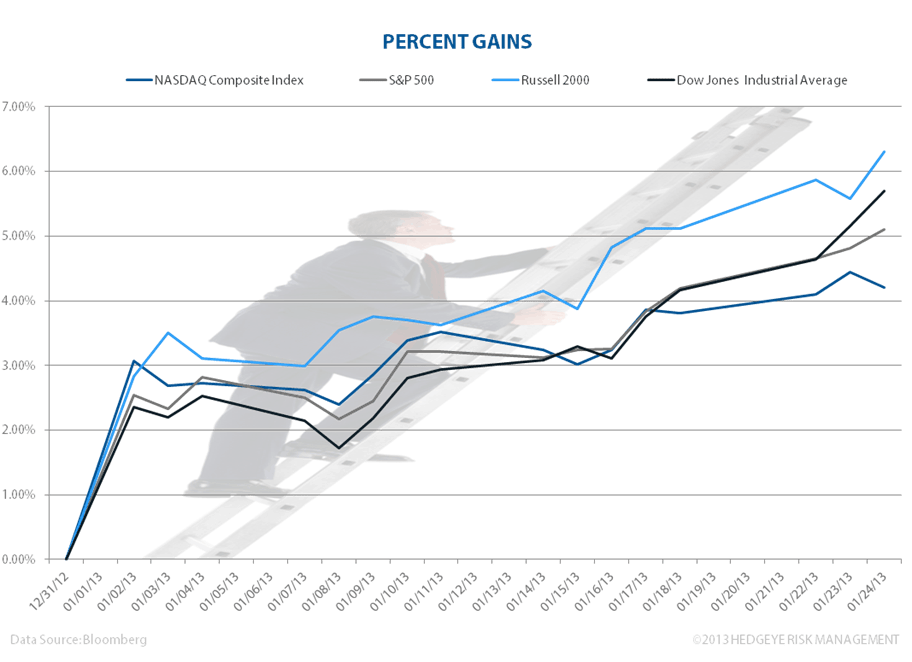

The market has treated bulls well with a great start to 2013. Several equity indices have hit multi-year highs and have put up extraordinary performance thus far considering that it’s still only January. Here’s a breakdown of several indices and their year-to-date performance:

S&P 500: +4.88%

Nasdaq Composite: +3.94%

Russell 2000: +6.11%

Dow Jones Industrial Average: +5.53%

The S&P 500 alone has been up for six consecutive days and is up +10.4% from its mid-November 2012 closing low. The bears have been killed and anyone who's fighting the broader market is in for a rough ride as fund flows continue to pour into US equities. Growth stabilizing is good for stocks, bad for bonds.