"On the road we're somebody else's guests - and we play in a way that they're not going to forget we visited them."

- Knute Rockne

With Keith and Daryl on the road across the pond I've been tapped to pen this morning's Early Look. In doing so, I'll bring an alternate angle to the morning missive compared to my hockey colleagues since my foundation was forged on the gridiron.

In 1924, the Four Horsemen as they were coined comprised Notre Dame's spirited backfield under legendary football coach Knute Rockne. During their three year run together ('22-'25) they only lost two games. They weren't the biggest, nor the fastest, but together they were dominant.

At Hedgeye, we have our own spirited foursome who delivered on our Best Consumer Ideas call on Monday. With the most recent addition to the team, Rob Campagnino, launching Consumer Staples coverage in December, the records have yet to be written, but that's precisely the spirit of Hedgeye's new Best Ideas product - we'll be keeping score real-time with #timestamps. Later I'll hit on four (IGT, JCP, KMB and BKW) of the nine Best Consumer Ideas presented.

First, let me highlight two new process improvements we introduced to Institutional Hedgeye clients on the call, our Best Ideas Product and new Consumer Coverage initiative that I will be spearheading personally. In brief, the Best Ideas Product will highlight only the Best Ideas from each sector firm-wide (4-8 per year). Clients will be notified of changes and additions to this list through Black Books and research notes.

Our Consumer Coverage offering provides a customized approach to conveying our top calls across all of Consumer, beyond just the Best Ideas. Drawing on my experience covering the Retail sector over the last 4+ years, I am working alongside each of our Four Horsemen infusing original content, analysis and risk management (quant/factor overlay) to select clients. For more information on either of these new offerings, please contact us at .

Back to our horsemen. Similarities can be drawn between each consumer sector head and Rockne's horsemen - quarterback (Harry Stuhldreher), fullback (Elmer Layden) and two halfbacks (Jim Crowley and Don Miller) by comparing sector beta (not physiques).

We have Rob Campagnino (Consumer Staples) representing the lowest relative beta - our 'three yards and a cloud of dust' fullback, two halfbacks in Howard Penney (Restaurants) and Brian McGough (Retail), and our high-beta quarterback in Todd Jordan (Gaming, Lodging and Leisure). A sorted bunch indeed, but I look forward to taking the field with these guys. Before we hit on some Ideas, let's cover a little ground on where we stand on the consumer and sectors.

Our view on the consumer here is one of concern of slowing demand from lower-to-middle income earners and underperformance of the companies over-indexed to this demographic. Meanwhile, the latest results out of Hermes and Michael Kors suggest the higher-end consumer remains resilient. Among the factors at play here include payroll tax increases of 2%; at the same time we're seeing a surge in gas prices over the last 3-weeks to historic February highs. The reality is that a pinch on consumer wallets near-term from both ends does not improve sentiment nor spur spending.

Another factor on the horizon to consider is the wealth effect of an improving housing market. As highlighted in our Q1 Macro Themes call, our #HousingsHammer theme suggests that house prices will increase due to lower supply, rising demand and stabilizing mortgage purchase application activity. This is positive indeed, but it will take time to manifest after which point it will take more time for people to actually feel better about their financial position. The timing here will more likely be measured not in months, but years.

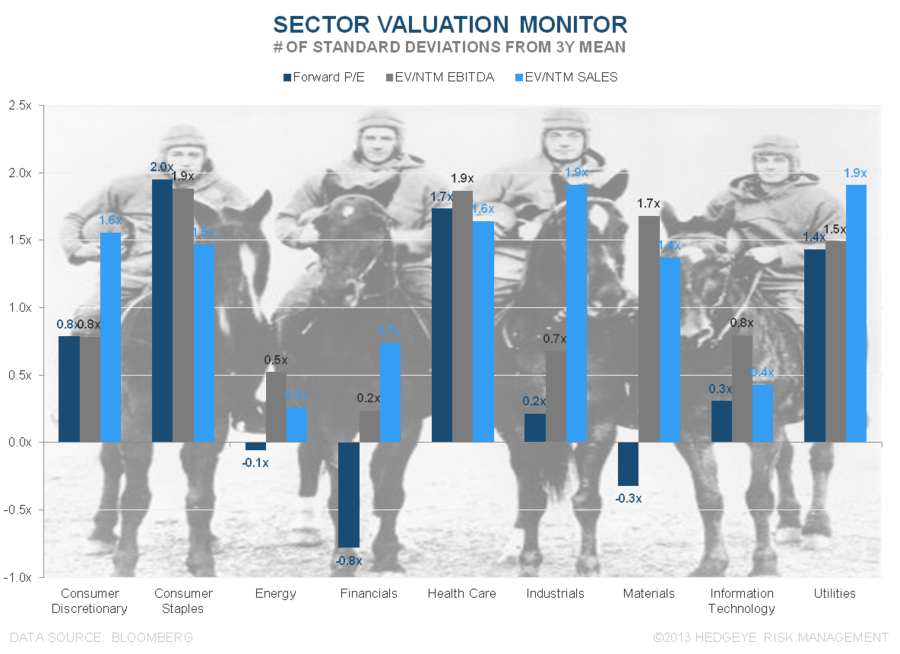

As for sectors, regardless of what duration you pull over the last year, the Staples Sector SDPR ETF (XLP) and Consumer Discretionary (XRT) have consistently outpaced the S&P 500. Year-to-date alone the XLP and XRT are up +7.3% and +8.7% respectively versus the S&P's encouraging +6.5% start.

A look at the chart below reflects this recent performance. Interestingly, yet not surprisingly, the move in price has not been supported in kind by a corollary move in upward earnings revisions with investors seeking yield. This is reflected in a valuation premium in likely sectors (Utilities, Health Care and Staples) 1.4x-2x standard deviations above recent history. The next closest sector? You guessed it, Consumer Discretionary clocking in with a 0.8x STD premium.

While these levels suggest peaky valuations, we're not trying to call a top, but simply recognize that it may be prudent to look beyond fundamentals alone when considering long positions at these levels. As a result, our list of longs consists of largely event/catalyst-driven stories. Fortunately, there are plenty of stocks that fit that criteria for those committed to playing Consumer.

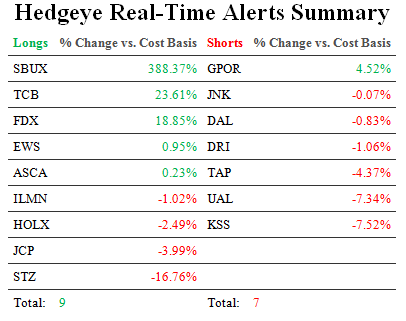

Here are four callouts among the nine Best Ideas discussed Monday, which also included CAG, CAKE, and ASCA (long) and PNK and UA (short):

IGT (Long) - After refocusing on game content and digesting several poor acquisitions to establish online gaming, the stock is at an inflection point with a rebound expected in ROIC. Growing replacement demand and new domestic and international markets should drive multi-year bull slot market. In addition, substantial share repurchase activity expected to continue with accelerating FCF. Bearish sentiment and 11x EPS multiple do not reflect the 20%+ earnings growth we expect. One of the better looking long-term longs as its nowhere near 5yr or all time highs = bullish formation with TREND breakout line of 14.26.

JCP (Long) - Near-term sentiment is too bearish at a time when the delta in top-line is likely to get better. We think improving sales trajectory with comps turning positive in 3Q and improving dot.com will drive the stock higher. Liquidity remains a concern, but we don't see it surfacing over the intermediate-term. TREND breakout above $20.41 is when the long works quantitatively, below that is all storytelling.

KMB (Short) - Top-line growth is masking deteriorating earnings quality at peak valuation. EBIT growth is largely derived from unsustainable restructuring savings and a slowing commodity benefit that swings to a headwind in 2013. Notably, the stock closed at $89.90 flirting with quantitative TRADE support at $89.81 - below that is where you press.

BKW (Short) - Never 'fixed' during its stint as a private company, the outlook for the U.S. and Canada (60% of total) is deteriorating. Some North American franchisees are tracking well below expectations. Decelerating comps are likely to compress BKW's industry high multiple. The stock is breaking down through both TRADE (17.45) and TREND (16.78) lines of support - short it here.

With the calls on the board and #timestamped, the Four Horsemen are off and running. For a replay of our Best Consumer Ideas call and slides, contact

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, and the SP500 are now $1, $116.98-118.91, $79.71-80.31, 92.78-94.46, 1.96-2.01%, and 1, respectively.

We are off to a strong start YTD, however, as my Hall of Fame coach Dick Farley liked to remind this Eph, "keep your head on a swivel."

Casey Flavin

Director of Consumer Research and Sales