This note was originally published at 8am on January 17, 2013 for Hedgeye subscribers.

“I found the PM not easy to talk to.”

-Eleanor Roosevelt

That’s what Eleanor Roosevelt said about her dinner discussions with Winston Churchill in the early 1940s. That’s what I’ve heard plenty of analysts say over the years in this business about their PMs too.

From a leadership perspective, what makes a good PM (Portfolio Manager)? What makes a great one? I’d love to hear your thoughts, because my sense is that there is a best practices answer developing. We are all hostage to the narrow scope of our own personal experiences and confirmation biases.

Of all the hedge fund PMs I’ve had the opportunity to work with, I’d say that Jon Dawson (former Dawson Samberg) was the easiest to talk to. When you are a young analyst, that’s helpful – having a good coach helps you learn. As you mature into a senior analyst, then a junior PM, it’s easy to start talking to yourself.

Back to the Global Macro Grind…

This game isn’t easy. That’s why I like to play it out loud. It’s the ultimate test of the mind. You have to be disciplined but flexible; aggressive, but calm; and patient, but nimble.

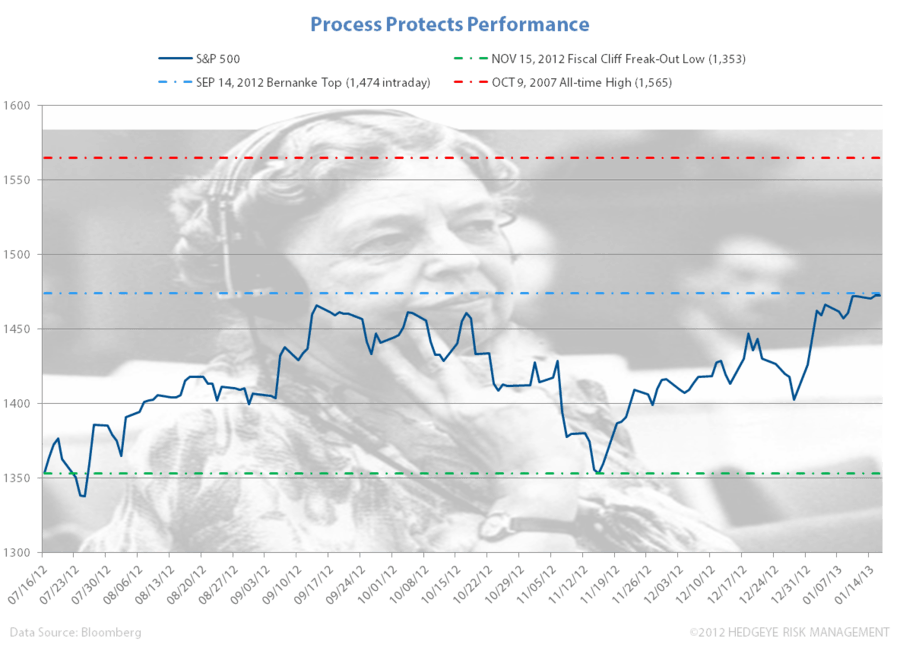

Staying in it to win it on the long-side of both US (and Global) Equities for the last 6 weeks hasn’t been easy. The first 17 days of January have left the SP500 stuck right at a 5-year closing high of 1472. I have 6 points of immediate-term upside left.

Contextualizing what that means to me doesn’t start with valuation – it starts with price performance:

- From the recent freak-out Fiscal Cliff low (NOV15) of 1353, the SP500 is up 119 pts (+8.8%)

- From the Bernanke Top (SEP14 intraday top of 1474), the SP500 is down 2 handles

- From the all-time SP500 high (OCT2007), the SP500 is still down -5.9%

Since buying tops isn’t cool (if you bought the SEP14 top, you had to slog for 4 months and be up +8.9% to get back to break-even), you want to be really careful when a market starts signaling that is might be done making higher-highs.

Particularly if you are paid to beat a relative performance bogey, that’s precisely why it’s so hard for PMs to sell-high, and then buy everything back lower. How do you know when a market is going to put in an immediate or intermediate-term top?

#Process

Now I am hardly suggesting my PM process is perfect on this front, but it’s better than bad. It’s been built out of making mistakes. And if you ask any absolute return PM in this business with a good to great long-term track record, I guarantee you they tell you this: the key to performing is eliminating big mistakes.

So let’s try to not do that.

If the market takes another run at the bears today, it may very well turn out to be as big a beta mistake being really long US Equities for the next 3 weeks as it was being short them for the last three.

I’m not just randomly choosing this morning to say that – my signals are all about price/volume/volatility:

- Last night was the 1st night in the last 10 trading days that my S&P Sector Model wasn’t what I call “perfectly bullish”

- Yesterday’s close also featured a fresh new negative-divergence with the Russell2000 not making a higher-high

- Since the prior closing high for the Russell (884) was an all-time high, that might matter – all-time is a long time

- Healthcare (XLV) signaled its 1st lower-high in my model of the year (it’s the #2 Sector at +4.5% YTD)

- Financials (XLF) signaled its 2nd consecutive lower-high in my model for the yr (it’s the #1 Sector at +4.6% YTD)

- US Equity Volume registered a bearish signal (SP500 tested making new highs on a down -19% volume signal)

- US Equity Volatility (VIX) signaled immediate-term TRADE oversold at 13.16

- US Equity Market Breadth was negative (44% advancers vs 52% decliners) with the SP500 at the highs

Apple had a 1-day move that explained some of this market skew (Nasdaq up vs Russell down). And that’s where having a quantitative view on a big index name like AAPL helps contextualize the rest of what I am being told to look at.

Since the core principle of how I think about risk management is to Embrace Uncertainty, I don’t know (and don’t really care to attempt to predict), what my signals are going to tell me. I have learned to shut-up, and just listen to them.

It’s not easy to listen. But, as my man Hemingway said, “I like to listen. I have learned a great deal from listening carefully. Most people never listen.”

Our immediate-term Risk Ranges for Gold, Oil (Brent), Corn, US Dollar, USD/YEN, UST10yr Yield, and the SP500 are now $1664-1684, $109.08-110.85, $7.12-7.41, $79.33-79.98 (USD is overbought), 88.06-89.85 (we re-shorted Yen via FXY yesterday), 1.81-1.89%, and 1466-1478, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer