In the note below Josh Steiner provides an updated view on this morning’s claims data. Summarily, while the seasonally adjusted numbers were largely uneventful WoW, the trend in the NSA figures is flashing some weakness.

Independent of the claims data we would flag some further, emergent risks to a successful hand-off from #growthstabilizing to growth accelerating from here. We caught the positive inflection in the slope of growth back in late November. Currently, however, the quantitative and global macro factoring is suggesting the easy alpha may now be rearview – from here it gets a little more interesting.

Quantitative Factoring: For the 1st time in a while, our model is signaling lower highs for the SPX and higher lows for the VIX. All 9 S&P Sectors have been Bullish Trade/Bullish Trend for 24 of the last 25 sessions – being perma-anything is generally not a winning long-term strategy, and the extended positive price action, alongside rising oil and a cresting in sentiment, has mean reversion risk percolating here in the more immediate term.

Globally, the Bovespa and the KOSPI have both moved to Broken TRADE & TREND and the EuroStoxx50 is barely holding Trend support at 2615. TREND line breakdowns are a new development and are not insignificant, particularly when the signal confirms over multiple days and multiple markets.

Oil: Huge headwind developing for global consumption #GrowthStabilizing with Brent Oil signaling higher-highs and higher lows on our intermediate-term TREND duration. If you need a reason to start selling some stocks and covering Treasury shorts, that’s it.

Sentiment: With both the Bull-Bear Spread & NYSE Margin Debt making new cycle highs thru January, investor sentiment has moved towards the historical red flag region.

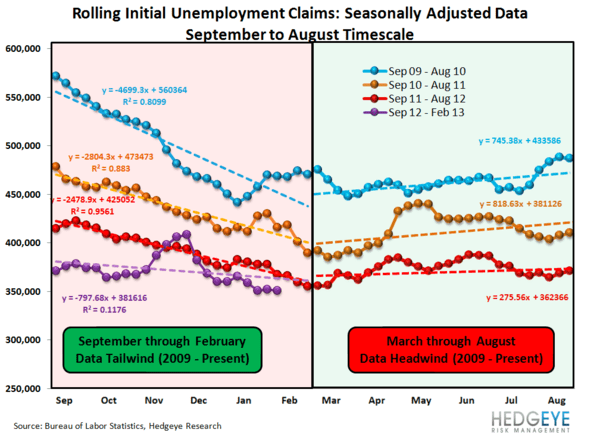

Seasonality: The employment shock experienced during the great recession was captured as a seasonal factor, creating a statistical distortional in the government reported employment and econ data persisting for five years (we're in year 4). The net effect of the distortion is that seasonal adjustments act as a tailwind to the SA labor market data from September – February, then reverse to a headwind over the March-August period. What’s the date today, again?

Congress: Congress remains the usual wild-card. What we do know is they will again attempt to save us from a problem they, themselves, perpetuated. The rhetoric and partisan acrimony will re-crescendo as we move through this month & beyond as congress seeks resolution to the fiscal policy trifecta of the Sequestration, Federal Budget, & the Debt Ceiling issues. As an aside, total debt now stands at $16.44T as of 2/5; approximately $50B higher than the previous Statutory limit of $16.394T.

As Keith highlighted this morning: “good spot to sell some stocks & cover some Gold/bonds”

- HEDGEYE Macro

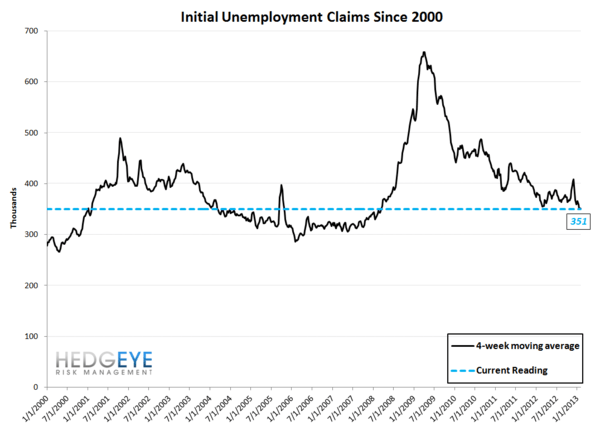

JOBLESS CLAIMS - ARE WE NEARING THE END OF THE LINE?

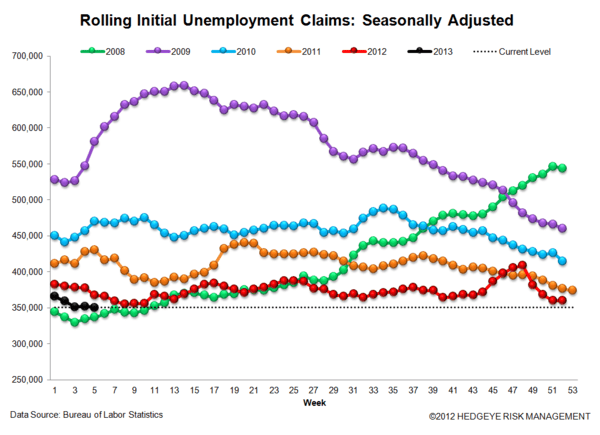

Initial claims continue to follow their predictable path of improvement through February, although this week's improvement was slightly more muted than expectations. To reiterate, there is another 3 weeks of improvement ahead, which will likely be followed by a ~1 month honeymoon period before the SA data starts to turn. Prior to revision, initial jobless claims fell 2k to 366k from 368k WoW, as the prior week's number was revised up by 3k to 371k.

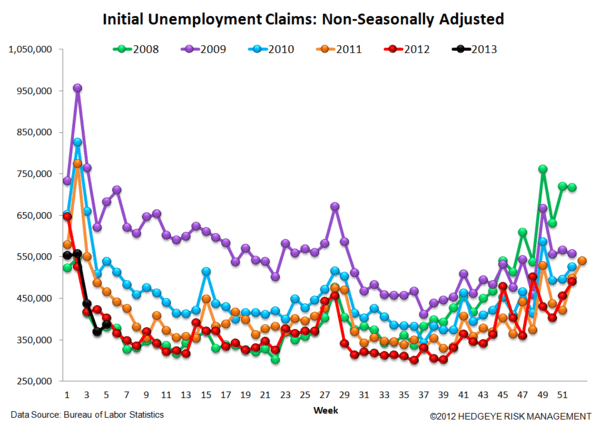

The headline (unrevised) number shows claims were lower by 5k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -1.5k WoW to 350.5k. The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -0.9% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -4.7%. This raises an interesting question about whether the payroll tax hike and high-earner tax rate changes are, in fact, having a negative impact on employment beneath the seasonal adjustment factors.

Joshua Steiner, CFA