“Only practitioners (or people who do things) tend to spontaneously get the point.”

-Nassim Taleb

On a flight to Denver last night I had round 2 with Taleb’s new book, Antifragility. It wasn’t painful, but I definitely feel like the guy has something brewing inside of him. Transitioning from a market practitioner to a philosopher can’t be easy.

“I am re-connected to my practical self, my soul of a practitioner, as this is a merger of my entire history as practitioner and volatility specialist combined with my intellectual and philosophical interests in randomness and uncertainty…” (page 13)

People can go a little squirelly when they over-think the complex.

Back to the Global Macro Grind…

Buy or sell? Or, as my 2-year old daughter Callie has figured out (when asking me for something when she senses I am pre-occupied), “yes or no?”. If you are playing this Game of Risk in real-time, you don’t have time to philosophize. Save that for the weekends.

On Monday and Tuesday, we bought the US Equity market open (on red). Yesterday, we sold it (on green). It doesn’t always work out that way - but when it does, at least you know that you did it for a reason.

In yesterday’s rant, I outlined the reasons to make some risk adjusted sales (SP500 and US Treasury 10yr Yields immediate-term TRADE overbought) pre-game. And that’s really why I do what I do. I need a repeatable process so that I can have a plan.

Oh, and the plan is that the plans are always changing …

Some people don’t like that. It doesn’t sound sophisticated, I guess. But on that point, I agree with Taleb: “Simplicity has been difficult to implement in modern life because it is against the spirit of a certain brand of people who seek sophistications…”

“Less is more and usually more effective.” –Nassim Taleb

So, let’s slap on the Practitioner Pants and go down that path this morning (just bullet points from my notebook).

USA:

- Russell2000 reversed from its all-time high yesterday, closing down -1.2% at 896

- SP500 was down for the 2nd day in 3, finally making a lower high vs the YTD closing high of 1507

- US Equity Volatility (VIX) continues to signal a Risk Range with lower-highs and lower lows (11.94-14.62)

- US Equity market Volume is finally starting to show some flickers of light (+8% versus the TREND avg)

- All 9 S&P Sectors in our model are bullish on both our TRADE and TREND durations (19 of the last 20 days)

- US Dollar Index signaled immediate-term TRADE oversold at $79.24 yesterday

- US Treasury Yields (10yr) signaled immediate-term TRADE overbought at 2.04%; next support 1.93%

- Apple (AAPL) failed at immediate-term resistance yesterday; Risk Range = $420-461

EUROPE

- Eurostoxx50 and Eurostoxx600 both signaled immediate-term TRADE overbought yesterday

- DAX immediate-term TRADE support line of 7771 needs to hold for price momentum to continue

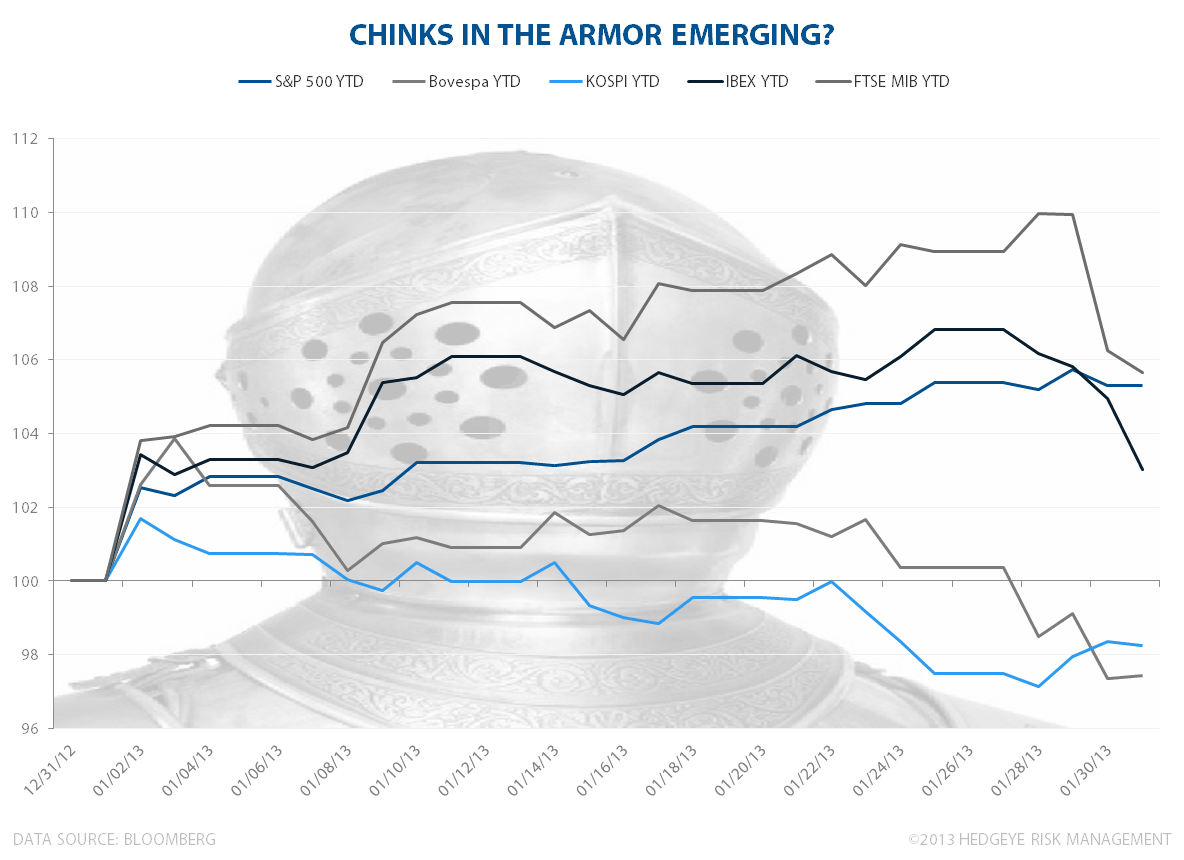

- Spain’s IBEX is snapping its immediate-term TRADE support of 8494 this morning (-1.6%)

- Italy’s MIB Index is breaking its immediate-term TRADE support of 17189 this morning (-1.1%)

- Greece’s squeezage finally stopped for a day (Athex index -1.5%)

- Euro (vs USD) = immediate-term TRADE overbought at $1.35 (support = $1.33)

ASIA/Brazil

- China’s stock market (Shanghai Comp) is signaling immediate-term TRADE overbought at 2384

- Japan’s Nikkei (up +28.6% as the Yen gets Taro Aso’d) has immediate-term TRADE resistance at 11159

- South Korea’s KOSPI remains bearish TRADE (1976 resistance) and bullish TREND (1959 support)

- India’s BSE Sensex is down (net) since being the first major country to cut rates in 2013

- Thailand and Vietnam (momentum markets in Asian Equities) corrected -1.1% and -1.6% overnight

- Brazil’s BOVESPA Index snapped immediate-term TRADE support of 60889, -1.8% yesterday

What’s new? We have 4 major countries (Brazil, South Korea, Spain, and Italy) showing initial chinks in the Global Equity market armor. It’s only an immediate-term TRADE signal (all remain bullish intermediate-term TRENDs), so do with it what you decide to do. I did.

Catalysts? It’s month-end today. Tomorrow you probably get another confirmation on why stocks are crushing US Treasuries and Gold for 2013 YTD (employment #GrowthStabilizing). But, at the same time, Oil prices up here are a new headwind to global consumption.

Buy or sell? Yes or no? These are simple questions requiring simple answers. No one has a Ph.d in playing a game that’s always changing. Stick with the practitioners. We can win this game together.

Our newly minted Senior Sector Head of Consumer Staples, Rob Campagnino, will be hosting an expert call on pyramid schemes ("An Expert's Opinion on Multi-Level Marketing, Pyramid Schemes and Herbalife” featuring multi-level marketing expert Dr. Jon M. Taylor) at 1030AM EST today. Ping if you are interested.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, EUR/USD, USD/YEN, 10yr UST Yield, and the SP500 are now $1, $113.02-115.22, $79.24-79.81, $1.33-1.35, 89.98-91.68, 1.93-2.04%, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer