’ comparable restaurant sales growth in the fourth quarter was slightly ahead of expectations at 5.8% versus consensus 3.6%. The company revealed that the first six weeks of the quarter were seeing same-restaurant sales growth of -2.8% at company locations. However, management estimates that when this number is adjusted to take into account the timing shift of college and football seasons for both seasons, the co-op comparable sales growth would be +2.6% at company locations.

Outlook

We believe that casual dining trends, broadly, are likely to disappoint in 1Q and see BWLD as an attractive short at these levels. The DFRH news was misinterpreted by the market yesterday, sending the stock on a surge; we believe that the shares should go lower from here. Management raised its implied FY13 earnings guidance to $3.55-3.60. We expect FY13 earnings to come in at $3.42.

Call us at the number below to discuss in greater detail.

Howard Penney

Managing Director

Rory Green

Senior Analyst