This note was originally published at 8am on January 24, 2013 for Hedgeye subscribers.

“The skin of the bear must not be distributed until the bear has been killed.”

-Sir Winston Churchill

That’s what Churchill said after the Allies invaded Italy at Salerno in late 1943. If you’ve ever thought about trying to skin a bear yourself, locals from my neck of the woods would suggest you make sure it’s dead first too.

Risk management lessons in markets and in life tend to rhyme – if you practice common sense, that is. Some people get all religious about this stuff. Others practice some “technical” form of voodoo. I’m more into Churchillian-style strategic thinking myself.

During WWII, Churchill’s strategy was “to assign a larger importance to opportunism and improvisation, seeking rather to live and conquer in accordance with the unfolding event than to aspire to dominate often by fundamental decisions.” (The Last Lion, page 708)

Back to the Global Macro Grind…

If your risk management strategy is to A) Embrace Uncertainty and B) react to changing probabilities based on time and price, you’ll be satisfied doing a whole lot of nothing sometimes. Waiting and watching is a risk managed choice.

That’s what we did heading into Apple’s (AAPL) earnings event. Since we didn’t have any fundamental “edge” on the quarter, and our risk management signal (Bearish Formation, TAIL RISK $561) said to stay away, any other decision would have been a gamble.

That doesn’t mean today’s reactions to AAPL (down -8%) or Netflix (up +30%) don’t present opportunities. And that’s the point. The great goals in my life have been scored when preparation meets opportunity. Patience is a virtue.

With the SP500 up for 6 consecutive days (up +4.8% YTD and +10.4% from its mid-November 2012 fiscal cliff freak-out closing low), plenty a stock market bear’s bum has been skinned – but has The Bear been killed?

If your answer to that is yes, you and I (and the T Bay locals) need to have a little chat about wild animals.

To review, there are 2 core components to what we do:

- Quantitative Risk Management (Signals, Factoring, etc.)

- Fundamental Research

On both, there are a few chinks in the bull’s growth horns this morning.

Quant Signals:

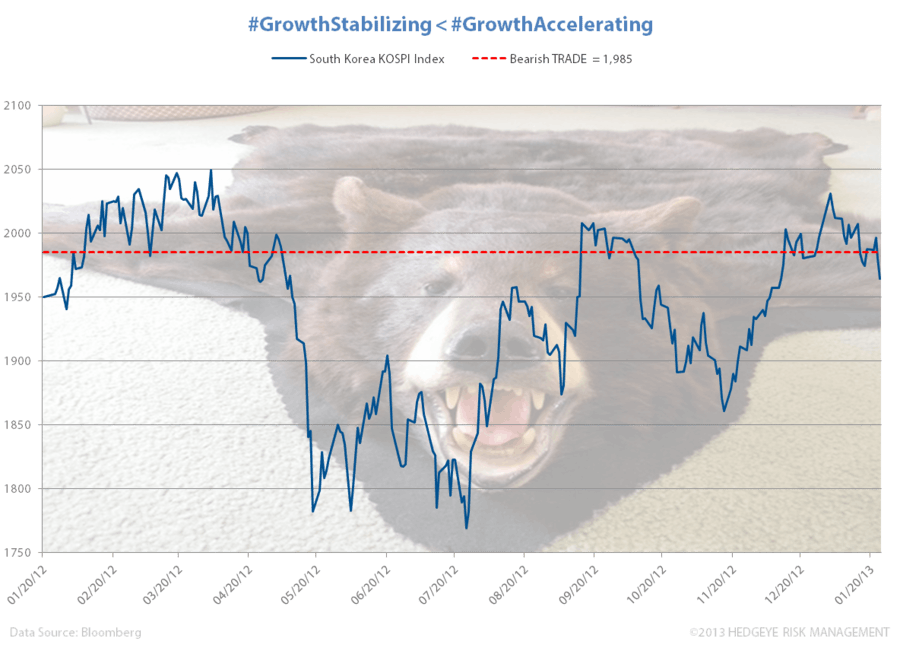

- KOSPI (-3.3% correction now from its YTD high) broke TRADE line support of 1985

- CHINA (Shanghai Comp), down -0.8% overnight, broke its immediate-term TRADE line of 2308

- JAPAN (Yen vs USD) failed to overcome 87.71 resistance again and is trading down hard, -1.2%

- Implied volatility in both the Yen and Japanese Equities is rising, fast

- Overbought signals across European Equities are being confirmed by lower immediate-term highs

- CRB Commodities Index failed at its long-term TAIL risk line of 306 (should snap 300 again today)

- Gold failed fast at intermediate-term TREND resistance of $1692

- Oil remains sticky, testing a TAIL duration breakout in both Brent and WTIC

- Copper, immediate-term TRADE overbought at $3.72/lb is making a series of lower long-term highs

- SPX overbought at 1496 and VIX oversold at 12.16 are what they are until they aren’t

Fundamental Research:

- Spain’s unemployment hits a higher-high at 26.02% (#PoliticalClass gets paid before The People)

- Japanese Exports fall another -5.8% y/y in DEC, despite setting their currency on fire!

- France printed a nasty Manufacturing PMI report for JAN, 42.9 (vs 44.9 in DEC)

Of course there are bullish Fundamental Research data points in this morning’s macro grind as well (imagine there wasn’t?). Chinese PMI of 51.9 in JAN was a little better than 51.5 in DEC; Germany’s Manufacturing PMI for JAN came in at 49.8 vs 46 last month, and the US economic data that’s pending (jobless claims today; New Home Sales tomorrow) continues to be bullish.

There’s always bulls and bears somewhere. Our daily service isn’t to be either – it’s to be objective and opportunistic when risk/reward changes (in any market or security) on the margin.

On the margin, was the Russell2000 making a lower-high yesterday a signal or was it noise? How about the US stock market’s breadth (advancers 46% vs decliners 50%) being negative on an up SP500 day? Why was there no volume (down 9% vs my TREND avg)? Channeling my inner-Churchill, inquiring risk management minds should never, ever, ever, give up asking questions.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, USD/YEN, UST 10yr Yield, AAPL, and the SP500 are now $1662-1692, $110.23-112.27, $3.65-3.71 $79.79-80.14 (USD bullish, Yen bearish), 80.71-90.41, 1.81-1.87%, $464-506 (Apple = immediate-term TRADE oversold in the post), and 1479-1496, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer