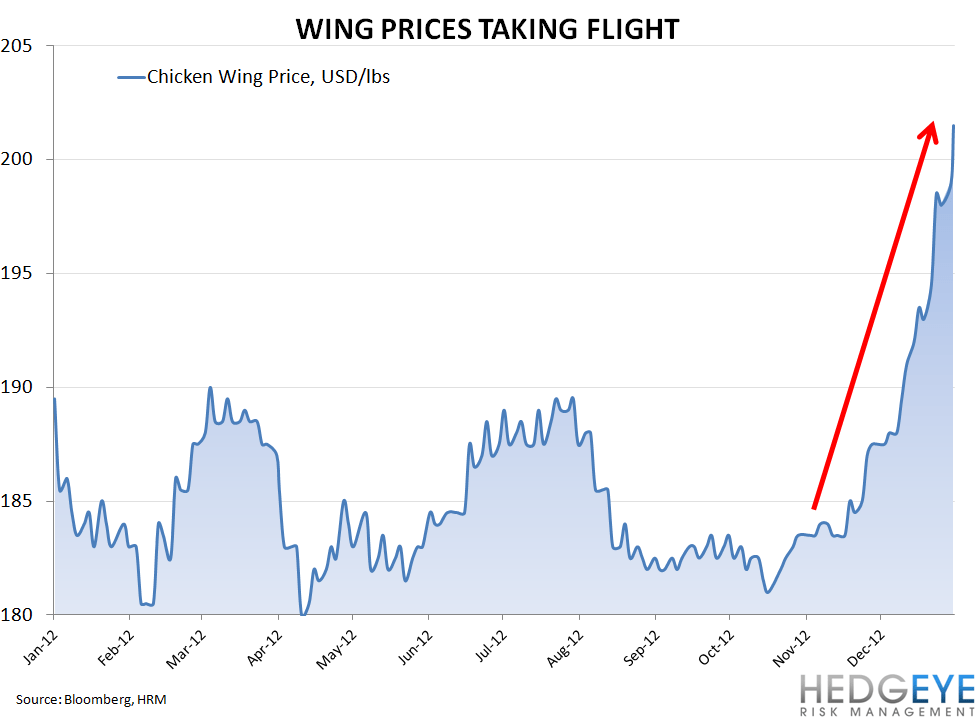

Chicken wing prices are, like last year, moving sharply higher to start the year. The difference in 2012 is that prices are moving above $2 per pound for the first time with a possibility of further upside. We continue to see risk to BWLD’s multiple.

Overview

In 2012, during the first 24 days of the year, chicken wing prices gained 14%. For much of the remainder of last year, prices stayed within a range of roughly 180-190 cents per pound. Year-to-date in 2013, wing prices are again moving higher: +7.2% YTD. During the 3Q earnings call, management warned that the price of wings was trending to $2.07 for the first two months of the fourth quarter and stated that they expected it to exceed that level heading into the super bowl.

The question is whether or not this expectation is baking in the possibility of McDonald’s expanding its testing of wings, currently in being sold in Chicago after a successful run in Atlanta, to its national system. BWLD’s guidance for earnings growth of 20% seems dependent on a number of factors, one important one being some moderation in wing prices in 2H13, per remarks from CFO Mary Twinen in October. MCD getting in on the act won’t help that happen.

Conclusion

- We still believe that BWLD’s multiple needs to reset much lower as earnings move lower

- Wing prices moderating in 2H13 could be difficult given industry conditions, wing demand, and potential weather impact on corn

- Moderating wing prices seem to be central to the bull case

- Selling wings by weight, rather than number, is likely to damage the brand and management knows this

- The first six weeks of 1Q12 saw co-op SSS increase 12.9%, presenting a difficult compare for the same period in ’13. If the switch is made to selling wings by weight, that could make comping last year’s strong first quarter even more difficult.

Howard Penney

Managing Director

Rory Green

Senior Analyst