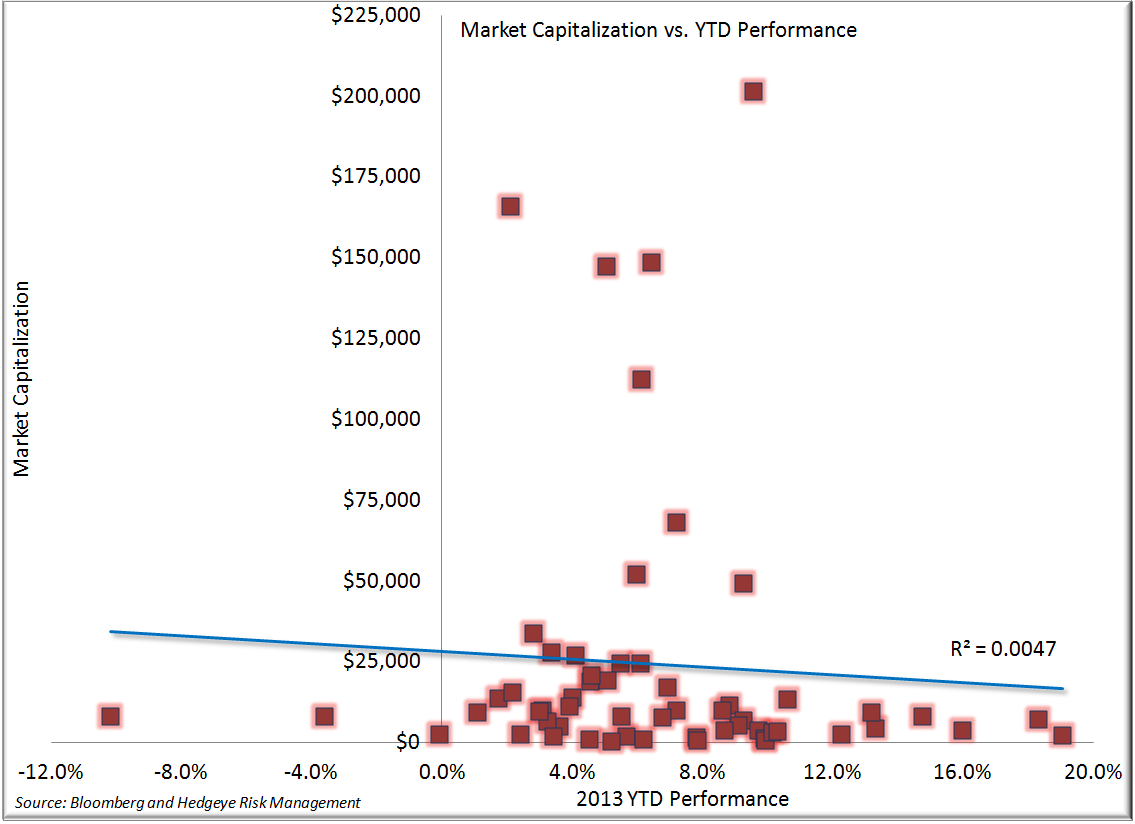

Earlier in the week, we took a look at the year to date performance across the consumer staples sector, looking for explanations related to short interest, 2012 performance and beta. Today we round out our discussion of quant factors with a look at market capitalization versus YTD stock performance. In much the same fashion as our prior attempt to identify the drivers of performance, our examination of market capitalization fell short.

We even took a look at the space absent the big uglies (market cap >$75 billion>, but the data didn't provide any incremental insight.

While these factors have been valuable indicators of outperformance in the broader market, consumer staples appears to be marching to its own beat. We remain convinced that the consumer staples sector is seeing inflows as investors seek to participate in a market rally they may not necessarily believe. We believe it, and see better ways to participate than with a consumer staples sector that is seeing historical valuation levels getting stretched.

Kind regards,

Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC

Matt Hedrick

Senior Analyst